A UCC filing usually means you used business assets to back a loan – not that you defaulted. In most cases, it is just a public notice filed by a lender. It can still affect new financing, refinancing, or asset sales, so I’d check it right away.

Here’s the short version:

- UCC-1 filing: Public notice that a lender has a lien on your business assets

- Not a lawsuit: It does not mean a court case, judgment, or missed payment by itself

- Common reasons it appears: term loan, line of credit, equipment financing, SBA loan, MCA, or factoring

- How long it lasts: usually 5 years

- Main statuses: Active, Lapsed, or Terminated

- Where to check it: your state’s Secretary of State UCC database

- If paid off: the lender should file a UCC-3 termination

- If wrong: contact the lender, file a UCC-5 Information Statement, and speak with a lawyer if needed

A few facts stand out:

- State UCC searches are often free, but certified reports can cost about $25 to $100+

- Business credit reports can lag state records by around 30 to 90 days

- After a payoff demand, a lender may have 20 days to file a termination under UCC 9-513

Bottom line: if you see a UCC filing, I’d verify the lender name, filing date, collateral, and status first. Then I’d match it to your loan papers and make sure old liens get cleared before they slow down your next deal.

That’s the full point of this article: what a UCC filing is, why it showed up, what it means now, and what to do next if it is active, old, paid off, or wrong.

What a UCC Filing Actually Is

UCC stands for Uniform Commercial Code. It’s a shared set of state commercial laws. When a lender gives you a secured loan backed by business assets, it files a UCC-1 financing statement with the Secretary of State. That filing publicly shows the lender has a security interest in those assets.

That matters for creditor priority. It does not mean your business is in default.

What a UCC-1 Filing Is and What It Is Not

A UCC-1 is not a lawsuit or a judgment. It’s a public filing connected to a secured loan.

The lender’s claim begins when you sign the security agreement. It becomes public once the UCC-1 is filed. That filing helps give the lender priority over creditors who file later. If more than one creditor has a claim on the same assets, the one that filed first gets paid first.

What Business Assets a UCC Filing Can Cover

The collateral listed in the filing often tells you what kind of financing is behind it. In most cases, the collateral falls into one of two buckets: specific assets or a blanket lien.

| Collateral Type | What It Covers | Common Use Case |

|---|---|---|

| Specific asset lien | Named equipment, vehicles, or inventory | Equipment financing, vehicle loans |

| Blanket lien | All current and future business assets | SBA loans, bank term loans, MCAs |

A specific asset lien is tied to named property, like a truck or a piece of equipment. A blanket lien is much broader. It can cover all current and future business assets.

Because the filing is public, you can check it in state records and on business credit reports.

Where UCC Filings Show Up and Why They Are Public

UCC records are searchable through the Secretary of State’s online database in the state where your business is organized. They also show up on business credit reports from bureaus like Dun & Bradstreet and Experian Business.

These searches use your exact legal business name. So if there’s a typo, or if the filing uses an old entity name, it can be easy to miss.

Once you know what the filing covers, the next step is figuring out why it was filed.

Why a UCC Filing Appeared Against Your Business

A UCC filing usually shows up because a lender filed notice after your business pledged collateral. But sometimes the record looks odd because it’s old, tied to a refinance, or still sitting there after details changed. In most cases, the reason falls into three buckets: a loan, a revenue-based funding product, or an older record that was never updated.

Business Loans, Credit Lines, and Equipment Financing

Term loans and business lines of credit often come with a lien on most or all business assets, including equipment, inventory, and bank accounts. Some SBA loans, including larger EIDL loans, can also lead to UCC filings.

Equipment financing is a bit narrower. If you financed a commercial truck or a piece of machinery, the lender likely filed a lien tied to that one item of collateral. The filing can stay on record even after you pay off the debt, at least until the lender files a termination statement.

So if the filing doesn’t line up with a standard loan, it’s worth checking whether it connects to funding based on receivables or future sales.

Merchant Cash Advances, Factoring, and Revenue-Based Funding

MCA and factoring providers often file UCC-1 statements to claim their place against accounts receivable, future receivables, or, in some cases, all business assets through a blanket lien. These filings often cover receivables, contract rights, inventory, leases, notes, or the proceeds from them.

If that still doesn’t sound like your situation, the filing may trace back to a refinance or an older entity record.

Ownership Changes, Refinancing, or Outdated Entity Records

A filing can also look unfamiliar after refinancing or a business name change. When you switch lenders, the new lender files a new UCC-1, but the previous lender’s filing does not end on its own. That means both records can stay on file at the same time.

The same thing can happen when a business changes its legal name, moves from a sole proprietorship to an LLC, or updates its address. What looks like a new filing is often just an old record that was never terminated or updated. Old filings often remain under prior entity names or addresses, so check both current and prior legal names when you review state records.

The next step is to verify whether the filing is still active, released, or mistaken.

What a UCC Filing Means for Your Business Right Now

Now that you know why a UCC filing shows up, here’s what it means for your financing, your assets, and your day-to-day business.

A UCC Filing Does Not Automatically Mean Default

A UCC filing does not mean you missed a payment or did anything wrong.

