Choosing the right jurisdiction for your global business depends on your goals: tax savings, investor access, banking ease, or market focus. Here’s a quick breakdown of the top options:

- US LLC: Ideal for global SaaS businesses targeting US customers. Offers 0% federal tax (if no US-source income), full access to US payment platforms (Stripe, PayPal), and remote banking via Mercury or Wise. However, compliance (like IRS Form 5472) is critical to avoid penalties.

- UK LTD: Best for UK/EU-focused businesses or founders seeking SEIS/EIS tax relief for investors. Low setup costs (£12) and remote banking (Starling, Tide) make it quick and affordable, but corporation tax can reach 25%.

- Singapore Pte Ltd: Perfect for high-profit businesses targeting Asia. Enjoys a 4.25% effective tax rate for the first 3 years, 0% dividend tax, and a high S$1M GST threshold. However, it requires a local director and higher compliance costs.

- UAE Free Zone: Great for founders relocating to the UAE. Offers 0% corporate and personal income tax (with conditions), residency visas, and a strong crypto licensing framework. Setup costs are higher, and banking access can be challenging.

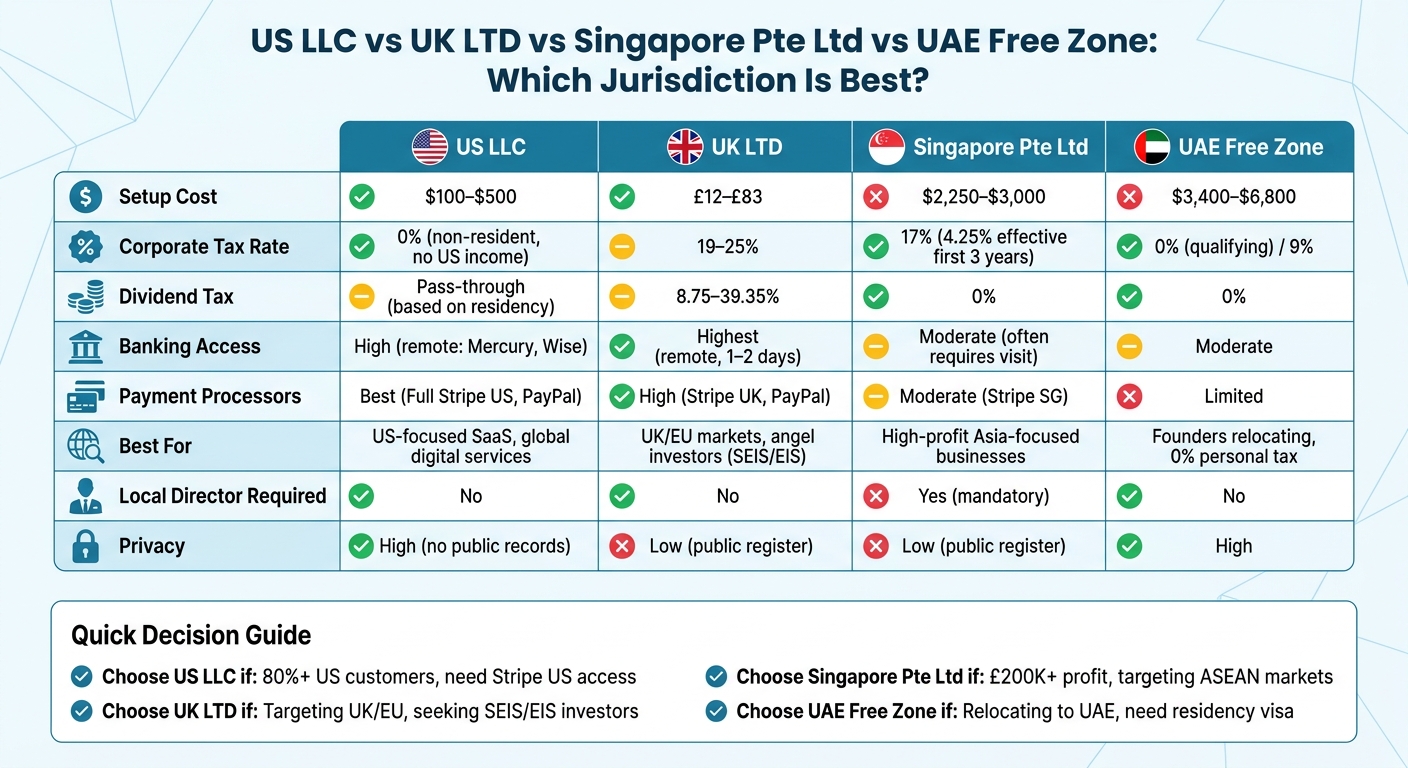

Quick Comparison

| Factor | US LLC | UK LTD | Singapore Pte Ltd | UAE Free Zone |

|---|---|---|---|---|

| Setup Cost | $100–$500 | £12–£83 | $2,250–$3,000 | $3,400–$6,800 |

| Corporate Tax Rate | 0% (non-resident, no US income) | 19–25% | 17% (4.25% effective) | 0% (qualifying) / 9% |

| Banking Access | High (remote options) | Highest (remote, fast) | Moderate (local visit often required) | Moderate |

| Investor Preference | US VCs (Delaware C-Corp preferred) | UK/EU Angels (SEIS/EIS) | Asia Investors | Limited VC interest |

| Privacy | High (no public records) | Low (public register) | Low (public register) | High |

Key Takeaway: Your choice depends on where your customers are, how much profit you expect, and your personal tax residency. This is especially important for digital nomads navigating tax obligations across multiple borders. For US-focused SaaS, a US LLC is often the best pick. For UK/EU markets, go with a UK LTD. For high profits in Asia, Singapore Pte Ltd wins. And for tax-free relocation, UAE Free Zone is worth considering.

