Owning real estate through an LLC is a smart way to protect your personal assets and maximize tax benefits. By separating your personal finances from your investments, an LLC shields you from liabilities like lawsuits and debts tied to your properties. It also simplifies tax reporting and provides privacy by listing the LLC’s name in public records instead of your own.

Here’s why real estate investors choose LLCs:

- Liability Protection: Your personal savings and assets are safe if legal issues arise.

- Tax Perks: Pass-through taxation avoids double taxation, and rental income often qualifies for a 20% QBI deduction.

- Privacy: Public records show the LLC’s name, not yours, reducing legal risks.

- Flexibility: Manage multiple properties with clearer financial separation.

To get started, you’ll need to:

- File Articles of Organization in your state.

- Transfer property titles into the LLC’s name, even after closing.

- Keep finances and operations strictly separate to maintain liability protection.

Proper management, such as using separate bank accounts and maintaining compliance with state filings, ensures your LLC remains effective. Pairing your LLC with insurance coverage adds another layer of security, protecting both the business and your property investments.

Key Benefits of Holding Real Estate in an LLC

Liability Protection and Asset Separation

Using an LLC to hold real estate offers a powerful layer of protection by keeping your personal and business assets separate. When a property is owned by an LLC, it becomes its own legal entity. This means that if something goes wrong – like an accident or a lawsuit – only the LLC’s assets are at risk, not your personal savings or property. This separation, often called the corporate veil, is what shields your personal wealth from business-related liabilities.

"The core reason investors hold rental property in an LLC is the liability shield. If a tenant gets injured on the property… creditors can only go after assets owned by the LLC itself." – LegalClarity Team

Here’s a real-world example: In May 2026, a landlord in Phoenix, Arizona, faced a $180,000 lawsuit after a tenant suffered a serious fall. Because the landlord owned all three of her rental properties in her personal name, the judgment put her personal savings, primary residence, and the equity in her other rentals at risk.

Another advantage is that creditors’ remedies are limited by a charging order, which restricts them to future distributions from the LLC rather than its current assets.

Tax Advantages and Flexibility

An LLC doesn’t just protect your assets – it can also offer significant tax benefits and flexibility.

For starters, a single-member LLC is typically taxed as a disregarded entity. This means rental income flows directly to your personal tax return via Schedule E, avoiding the double taxation that C-corporations face. Plus, rental income is classified as passive income, so it’s not subject to the 15.3% self-employment tax.

LLCs also allow you to take advantage of tax deductions that go beyond what’s available with personal ownership:

| Tax Benefit | Personal Ownership | LLC |

|---|---|---|

| Mortgage Interest | Capped at a $750,000 balance | No cap for rental properties owned by an LLC |

| Property Tax Deduction | Limited to $10,000 (SALT cap) | Fully deductible as a business expense |

| QBI Deduction (20%) | Not available | Available for qualifying rental activity |

| Depreciation | Limited | Full 27.5-year residential schedule |

For investors earning higher profits, electing S-Corp taxation for your LLC can lead to even greater savings. Take this example: In February 2026, a dentist in Cheyenne, Wyoming, transferred three rental properties worth $1.2 million into a Wyoming LLC taxed as an S-Corp. She paid herself a $35,000 salary and took $50,000 as distributions, reducing her self-employment tax from $13,050 to $5,355. This restructuring saved her $13,195 in taxes during the first year alone.

On top of these tax perks, an LLC makes it easier to manage your finances, keeping everything streamlined and organized.

Simplified Recordkeeping and Operations

An LLC simplifies the operational side of real estate investing. Since the LLC is a separate entity, it has its own bank account and handles its own income and expenses. This makes bookkeeping much easier – you always know exactly what each property is earning and spending. It also makes tax preparation more straightforward because your financial records are already separated.

