If you work in your S-corp, I’d pay myself a W-2 salary first and make sure it matches the job I actually do. Then I’d take distributions only after that. That’s the core rule.

Here’s the short version:

- There is no IRS safe percentage

- Salary should match market pay for similar work

- W-2 wages face payroll tax; distributions do not

- Low salary + high distributions can trigger IRS review

- Good records and regular payroll matter

- I’d review the number at least once a year

A court case made this clear: in Watson v. Commissioner, an owner took $24,000 in salary while the court said $93,000 was the right number based on market pay. That gap led to wage reclassification and more tax.

What I take from this article is simple: reasonable salary is not a guess. It should be tied to my duties, hours, experience, local pay data, and the company’s finances.

If I wanted a clean way to handle it, I’d do this:

- List the work I do

- Estimate my hours and time split

- Check local wage data

- Set a salary I can support

- Run payroll during the year

- Keep notes, forms, and pay records

This article’s main point is clear: pay yourself like an employee first, not like an owner only taking distributions.

The Problem: Low Salary, High Distributions, and IRS Red Flags

The mistake that trips up many S-corp owners is simple: they pay themselves little or no W-2 salary, then take most of the cash as distributions. That can backfire fast. Under Revenue Ruling 74-44, the IRS can reclassify those distributions as wages.

If that happens, the tax bill can sting. The IRS may assess back payroll taxes on the amount it reclassifies, including both the employer and employee sides of FICA. It may also assess payroll tax, penalties, and interest. In more serious cases, civil fraud penalties and personal liability for the employee share can apply under IRC §6672.

What the IRS Looks At When Your Salary Seems Too Low

The IRS doesn’t use a fixed formula here. It looks at the full picture using a facts-and-circumstances test built around six factors:

| IRS Factor | What the IRS Examines |

|---|---|

| Duties & Responsibilities | The nature and scope of services the shareholder actually performs |

| Hours Worked | How much time the shareholder devotes to running the business |

| Market Comparables | What comparable businesses pay for similar services in the same market |

| Experience and Credentials | The shareholder’s training, credentials, and years of experience |

| Company Profitability | The financial condition and overall profitability of the S-corp |

| Non-Shareholder Pay | Pay for non-owner employees doing similar work |

Those are the same factors you should use when setting a salary that can hold up under review.

Two things tend to stand out for the wrong reasons. No salary at all is an obvious red flag. And a single payroll run at year-end can also look weak to the IRS.

In Glass Blocks Unlimited v. Commissioner, the sole shareholder took no salary in 2007 and 2008 while taking distributions. The Tax Court rejected the loan characterization because the paperwork was missing and reclassified the payments as wages subject to employment taxes.

Why Rules of Thumb Like ‘50% of Profit’ Can Mislead You

A lot of owners look for a shortcut, like paying themselves 50% of profit. The problem? The IRS has never endorsed a percentage-based safe harbor.

Sean McAlary Ltd., Inc. v. Commissioner shows why that matters. In that case, a real estate broker reported $0 in wages while taking $240,000 in transfers. The Tax Court looked to regional wage data and reclassified $83,200 as wages.

That’s the heart of it: this isn’t a guessing game, and it’s not about plugging profit into a rule of thumb. The better path is to base salary on the work you do, the time you put in, and what the market pays for that role.

How to Set a Reasonable Salary for an S-Corp Owner

Once you know the IRS looks at the facts and circumstances, the next step is to set a salary you can back up if anyone asks.