US LLC vs UK LTD vs Singapore Pte Ltd vs UAE Free Zone: Comparison Table

When deciding between a US LLC, UK LTD, Singapore Pte Ltd, or UAE Free Zone company, there are nine critical factors to consider. Formation costs range widely, from as low as £12 for a UK LTD to over $3,400 for a UAE Free Zone company [1][3]. Corporate tax rates also vary, with some setups like a US LLC (non-resident with no US income) and UAE Free Zone (qualifying businesses) offering 0%, while a UK LTD could face up to 25% [1][4]. Banking access and payment processor compatibility also play a significant role, with the US and UK offering the easiest solutions.

| Factor | US LLC (Wyoming) | UK LTD | Singapore Pte Ltd | UAE Free Zone |

|---|---|---|---|---|

| Formation Cost | $100–$500 | £12–£83 | S$3,000–S$4,000 (~$2,250–$3,000) | $3,400–$6,800 |

| Annual Maintenance | $610–$2,210 | £834–£1,534 (~$1,050–$1,930) | S$3,000–S$5,000 (~$2,250–$3,750) | $2,700–$5,400 |

| Corporate Tax Rate | 0% (non-resident, no US income) | 19–25% | 17% (4.25% effective first 3 years) | 0% (qualifying) / 9% (>AED 375k profit) |

| Personal Tax (Dividends) | Pass-through (based on residency) | 8.75–39.35% | 0% | 0% |

| Payment Processor Access | Best (Stripe US, PayPal Business, Square) | High (Stripe UK, PayPal) | Moderate (Stripe SG) | Moderate |

| Banking Ease (Non-Resident) | High (Mercury, Relay, Wise – 100% remote) | Highest (Starling, Tide – approved in 1–2 days) | Moderate (often requires visit or nominee) | Difficult (requires residency/office) |

| VC Preference | Delaware C-Corp preferred | UK LTD (SEIS/EIS eligible) | Pte Ltd (ASEAN/Asia investors) | Free Zone (MENA/South Asia) |

| Privacy | High (no public ownership records) | Low (public register) | Low (public register) | High |

| Local Director Required | No | No | Yes (mandatory) | No |

Singapore offers an advantage with its S$1,000,000 GST threshold, which is 6.4 times higher than the UK’s £90,000 VAT threshold. This allows startups generating significant revenue more time before incurring consumption tax obligations [1]. For example, a UK startup earning £200,000 in profit would pay approximately £90,730 more in combined taxes than a Singapore startup in its second year [1].

"The real test is not incorporation speed – it is banking access. Getting your company registered takes a day or two… Getting a business account that international clients and suppliers accept is where most non-resident founders get stuck." – Bertrand Théaud, Founder, Statrys [6]

Revenue sources also influence jurisdiction choice. For businesses with 100% US-based revenue, a US LLC can save on the 0.4–1.5% currency conversion fees that UK or Singapore entities would face when handling USD payments [4]. On the other hand, startups seeking UK angel investors often require a UK LTD to qualify for SEIS/EIS benefits [4]. Meanwhile, the UAE Free Zone is a compelling option for entrepreneurs aiming to relocate, as company formation provides a direct path to residency visas valid for 2–10 years [3].

This table and analysis provide a solid starting point for understanding the key differences among these jurisdictions.

sbb-itb-ba0a4be

US LLC: Overview, Pros, Cons, and Tax Details

A single-member US LLC owned by a non-resident is considered a disregarded entity for federal tax purposes [4]. Unlike UK LTDs or Singapore Pte Ltd companies, the LLC itself doesn’t pay federal income tax. Instead, profits and losses are passed directly to the owner.

For non-residents with no US employees, office, or Effectively Connected Income, the federal tax liability for the LLC is usually $0 [4]. Additionally, forming a US LLC provides access to US payment platforms like Stripe US and banking services such as Mercury or Relay. This can help avoid currency conversion fees, which typically range from 0.4% to 1.5% for non-US entities. For example, a SaaS founder earning $200,000 annually from US customers could save between $800 and $3,000 per year on transaction fees.

However, compliance is a key challenge for this structure. Even if your LLC generates no revenue, you’re required to file IRS Form 5472 along with a pro-forma Form 1120 annually. Missing this filing can result in a $25,000 penalty [4][7].