One critical point: commingling funds can jeopardize your liability protection. For example, depositing a rent check into your personal account – even once – could lead a court to strip away your LLC’s legal shield. To avoid this, maintain a dedicated business account for each LLC and ensure all property-related transactions go through it. Keeping these boundaries clear strengthens your liability protection and ensures compliance.

sbb-itb-ba0a4be

Single LLC vs. Multiple LLCs: How to Structure Your Portfolio

Once you’ve set up your LLC and separated your finances, the next step is figuring out how to structure your portfolio. Should you stick with one LLC or create multiple? The answer depends on factors like the number of properties you own, the equity you’ve built, and the level of risk associated with each property. Your decision here can play a big role in managing risk and shaping your financial strategy.

Factors to Consider When Choosing a Structure

One of the biggest downsides of using a single LLC is the risk of cross-collateralization. If all your properties are under one LLC, a lawsuit involving one property could potentially put the equity in your other properties at risk.

"If all of your properties are owned by a single LLC, that firewall only works in one direction. A claim against Property A can potentially reach the equity in Properties B, C, and D since they’re all owned by the same entity." – Davis Law Group

Experts often recommend setting up a new LLC when the combined equity in one LLC approaches $1 million or when you’re managing more than two or three properties. The additional cost of forming multiple LLCs is often worth the extra layer of protection.

Instead of creating an LLC for every property, you can group properties by risk level. For instance, high-liability properties like short-term rentals, student housing, or those with pools could be placed in their own LLC. This way, if something goes wrong with one high-risk property, the fallout is contained.

Geography also plays a role. If your properties are in different states, you might need separate LLCs to comply with state laws. Otherwise, you’ll have to register your LLC as a foreign entity in each state where you operate, which adds fees and paperwork.