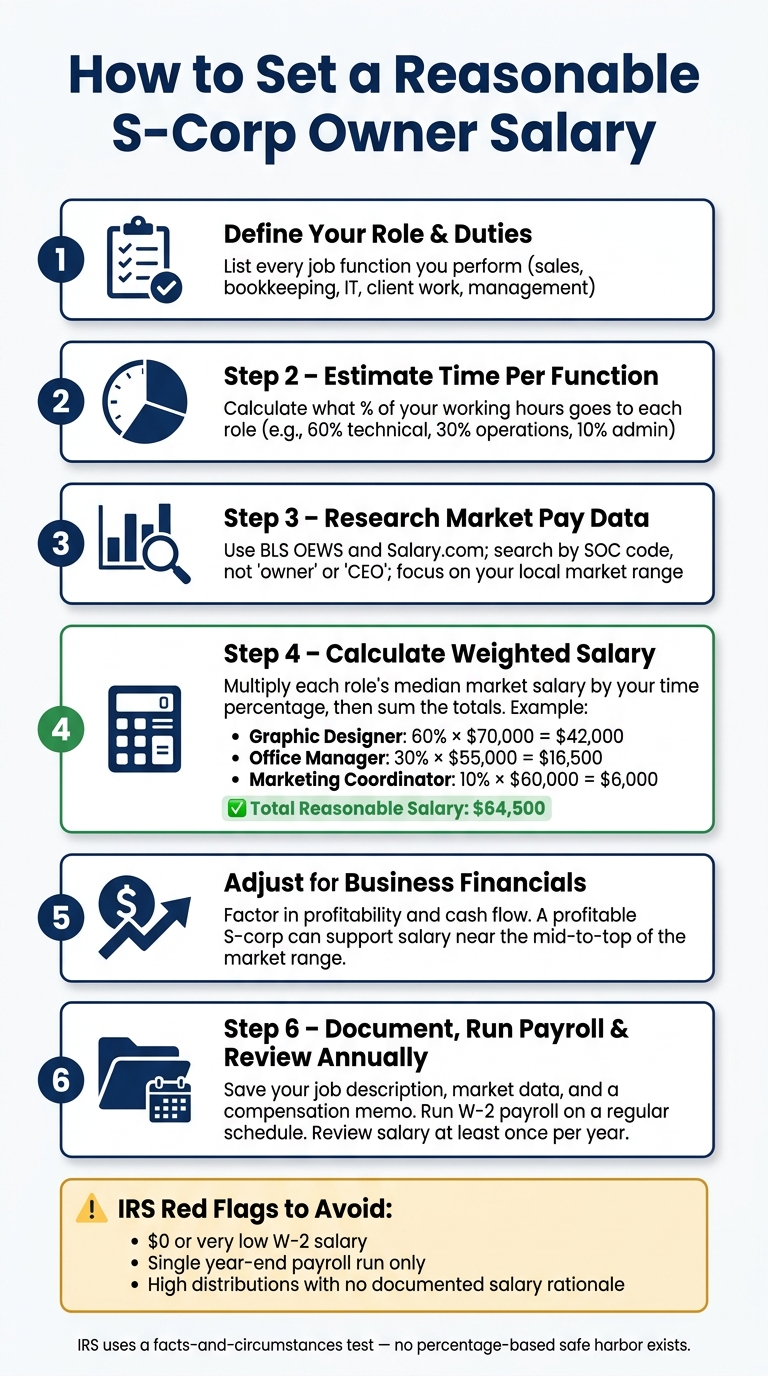

Start With Your Actual Role, Duties, and Hours Worked

Start with the work itself, not with a dollar figure. Write down each job you handle in the business: sales, client work, bookkeeping, employee management, and IT support. Then estimate how much of your working time goes to each one.

If you work part-time, your salary will usually be lower than it would be for a full-time role. It helps to group your work into job functions. So if you spend 60% of your time on technical work, 30% on operations, and 10% on admin tasks, you’d match each function to local market pay and build your salary from there.

Use Market Data From BLS and Salary Research Tools

Use BLS OEWS and Salary.com to compare pay for the same kind of work in your area. IRS examiners use BLS data, and Tax Court has relied on it in cases like Watson v. Commissioner. Search by Standard Occupational Classification (SOC) code instead of using a broad title like "owner" or "CEO."

Stick with the local market range. In many cases, the middle of that range is the safest place to aim.

A simple way to do this is to multiply the median market salary for each function by the share of time you spend on it, then add those weighted amounts together. Here’s a hypothetical example:

| Role | % of Time | Comparable Salary | Weighted Value |

|---|---|---|---|

| Graphic Designer | 60% | $70,000 | $42,000 |

| Office Manager | 30% | $55,000 | $16,500 |

| Marketing Coordinator | 10% | $60,000 | $6,000 |

| Total Reasonable Salary | 100% | – | $64,500 |

Hypothetical example of the "Many Hats" Cost Approach [8]

That gives you a salary range based on what you do, how much you work, and what similar jobs pay in your local market before you take distributions.