"The most expensive mistake in international business formation is not the wrong jurisdiction. It is forming without a compliance plan, and discovering the obligation only when the penalty notice arrives." – Corporatee [7]

For UK residents, there’s an added layer of complexity. While the IRS treats the LLC as a pass-through entity, HMRC often classifies it as "opaque", meaning it’s taxed as a corporation in the UK. This difference in classification can lead to double taxation for UK residents. As entrepreneur Jett Fu explains, HMRC’s treatment of a US LLC as opaque makes a UK LTD a safer option for UK-based founders [4].

The cost to form a US LLC varies by state, ranging from $100 in Wyoming to $300 in Delaware. Annual maintenance fees also differ, from $60 to $300 depending on the state. Wyoming is popular for its low fees and privacy protections, while Delaware is favored by founders aiming to raise US venture capital within 18 months.

US LLC Pros and Cons

| Pros | Cons |

|---|---|

| No federal tax if no US-source income | $25,000 penalty for missing Form 5472 filings |

| Pass-through taxation (no corporate-level tax) | Risk of double taxation for UK residents due to HMRC’s "opaque" classification |

| Access to US payment platforms (Stripe US, PayPal, Square) | Not eligible for UK SEIS/EIS tax reliefs |

| Remote banking options (e.g., Mercury, Relay, Wise) | State-level fees vary ($60–$300/year) |

| No residency requirement to form an LLC | US venture capitalists often prefer Delaware C-Corps over LLCs |

| Strong privacy protections (especially in Wyoming) | complex sales tax compliance across 13,000+ jurisdictions (rates from 0% to 10.25%) |

These advantages and drawbacks highlight the scenarios where a US LLC is most beneficial.

Best Use Cases for US LLC

A US LLC works particularly well for SaaS and digital service businesses primarily targeting American customers. If most of your revenue (80% or more) comes from US clients paying in USD, avoiding currency conversion fees can make this structure worthwhile.

Amazon sellers using the Amazon US platform may also benefit from forming a US LLC to limit legal liability. For those selling in the UK or EU as well, maintaining a UK LTD for those regions can help isolate potential issues and streamline operations globally.

Early-stage founders testing the US market often start with a US LLC before transitioning to a Delaware C-Corp. However, founders planning to raise institutional venture capital within 18 months should note that most US VCs prefer Delaware C-Corps. Similarly, UK residents raising funds from UK angel investors may find a UK LTD more advantageous, as a US LLC disqualifies them from SEIS/EIS tax incentives. A UK LTD also offers quicker formation, simpler banking, and avoids HMRC’s double taxation issues.

US LLC Tax Structure

The tax framework for a US LLC depends on whether you have US-source income and where you live. For non-resident owners without US employees, a physical office, or activities classified as "Engaged in Trade or Business in the United States", federal tax liability is generally $0 [4]. Profits are reported on your personal tax return in your country of residence. For instance, if you live in the UAE, where there’s no personal income tax, you pay nothing. However, as a UK resident, you would owe income tax on the profits, which could range from 20% to 45%, depending on your tax bracket.

Annual filings for these obligations typically cost between $500 and $2,000 when handled by professionals. State-level fees vary widely: Wyoming charges a $60 annual report fee, while Delaware imposes a $300 annual franchise tax. While some states like Alaska, Delaware, Montana, New Hampshire, and Oregon have no state-level sales tax, selling goods or specific digital services in other states may require sales tax registration. With over 13,000 jurisdictions and rates ranging from 0% to 10.25%, compliance can become intricate.

This tax setup, along with the outlined compliance requirements, differentiates the US LLC from models like UK LTD or Singapore Pte Ltd.

UK LTD: Overview, Pros, Cons, and Tax Details

A UK Limited Company (LTD) offers a quick and affordable incorporation process through Companies House, with same-day electronic setup available for just £12. This makes it a go-to option for founders needing to establish their business in under 24 hours [4]. Non-residents also benefit from remote banking solutions provided by platforms like Starling, Tide, and Wise – no in-person visits required, unlike jurisdictions such as Singapore or the UAE [1][3]. These features make the UK LTD particularly appealing for entrepreneurs seeking speed, convenience, and cost-efficiency.

The UK also stands out for its SEIS and EIS schemes, which offer tax relief to angel investors [4]. On the flip side, the tax structure can be less appealing for high-profit businesses. Corporation tax ranges from 19% for profits under £50,000 to 25% for profits exceeding £250,000 [7][4]. When combined with dividend taxes of 8.75% to 39.35% for UK residents, the overall tax burden can climb to nearly 50% [1][4].

"Companies House is genuinely one of the best business registration systems anywhere." – Jett Fu, Cross-border entrepreneur, Global Solo [4]

Another challenge is the UK’s VAT registration threshold of £90,000, which is significantly lower than Singapore’s S$1,000,000. This means UK businesses face the 20% VAT compliance requirement much sooner, potentially raising B2C prices and impacting competitiveness [1]. Annual compliance costs, covering accountant fees for tax returns, annual accounts, and the £13 Confirmation Statement, range from £834 to £1,813 [1][4]. Additionally, US residents with a UK LTD may encounter Controlled Foreign Corporation (CFC) reporting requirements, potentially triggering US taxes on foreign profits [4].

Here’s a closer look at the pros, cons, and tax details of a UK LTD.