Most of the time, it simply means a lender filed notice when you signed a secured financing agreement. A UCC-1 is a public notice of a secured transaction, not a lawsuit, judgment, or collection action.

That said, even if the filing does not point to a problem today, it can still shape what you’re able to borrow against or sell later.

How It Can Affect New Loans, Credit Decisions, and Asset Sales

A UCC filing can make borrowing, refinancing, and asset sales more difficult. If an existing lien is still active, a new lender may pause before offering credit because its claim would sit behind the current lien.

Here’s how the lien type can change your options:

| Feature | Specific-Collateral Lien | Blanket Lien |

|---|---|---|

| Coverage | Named assets only, such as a specific machine or vehicle | All business assets, present and future |

| Financing Impact | Lower; other assets may still be available to pledge | Higher; new lenders may be reluctant to take a junior position |

| Ease of Release | Easier to release specific assets | Harder; usually requires payoff or a release/subordination agreement |

If a blanket lien is getting in the way of new financing, talk to your original lender about a partial release or a subordination agreement. And don’t sell, transfer, or re-pledge collateral covered by an active lien unless you have the lender’s written consent.

How Long UCC Filings Last and Why Paid-Off Loans May Still Show

A UCC-1 filing is generally effective for five years from the date it was filed. That’s one reason these records can be confusing. Even after a loan is paid off, the filing may still appear until the lender files a release.

You’ll usually see one of these statuses:

- Active – current lien

- Lapsed – expired and no longer effective

- Terminated – formally released

sbb-itb-ba0a4be

How to Verify a UCC Filing and Decide What to Do Next

If you still haven’t pinned down the filing, use the state record to see whether it’s active, lapsed, or tied to the wrong business.

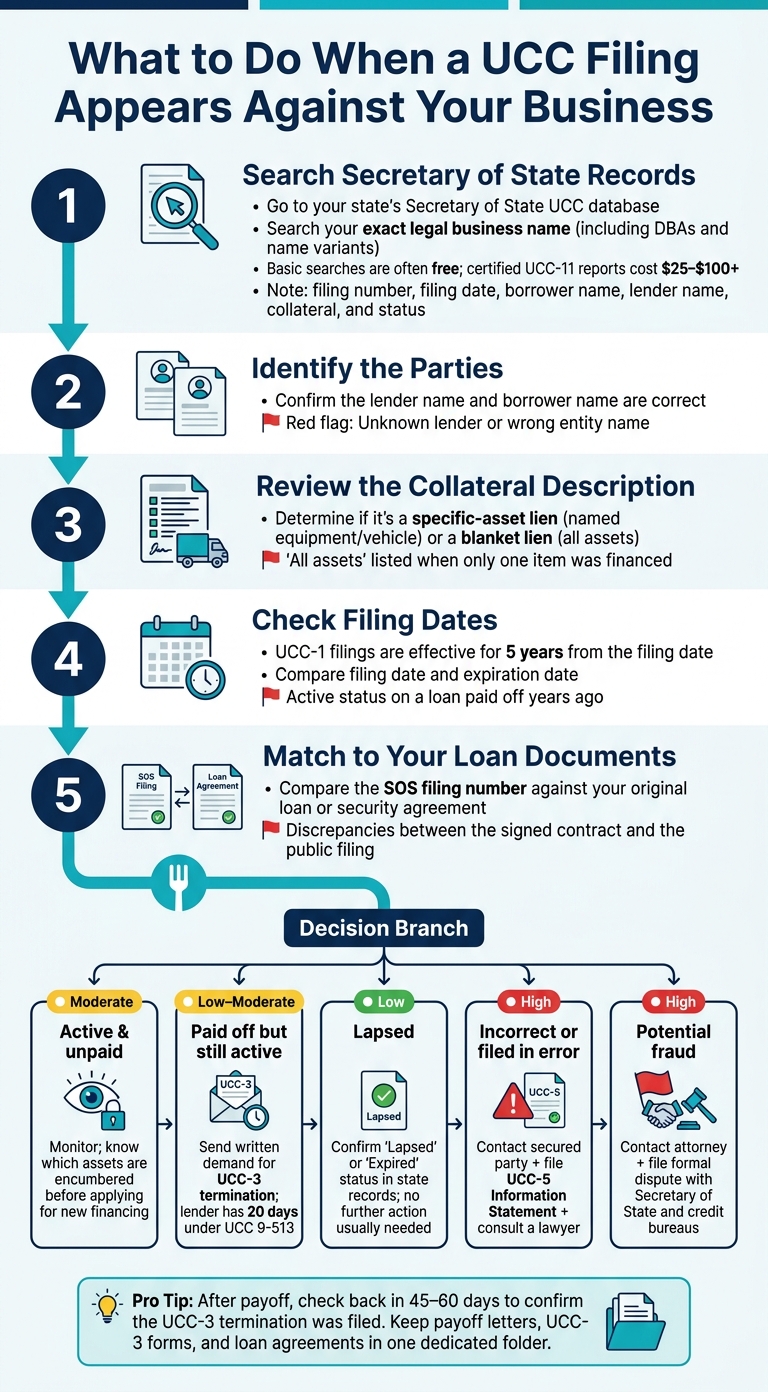

Search the Secretary of State Records and Read the Filing Carefully

Start with the Secretary of State database in the state where the filing was made. In most cases, that’s the state where your business was formed.