Adjust for Profitability, Cash Flow, and Business Stage

After you have a market range, look at the company’s finances to decide where your pay should fall inside that range. A profitable S-corp with solid cash flow can support a salary near the middle or top end of the market range.

For example, an IT services business with $350,000 in net income has an illustrative salary range of $100,000 to $160,000, which you can then adjust based on your own duties and local market conditions.

That range is the number you should document and review each year.

Save the inputs you used. If the IRS ever takes a look, you’ll want to show how you arrived at the salary in the first place.

sbb-itb-ba0a4be

How to Document Your Salary and Stay Compliant Year-Round

Once you set your salary, put it in writing and run it through payroll. That paper trail matters. If the IRS asks how you came up with the number, you want records that were created at the time, not something pulled together after the fact. This matters even more when a return shows low wages and high distributions, because that pattern can draw attention from the IRS.

Keep a Written Salary File With Market Data and Job Details

Keep one folder, either digital or paper, with the records you used to set your salary. That file should include your job description, notes on how you spend your time, market pay data, and a short memo that explains the final salary number.

It also helps to add a written compensation memo or board resolution at the start of each year. That document should record the salary decision and explain the method you used to reach it. Records made before an audit carry much more weight than records built later.

That said, paperwork alone isn’t enough. Your payroll has to match what those records say.

Run Payroll Before Taking Distributions

Pay your W-2 salary through payroll on a regular schedule. Withhold payroll taxes first, then take shareholder distributions. Distributions are not a stand-in for salary, and skipping payroll can lead to reclassification risk.

Your payroll file should include:

- Quarterly Forms 941

- Annual Form 940

- Your year-end W-2

If you’re a more-than-2% shareholder and you pay your own health insurance premiums, those premiums need to be included in Box 1 wages on your W-2.

Review Your Salary at Least Once a Year

Review your salary file at least once a year. Go back to it sooner if your duties shift in a big way, revenue climbs, or you start putting in more hours. If you need to make a change, do it before your final payroll run so your W-2 stays accurate.

Keep a running note for each yearly review that shows what changed, what data you checked, and what adjustment you made. A salary that made sense before can get harder to defend if your role gets bigger or profits climb a lot. That kind of record shows a steady review process and keeps your file lined up with changes in duties and revenue.

Conclusion: Set a Defensible Salary Before Taking S-Corp Distributions

Bottom line: a reasonable salary is the market rate for the work you personally do. Pay that first, then take shareholder distributions.

If you set your salary too low and take most of the money as distributions, you can run into back taxes, penalties, interest, and personal liability for payroll taxes. That’s why it makes sense to document your salary and review it before any distributions go out.

The Watson v. Commissioner case shows what can happen when an owner underpays themselves. The IRS can reclassify distributions as wages, which can lead to back taxes, penalties, and interest. The safest move is to set pay based on your duties, market data, and time worked before taking distributions.

FAQs

How low is too low for an S-corp salary?

An S-corp salary is too low when it falls well below the market rate for the work you do. There isn’t an official percentage or a safe-harbor formula you can lean on.

The IRS looks at what an unrelated employer would pay for your role, based on your duties, experience, and location. If you pay yourself too little while taking large distributions, the IRS may treat those distributions as wages instead.

That can lead to back taxes, interest, and penalties.

Can I change my salary during the year?

Yes, but make changes with care so they don’t look like income manipulation. Retroactive changes, or pay that jumps around for no clear reason, can draw IRS attention.

To stay compliant, set your salary ahead of time and document it. Back it up with market data. If your finances or role change in a major way, keep a written record that explains the adjustment before it takes effect.

What records should I keep for salary?

Keep a current file that supports your salary, and update it each year before your last payroll run.

That file should include:

- Your job description

- Your credentials

- Estimated hours by function

- Salary benchmark data

- Board minutes or a resolution that sets pay

- Your compensation agreement

- Payroll records, such as W-2s and Form 941s

- A dated annual review memo that explains your reasoning

Think of it as your paper trail. If someone asks why your salary is set at that level, you want the answer in writing and easy to follow.