UK LTD Pros and Cons

The table below highlights the main advantages and drawbacks of setting up a UK LTD:

| Pros | Cons |

|---|---|

| Same-day incorporation for £12 | High corporation tax (25%) for profits over £250,000 |

| Remote banking for non-residents (Starling, Tide, Wise) | Low VAT threshold (£90,000) triggers 20% compliance early |

| Access to SEIS/EIS for UK angel investors (50%/30% tax relief) | Dividend taxes for UK residents range from 8.75% to 39.35% |

| Respected English Common Law framework | HMRC classifies US LLCs as "opaque", creating double-taxation traps |

| Low annual compliance costs (£834–£1,813) | Not ideal for high-profit digital nomads (combined tax ~50%) |

| Trusted by US and EU B2B buyers | Complex visa routes (Skilled Worker visa costs £2,500+, takes 3–6 months) |

Best Use Cases for UK LTD

A UK LTD is an excellent choice for UK-based founders who prefer to operate within a familiar business environment without dealing with visa challenges. It’s also ideal for attracting angel investors, as the SEIS/EIS tax relief schemes require a UK LTD structure [4]. For businesses targeting the US and EU markets, the UK’s legal framework is widely recognized and trusted by B2B buyers in these regions.

Early-stage or low-revenue businesses, especially those earning under £200,000, benefit from the UK LTD’s low setup and compliance costs. For these companies, the higher costs associated with jurisdictions like Singapore or the UAE may not be justifiable [1]. Additionally, professional services firms and fintech startups gain from the UK’s status as a global financial hub with a well-established regulatory environment. However, for high-profit digital nomads with no UK ties, Singapore or the UAE may be better options due to their more favorable tax systems [1].

UK LTD Tax Structure

The tax framework of a UK LTD is a key factor in determining its suitability for your business. Corporation tax is tiered, with a 19% rate for profits up to £50,000 and a 25% rate for profits above £250,000 [7][4]. Profits within the marginal band are taxed at an effective rate of 26.5% [7][1]. If you own multiple companies, the thresholds are divided across all entities under common control, as per the UK’s associated company rules [7].

For UK residents, dividend taxation adds another layer of complexity. After a £1,000 tax-free allowance, dividends are taxed at rates ranging from 8.75% (basic rate) to 39.35% (additional rate) for the 2025/26 tax year [4]. To put this into perspective, a UK-based founder earning £200,000 in profit would take home roughly £101,875 after corporation and dividend taxes. In comparison, a Singapore-based founder would retain £192,605 [1]. The UK’s VAT rate stands at 20%, applying to most goods and services once the £90,000 threshold is crossed [7].

"UK only wins on compliance cost when pre-revenue or below ~£30K profit. The compliance premium [of Singapore] is irrelevant against tax savings at any meaningful revenue." – James Hartley, SME Growth Strategist, ThriveOnz360 [1]

Singapore Pte Ltd: Overview, Pros, Cons, and Tax Details

Singapore Pte Ltd is a popular choice for businesses in the Asia-Pacific region, thanks to its low effective tax rates and the absence of personal taxes on dividends or capital gains. This setup is particularly appealing for high-profit ventures [1]. Incorporating a Singapore Pte Ltd company costs approximately S$1,200 (~$876), and at least one resident director is required. Non-residents often hire nominee directors, which typically costs between S$1,500 and S$3,000 ($1,095–$2,190) annually [1]. While opening a bank account with local banks like DBS or OCBC often requires an in-person visit, virtual banks such as Aspire provide quicker options for non-residents [1].

The Startup Tax Exemption (SUTE) significantly reduces the effective tax rate to 4.25% for the first S$100,000 of profit, making Singapore’s rates much lower than the UK’s 19–25% corporation tax. Additionally, Singapore’s GST threshold of S$1,000,000 (~$730,000) delays tax compliance for early-stage businesses [1]. Annual compliance costs range from $873 to $1,635, covering essential services like secretarial fees, accounting, and filings with the Accounting and Corporate Regulatory Authority (ACRA) [1].

"Singapore wins on tax (4.25% effective vs UK 25% corporation tax, 0% dividend tax, 0% capital gains tax), VAT/GST threshold (S$1M vs UK’s £90K – 6.4× higher), and founder visa speed (3 weeks vs 3–6 months)." – James Hartley, Former City of London fintech advisor, ThriveOnz360 [1]

Singapore’s territorial tax system, which only taxes locally sourced income, benefits digital nomads and globally focused service businesses. For instance, a Singapore-based founder with £200,000 (~$260,000) in profits could save around £90,730 (~$118,000) annually compared to a UK-based founder due to the absence of dividend and capital gains taxes [1]. However, businesses with revenue exceeding S$10 million must undergo mandatory audits, and the requirement for a local director can complicate operations for fully remote teams [1][11].

Singapore Pte Ltd Pros and Cons

| Pros | Cons |

|---|---|

| 4.25% effective tax rate for the first 3 years (SUTE) | Requires a local director (nominee costs $1,095–$2,190/year) |

| 0% tax on dividends and capital gains | Physical bank account setup often needed (e.g., DBS, OCBC) |

| High GST threshold (S$1,000,000 or ~$730,000) | Annual compliance costs ($873–$1,635) are higher than the UK ($609–$1,324) |

| Access to ASEAN (680M population), China, and India | Mandatory audits for revenue above S$10 million |

| IP Development Incentive (5–10% tax on qualifying IP income) | Smaller businesses may find compliance costs outweigh benefits |

| Quick Employment Pass (founder visa) approvals (about 3 weeks) |

These pros and cons help determine whether Singapore Pte Ltd aligns with specific business goals.