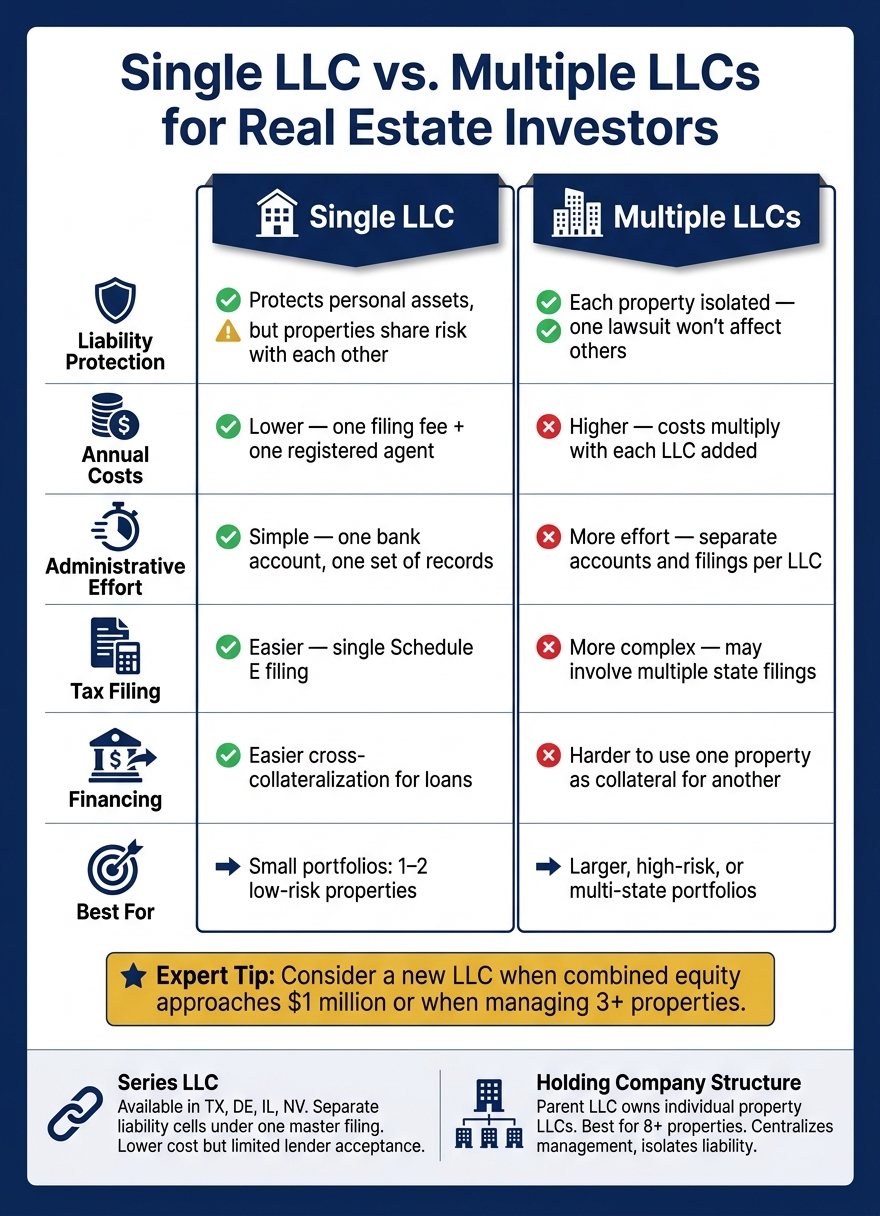

Single LLC vs. Multiple LLCs: A Side-by-Side Comparison

Here’s a quick breakdown of the pros and cons of using a single LLC versus multiple LLCs:

| Feature | Single LLC | Multiple LLCs |

|---|---|---|

| Liability Protection | Protects personal assets, but properties aren’t shielded from each other | Isolates each property; one lawsuit won’t affect others |

| Annual Costs | Lower – one set of filing fees and a single registered agent | Higher – costs increase with each LLC |

| Administrative Effort | Simpler – one bank account and one set of records | More effort – separate accounts and filings for each LLC |

| Tax Filing | Easier – single-member LLCs file with Schedule E | More complex – may involve multiple state filings |

| Financing | Easier to cross-collateralize properties for loans | Harder to use one property as collateral for another in a separate LLC |

| Best For | Small portfolios with 1–2 low-risk properties | Larger, high-risk, or multi-state portfolios |

Another option to consider is the Series LLC, available in states like Texas, Delaware, Illinois, and Nevada. A Series LLC allows you to create separate "cells" under a single master LLC filing. Each cell operates like its own LLC, isolating liability between properties, but often at a lower cost than forming multiple LLCs. The catch? Not all states recognize Series LLCs, and some lenders won’t close loans under individual series names.

If your portfolio grows to eight or more properties, you might want to explore a holding company structure. In this setup, a parent LLC owns individual property-level LLCs. This centralizes management while keeping liability for each property separate. While it adds complexity, it’s a practical solution for managing larger portfolios.

How to Form a Real Estate LLC: A Step-by-Step Guide

Once you’ve determined that an LLC is the best structure for your real estate portfolio, it’s time to set it up. The process is pretty straightforward, but every step is important. Skipping anything could lead to unnecessary complications or even leave you vulnerable down the road.

Choosing a Name and Filing Articles of Organization

The first step is picking a name for your LLC. Make sure it’s unique and includes a legal designator like "LLC" or "Limited Liability Company." To avoid any issues, check your state’s Secretary of State database to confirm the name is available. For privacy reasons, avoid using your personal name. A generic name like "Oak Ridge Properties LLC" works well, as it helps keep your personal details out of public property records.

Once you’ve settled on a name, file your Articles of Organization in the state where the property is located. This document officially establishes your LLC and includes key details like the business name, address, registered agent information, and management structure. Filing in the same state as the property avoids the extra costs and paperwork tied to registering as a foreign entity.

Filing fees vary by state, ranging from $35 to $500. For instance, Montana charges $35, Wyoming $100, and Massachusetts $500.

After completing this step, you’ll need to appoint a registered agent and secure an EIN.