Search your exact legal business name and any DBA names too. Tiny differences in punctuation, spacing, or wording can keep a filing out of sight.

When you find a record, review it line by line. Note the filing number, filing date, borrower name, lender name, collateral description, and current status. Basic Secretary of State searches are often free, but certified copies or UCC-11 reports usually cost $25 to $100+, depending on the state.

It also helps to compare what you find with your business credit reports from Dun & Bradstreet or Experian Business. Just be careful not to treat those reports as the last word. They can lag behind live Secretary of State records by 30 to 90 days.

Match the Filing to Your Loan Documents and Check for Red Flags

After you find the record, match it against your loan paperwork before you assume it belongs to you.

Pull the original loan agreement, equipment finance contract, or merchant cash advance papers. Then compare those documents with the Secretary of State filing.

| Step | What to Verify | Red Flags |

|---|---|---|

| 1. SOS Search | Search the exact legal name, including DBAs and known variants. | Liens from unknown lenders or suspicious entities. |

| 2. Identify Parties | Confirm the lender name and borrower name are correct. | Wrong entity name or a lender you never did business with. |

| 3. Review Collateral | Check whether the description is specific or a blanket lien covering all assets. | "All assets" listed when the loan was only for specific equipment. |

| 4. Check Dates | Compare the filing date and expiration date, which is usually five years out. | Active status for a loan that was paid off years ago. |

| 5. Match Documents | Compare the SOS filing number with your original loan or security agreement. | Discrepancies between the signed contract and the public filing. |

The collateral description matters a lot here. If the filing says "all assets" but you only financed a piece of equipment, that’s a sign to stop and take a closer look.

What to Do if the Filing Is Valid, Paid Off, Lapsed, or Wrong

What you do next depends on the filing’s status.

| Status | Risk Level | Next Action |

|---|---|---|

| Active and unpaid | Moderate | Monitor it and make sure you know which assets are encumbered before applying for new financing. |

| Paid off but still active | Low to Moderate | Send a written demand to the lender for a UCC-3 termination statement right away. |

| Lapsed | Low | Confirm the state record shows "Lapsed" or "Expired"; usually no further step is needed. |

| Incorrect or filed in error | High | Contact the secured party, file a UCC-5 Information Statement with the state, and get legal help. |

| Potential fraud | High | Contact an attorney and file a formal dispute with the Secretary of State and credit bureaus. |

If the debt has been paid but the filing still shows as active, send a written demand under UCC Article 9-513. The lender then has 20 days to file the UCC-3 termination. If they miss that deadline, they can face statutory and actual damages.

After the lender says the termination has been filed, search the Secretary of State database again and make sure the status changed. Keep your payoff letters, UCC-3 forms, and formation documents together so you can find them fast when you need them.

Conclusion: Add UCC Checks to Your Business Compliance Routine

Once you confirm the filing is real, the next step is simple: don’t let it hold up your next deal. A UCC filing is a normal lending record, but it can still affect future financing and asset sales.

An active lien can block or delay a new loan or an asset sale until it’s released. That’s why payoff follow-up matters.

Add UCC checks to your compliance routine. Search your Secretary of State’s UCC database using your exact legal entity name, review your UCC records every quarter, and after you pay off a secured debt, check back in 45 to 60 days to make sure the termination was filed.

Keep a dedicated folder with:

- Original loan agreements

- Final payment receipts

- Written payoff confirmations

- File-stamped UCC-3 termination copies

If a new lender asks for proof that a lien was released, you’ll have it ready.

Keep UCC records with your loan files so you can clear liens fast when you need new financing.

FAQs

Can a UCC filing hurt my business credit?

A UCC filing usually does not directly lower your business credit score. Still, it can show up on your business credit report for lenders, vendors, and landlords to review.

On its own, a UCC filing is a normal part of secured lending. It simply tells others that a lender has a claim on certain business assets.

That said, the picture can change when there are multiple active liens, outdated filings, or a filing that is inaccurate or unauthorized. In those cases, your business may look riskier on paper, which can make financing or trade terms harder to get.

Can I get another loan with an active UCC filing?

Yes. Many businesses can still get another loan even with an active UCC filing.

That said, a new lender will look closely at any current claims on your collateral. If the filing places a blanket lien on all business assets, the lender may pause. Why? Because if you default, they could end up in second position.

In some cases, you may need:

- a lien subordination agreement

- a partial release of assets

What if I never signed for this UCC filing?

If you find a UCC filing you never authorized, it could be a mistake or a sign of identity theft. First, check your state’s Secretary of State records to confirm the filing details, including the secured party and the collateral listed.

If the filing is wrong or was submitted by mistake, contact the creditor named in the record and ask for it to be removed. If the creditor doesn’t respond or you don’t recognize them, you may need to file a correction statement or UCC-5 form and speak with a legal professional.