Best Use Cases for Singapore Pte Ltd

Singapore Pte Ltd is ideal for businesses with substantial profits – typically over £200,000 (~$260,000) – where tax savings justify higher compliance costs [1]. It’s particularly suited for companies targeting ASEAN markets, such as Malaysia, Indonesia, and the Philippines, or IP-driven ventures like SaaS platforms and deep tech startups. These businesses can take advantage of the Intellectual Property Development Incentive (IPDI), which offers a reduced tax rate of 5–10% on qualifying income [1][5].

Digital nomads, venture-backed startups seeking Asian investors, and companies planning to transition to a Delaware C-Corp also benefit from Singapore’s business-friendly framework. Additionally, professional services firms, fintech companies, and e-commerce businesses leverage Singapore’s robust regulatory system and its extensive double-tax treaty network, which spans over 80 jurisdictions [5][11].

Singapore Pte Ltd Tax Structure

Singapore imposes a 17% flat corporate tax rate on both resident and non-resident companies [10][11]. Qualifying startups enjoy a 75% tax exemption on the first S$100,000 (~$73,000) of chargeable income and a 50% exemption on the next S$100,000, resulting in an effective tax rate of 4.25% for their first three years [10][11]. Non-startups receive a 75% exemption on the first S$10,000 (~$7,300) and a 50% exemption on the next S$190,000 (~$138,700) [10][11]. For the 2025 income year (YA 2026), eligible companies will benefit from a 50% Corporate Income Tax rebate, capped at S$40,000 (~$29,200) [10].

Singapore operates a one-tier taxation system, meaning dividends distributed by resident companies are tax-free for shareholders [10]. Additionally, there is no capital gains tax, except for gains arising from trading activities [11]. The GST rate is set at 9% as of 2024 and applies only when annual revenue exceeds S$1,000,000 [1]. Companies must file their Estimated Chargeable Income (ECI) within three months of their financial year-end and submit their final tax return (Form C-S or C) by November 30 each year [11]. Starting January 1, 2025, a 15% domestic top-up tax will apply to multinational enterprise groups with annual revenues exceeding €750 million (~$817 million) [10].

UAE Free Zone: Overview, Pros, Cons, and the 0% Tax Reality

UAE Free Zone companies are a magnet for founders, thanks to the promise of 0% corporate tax and residency options that outshine what US LLCs or UK LTDs typically offer [5]. However, setting up in the UAE comes with a price tag – formation costs range between $3,000 and $5,000, far exceeding the UK’s $100–$150 or Singapore’s ~$1,200 [9]. Strategically located at the crossroads of Europe, Asia, and Africa, the UAE is an attractive base for international trading firms and family offices [5]. Founders also benefit from Golden Visa residency for themselves and their families, alongside 0% personal income tax [9].

Banking access is rated 4 out of 5 stars – better than many offshore jurisdictions but not quite on par with Singapore’s top-tier rating [9]. The UAE also stands out for its VARA (Virtual Assets Regulatory Authority) licensing, making it a go-to destination for crypto and blockchain businesses [9]. However, the much-touted "0% tax" comes with fine print: it only applies to companies that meet specific substance requirements, including local management and decision-making. Without this, Free Zone companies face the standard 9% UAE corporate tax [5][9]. These compliance standards also affect banking relationships and can lead to higher operational costs.

"Many entrepreneurs choose where to incorporate based on headlines (low tax rates, fast setup times, or promotional rankings) rather than a comprehensive assessment of long-term business needs." – SIGTAX [5]

The UAE is particularly appealing for trading companies taking advantage of major shipping routes, consulting firms seeking residency perks, and tech founders relocating for 0% personal income tax [5][9]. However, annual compliance costs – covering corporate management, accounting, and regulatory filings – often require professional advisory services [12]. Unlike the UK’s digital-first banking or Singapore’s virtual options, UAE banking demands a more tangible operational presence and extensive documentation [9].

UAE Free Zone Pros and Cons

Here’s a quick look at the key advantages and drawbacks:

| Pros | Cons |

|---|---|

| 0% corporate tax (for qualifying companies) | Higher setup costs ($3,000–$5,000 vs. UK’s ~$100–$150) |

| 0% personal income tax for residents | 9% corporate tax without proper substance |

| Golden Visa residency for founders and families | Requires substantial operational presence |

| VARA licensing for crypto businesses | Banking involves more documentation than digital banking solutions |

| Prime location connecting Europe, Asia, and Africa | Annual compliance costs for professional services |

| Flexible labor laws under Free Zone Authority | VAT at 5% on most goods and services |

| Banking ease rated at 4/5 stars | Less suited for remote-only operations |

Best Use Cases for UAE Free Zone

UAE Free Zones are ideal for international trading firms leveraging proximity to major shipping routes [5]. Consulting and service businesses benefit from the combination of low corporate tax and residency options [5]. Crypto and blockchain companies find a supportive environment through VARA licensing, which provides a regulated framework uncommon in other jurisdictions [9].

Family offices often use the UAE as a hub for managing global investments, similar to other financial centers [5]. Tech founders planning to relocate also gain from the favorable personal tax regime [9]. However, businesses operating fully remotely may find the additional costs of maintaining substance requirements diminish the financial advantages [5][9].

The 0% Tax Reality: Hidden Costs Explained

The headline-grabbing "0% corporate tax" comes with strings attached. While qualifying Free Zone companies avoid the standard 9% UAE corporate tax, adhering to economic substance rules is non-negotiable. This means maintaining physical office space, hiring local staff, and ensuring regular in-person oversight – all of which can add $10,000–$30,000 annually to operational expenses [5][9].

Additionally, businesses generating over AED 375,000 (about $102,000) in revenue are subject to a 5% VAT, requiring quarterly filings and ongoing compliance management [12]. Professional services for corporate management, accounting, and regulatory needs are essential, as non-compliance can result in penalties or loss of tax-exempt status [12].

"Their expert guidance and support helped us navigate complex regulations, maximizing our tax efficiency and ensuring compliance." – Aisha Enterprises [12]

Even banking, rated at 4/5 for ease, demands a medium level of substance verification. Banks closely evaluate whether a business genuinely operates from the UAE, meaning smaller or fully remote operations may struggle to justify the added costs of meeting these requirements. For such companies, the tax benefits may not outweigh the operational expenses.

Payment Processor Access by Jurisdiction

When choosing a jurisdiction for your business, access to payment processors often outweighs considerations like tax rates or formation costs. After all, if you can’t connect your entity to Stripe or PayPal, other benefits might not matter much.

US LLCs are the gold standard for payment gateway compatibility. With an Employer Identification Number (EIN), a US LLC unlocks Stripe’s full US feature set, PayPal Business, and nearly all US-specific payment gateways [8][4]. Non-residents only need to get an EIN for their LLC to get started [8][7]. This is why many UAE-based founders turn to US LLCs to bypass the challenges of local payment processor restrictions [8][4].

"US LLC – hands down. Stripe’s full feature set, PayPal Business, and all US payment gateways require a US entity with an EIN." – OpenEntity [8]

UK LTDs provide seamless access to Stripe UK and PayPal, along with European processors like GoCardless [8][4]. However, they cannot tap into Stripe US or the broader US payment network [4]. For businesses handling USD payments, currency conversion fees of 0.4% to 1.5% per transaction can add up, costing $400 to $1,500 annually on $100,000 in revenue [4]. On the bright side, banking setup is quick – challenger banks like Starling or Tide often approve accounts within 24 hours [1].

Singapore Pte Ltd companies also have reliable access to Stripe and PayPal. However, onboarding with banks can be slower. Traditional banks often require in-person visits, but virtual options like Aspire can speed up the process, typically approving accounts in 3–5 days [1]. On the other hand, UAE Free Zone entities face more challenges with payment processors. Many founders in this region choose to operate a parallel US LLC to simplify payment access [8].

| Jurisdiction | Stripe Access | PayPal Access | Banking Speed | Best For |

|---|---|---|---|---|

| US LLC | Full US Feature Set | PayPal Business (US) | Moderate (e.g., Mercury, Wise) | Global SaaS, USD revenue |

| UK LTD | Stripe UK Only | PayPal Business (UK) | Fast (completed within 24 hours) | UK/EU markets, GBP revenue |

| Singapore Pte Ltd | Stripe Singapore | PayPal Business (SG) | 3–5 days (with virtual banks) | ASEAN markets |

| UAE Free Zone | Limited/Complex | Available | Medium | Often paired with a US LLC |

These payment processor considerations set the stage for the next topic: banking access by entity type, another critical factor for international founders.

Banking Access by Entity Type

Opening a business bank account often turns out to be more challenging than many founders initially anticipate. When evaluating the best jurisdiction for a startup in 2026, banking ease is a key factor, alongside tax and compliance considerations.

UK LTDs offer the simplest banking process for non-residents. Challenger banks like Starling, Tide, and Monzo make the process incredibly straightforward, allowing fully online applications that typically take just 10–15 minutes. Approval is usually granted within 1–2 days[1]. Importantly, there’s no need for a physical visit or for a UK-resident director to attend a branch meeting[1]. This convenience makes UK LTDs a popular choice for international founders, even if their target markets are elsewhere.

US LLCs provide strong banking access, though the process is slightly longer. Fintech platforms such as Mercury, Relay, and Wise Business allow non-residents to apply remotely[4]. However, an Employer Identification Number (EIN) from the IRS is required before starting the application process[4]. Once the EIN is secured, bank account approval typically takes 1–2 weeks[4]. That said, opening a UK bank account for a US LLC is usually not an option, as most UK banks either refuse non-resident directors or require a local branch presence[4].

Singapore Pte Ltd companies face the most hurdles in banking. Traditional banks like DBS, OCBC, and UOB require physical visits and a resident director, which can extend approval times to 2–4 weeks. Virtual banks like Aspire offer a faster alternative, with approval timelines of 3–5 days[1]. For founders unable to travel to Singapore, options include hiring a nominee director service – costing between S$1,500–3,000 annually (roughly $1,100–2,200) – or relying on virtual banking solutions[1].

UAE Free Zone entities fall somewhere in the middle. Banking services are reliable, particularly for high-volume trading firms and family offices, though the process and requirements can vary depending on the bank[5].

"Banking is what actually drives this decision for most UK founders, not tax theory." – Jett Fu, Cross-border entrepreneur, Global Solo[4]

| Jurisdiction | Ease for Non-Residents | Physical Visit Required? | Approval Time | Top Banking Options |

|---|---|---|---|---|

| UK LTD | Very High | No | 1–2 Days | Starling, Tide, Monzo, Wise |

| US LLC | High | No | 1–2 Weeks (post-EIN) | Mercury, Relay, Wise, Airwallex |

| Singapore Pte Ltd | Low to Moderate | Often (Traditional Banks) | 2–4 Weeks (Traditional) / 3–5 Days (Virtual) | DBS, OCBC, UOB, Aspire |

| UAE Free Zone | Moderate | Varies | Varies | Local UAE Banks |

This breakdown of banking access highlights how each jurisdiction supports non-resident founders. With these details in mind, the next step is to examine how these entities align with broader funding strategies, particularly in terms of venture capital opportunities.

VC Funding Preferences by Jurisdiction

In the United States, venture capital firms overwhelmingly prefer Delaware C-Corps. This preference stems from Delaware’s well-established legal framework, including the General Corporation Law (DGCL), which is supported by over two centuries of specialized case law. Additionally, major accelerators like Y Combinator, Techstars, and 500 Global require companies to incorporate as Delaware C-Corps to participate in their programs [13]. Y Combinator’s SAFE (Simple Agreement for Future Equity) is specifically designed for Delaware corporations, further solidifying their dominance in early-stage fundraising [13].

In contrast, UK LTDs are more suitable for local and European investors but can create hurdles for engaging with US venture capital. The UK’s Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS) mandate UK incorporation, which is why UK-based venture capitalists typically expect startups to adopt a UK Ltd structure [4].

"Form a US LLC instead of a UK Ltd, and you’ve locked yourself out of this [SEIS/EIS] capital pool entirely." – Jett Fu, Founder, Global Solo [4]

For founders aiming to secure US venture capital, it’s common to convert a UK Ltd into a Delaware C-Corp. However, this process can be expensive, with legal fees ranging from $5,000 to $25,000 [4]. This highlights how the choice of jurisdiction can significantly influence a startup’s funding strategy.

For startups targeting the Asian market, Singapore Pte Ltds offer distinct advantages. These entities are highly regarded by Asian investors and serve as an effective gateway to ASEAN, China, and India. Singapore’s strong legal framework and 0% capital gains tax make it an attractive option [1]. Many founders operate under a Singapore Pte Ltd for 2–3 years to benefit from tax efficiency before transitioning to a US structure for Series A funding [1].

While Singapore’s structure aligns well with Asian investors, other regions present challenges. For example, UAE Free Zone entities lack the legal and structural standards required by most venture capital firms, making them less suitable for VC-backed startups [2].

The table below summarizes the compatibility and strategies for various jurisdictions:

| Jurisdiction | US VC Compatibility | Regional VC Compatibility | Key Investor Benefit | Common Strategy |

|---|---|---|---|---|

| Delaware C-Corp | Universal standard | High globally | QSBS (up to $10M tax-free gains) [13] | Incorporate early if US VC is the goal |

| UK Ltd | Limited | High (UK/EU) | SEIS/EIS tax relief [4] | Start in the UK, then convert to Delaware |

| Singapore Pte Ltd | Moderate | High (Asia-focused) | 0% capital gains tax [1] | Operate for 2–3 years, then convert |

| UAE Free Zone | Very low | Low | 0% corporate tax [2] | Not aligned with VC standards |

Tax Residency vs Company Residency: What You Need to Know

Company residency refers to the location where your business is legally incorporated – whether that’s Delaware, London, Singapore, or Dubai. On the other hand, personal tax residency is tied to where you live and pay income taxes. Mixing up these two concepts can lead to costly mistakes.

Many countries tax their residents on worldwide income, regardless of where the company operates [4]. For example, if you’re a UK resident running a Singapore Pte Ltd, you’re still liable for personal taxes on dividends, even though Singapore has no dividend tax [1][4]. Similarly, if you’re a UK resident with a US LLC as a non-resident, HMRC will tax the distributions you receive [4].

Grasping the difference between these two types of residency is essential when assessing how your business structure impacts your tax obligations.

This distinction becomes even trickier due to classification mismatches. For instance, the IRS treats a single-member US LLC as a pass-through entity, while HMRC views it as opaque. This difference can result in double taxation, as neither country fully credits taxes paid to the other [4].

"HMRC doesn’t care what the IRS thinks… The practical result: neither country gives full credit for tax paid to the other, because each views the entity differently." – Jett Fu, Cross-border entrepreneur, Global Solo [4]

Another key factor is how your company is managed. Beyond residency, tax authorities now focus heavily on economic substance rules. If a company is registered in one jurisdiction but effectively managed from another (like a Singapore company run from London), it could be reclassified as tax-resident in the manager’s country under Controlled Foreign Company (CFC) rules [4]. To avoid this, your company must demonstrate real management, decision-making, and operations within its registered jurisdiction [5]. Failure to meet these requirements – such as neglecting to file Form 5472 – can lead to severe penalties, reaching up to $25,000 per form [4].

5 Founder Scenarios: Which Jurisdiction to Choose

The examples below highlight how personal tax residency, business type, and market goals influence the best jurisdiction for a business.

| Founder Profile | Tax Residency | Recommended Jurisdiction | Why This Works | Estimated Annual Cost |

|---|---|---|---|---|

| Nigerian SaaS developer selling globally via Stripe | Nigeria | US LLC (Wyoming) | No US federal tax on non-US-source income, full Stripe US access, remote banking via Mercury/Wise | ~$708/year ($499 setup + $209 annual) |

| Dubai-based consultant serving Middle East and Europe | UAE | UAE Free Zone + UK LTD (dual structure) | 0% personal tax in UAE, UK LTD adds European credibility and VAT compliance | UAE: $3,400–$6,800 setup; UK: £12–£83 setup + £834–£1,534/year |

| US-based e-commerce entrepreneur selling internationally | United States | Delaware C-Corp (for VC funding) or Wyoming LLC (for bootstrapping) | C-Corp suits Series A+ funding; LLC offers pass-through taxation but may need costly conversion later | LLC: ~$610–$2,210/year; C-Corp: ~$300/year franchise tax |

| UK resident targeting ASEAN markets | United Kingdom | Singapore Pte Ltd | 4.25% effective tax rate for 3 years, high S$1M GST threshold, 0% dividend tax | ~£696 setup + £1,195–£2,239/year (includes mandatory secretary/nominee) |

| Indian freelancer working with US and UK clients | India | UK LTD | Fast setup (24 hours), low-cost formation, remote banking options (Starling, Tide), UK address | £12–£83 setup + £145–£1,500/year |

Why These Jurisdictions Make Sense

For the Nigerian SaaS developer, a US LLC is ideal because it provides unrestricted access to US payment systems, crucial for a global SaaS business. The lack of federal tax on non-US-source income further solidifies this choice.

The Dubai-based consultant benefits from a dual structure. A UAE Free Zone ensures 0% personal tax, while a UK LTD enhances trust and compliance in European markets through VAT registration.

The US e-commerce entrepreneur has different needs depending on funding goals. A Delaware C-Corp accommodates venture capital funding, while a Wyoming LLC is more cost-effective for self-funded ventures. However, converting an LLC to a C-Corp later can incur significant legal costs.

For the UK resident targeting ASEAN markets, Singapore’s favorable tax policies, including a low effective tax rate and a high GST threshold, make it a strategic choice. However, UK residents still face HMRC taxation on distributions, which should be considered.

The Indian freelancer finds value in a UK LTD due to its quick and inexpensive setup, along with easy access to remote banking and a professional UK address. While they will encounter UK corporation tax, the operational benefits outweigh the downsides.

Key Takeaway

These scenarios show how aligning business jurisdiction with personal tax residency and business strategy can significantly enhance both operational efficiency and financial outcomes. Each case demonstrates that the right jurisdiction depends on a careful balance of tax advantages, market access, and long-term business goals.

Conclusion: How to Choose the Right Jurisdiction

Bringing together the key points from our comparisons, picking the best jurisdiction for your business isn’t just about minimizing costs – it’s about finding the right fit for your company’s structure, market goals, and growth potential. As SIGTAX aptly puts it, "The critical question, therefore, is not ‘Where is tax lowest?’ but: Where will this company operate most effectively and grow most sustainably?" [5]

The first step is to think about your customer base. For instance, if your focus is on US customers and you’re selling SaaS globally, setting up a US LLC gives you access to digital-first payment gateways and remote banking options. On the other hand, if your target is European B2B clients, a UK LTD offers VAT registration and credibility within the region. Meanwhile, for businesses aiming at ASEAN markets, a Singapore Pte Ltd is the go-to option [1][4].

Your funding strategy is another crucial factor. If you’re seeking UK investors, they often prefer a UK LTD to take advantage of SEIS/EIS tax reliefs. US venture capitalists, however, typically expect a Delaware C-Corp. For those bootstrapping, both a US LLC and a UK LTD provide lower compliance costs and operational flexibility, making them practical choices [4][5].

Banking and payment processing can also be a deciding factor. These logistics often outweigh tax considerations. As cross-border entrepreneur Jett Fu explains, "Banking is what actually drives this decision for most UK founders, not tax theory" [4]. Entities in the US and UK tend to offer smoother remote banking setups through platforms like Mercury, Starling, and Wise, which can simplify operations [1][4].

Lastly, think about how your personal tax residency interacts with your company’s structure. For instance, UK residents forming US LLCs need to be mindful of classification issues, as discussed earlier. When profits surpass £100,000–£200,000, the tax benefits of a Singapore entity or a US LLC may outweigh their higher compliance requirements [1][4].