Appointing a Registered Agent and Obtaining an EIN

Every LLC is required to have a registered agent. This can be an individual or a professional service with a physical address in the state. The registered agent receives important documents like legal notices and tax forms on behalf of the LLC. Using a professional service, which typically costs between $39 and $300 annually, has the added benefit of keeping your personal address off public records and ensuring reliable handling of correspondence during business hours.

Once your Articles of Organization are filed, you’ll need to get an EIN (Employer Identification Number). This is a federal tax ID for your LLC, and you can apply for it free on the IRS website – it takes about 15 minutes. An EIN is essential for opening a business bank account.

"The single most common reason LLC liability protection fails is also the most avoidable: commingling personal and business funds." – TopBestLLCService.com

Also, don’t forget about the Corporate Transparency Act. Most LLCs must now file a Beneficial Ownership Information (BOI) report with FinCEN, a newer compliance requirement that’s easy to overlook.

Drafting an Operating Agreement

With the LLC legally established, the next step is creating an operating agreement. While you don’t need to file this document with the state, it’s a critical internal tool. It spells out ownership percentages, how profits and losses are shared, who handles daily operations, and what happens if a member leaves or the LLC dissolves.

For real estate investors, the agreement should also include:

- Authority for refinancing (who can take out loans)

- Procedures for capital calls

- Steps for acquiring or selling properties

Many banks will ask for a copy of your operating agreement before allowing you to open a business account. You can find free templates online, but a customized agreement drafted by a real estate attorney – typically costing $500 to $2,000 – is often worth the investment, especially if you co-own properties. It’s far cheaper than dealing with disputes in court later.

If you want a more affordable option but still need something tailored, BusinessAnywhere offers an Operating Agreement Template for $97.

How to Transfer Property Titles to an LLC

Forming an LLC is just the beginning; you also need to legally transfer property into the LLC’s name to activate its liability protection. Real estate attorney Teresa R. Martin emphasizes:

"Forming an LLC does not transfer the rental property into the LLC… It is an actual legal transaction. It is not an administrative side note." – Teresa R. Martin, Esq.

Here’s how you can handle the transfer process effectively.

Steps to Transfer Property Titles

If you’re transferring property from your personal name to your own LLC, a quitclaim deed is usually sufficient. This type of deed transfers your ownership interest without providing guarantees about the title. However, if other partners or investors are involved, a warranty deed might be necessary to confirm the title is free of liens or disputes.

Here’s what you need to do:

- Prepare the Deed: Create a new deed that lists you as the grantor and the LLC as the grantee. Be sure to use the LLC’s full legal name.

- Notarize the Document: Sign the deed and have it notarized.

- Record the Deed: File the notarized deed with your local county recorder’s office. Recording fees can range from $25 to several hundred dollars, depending on the location.

- Update Insurance and Contracts: Revise insurance policies, leases, utility accounts, and vendor agreements to reflect the LLC as the property owner.

- Transfer Related Assets: Move any personal assets tied to the property – such as appliances or lease rights – into the LLC through a bill of sale.

Additionally, notify tenants in writing about the change. Let them know the LLC is now the landlord and provide updated details for rent payments, including the LLC’s bank account information.

Mortgage and Tax Considerations

Once the deed transfer is complete, you’ll also need to address potential mortgage and tax implications:

- Mortgage Issues: Most mortgages include a "due-on-sale" clause, allowing the lender to demand full repayment if the property title is transferred. This clause may be triggered when transferring to an LLC, so it’s crucial to get written approval from your lender before proceeding. Keep in mind that the Garn-St. Germain Act doesn’t protect transfers to LLCs. However, if your mortgage is backed by Fannie Mae or Freddie Mac, their guidelines often permit transfers to an LLC without triggering the clause, as long as you maintain at least 51% ownership of the LLC.

- Tax Impacts: For single-member LLCs, transferring a property is generally tax-neutral because these entities are disregarded for federal tax purposes. Multi-member LLCs, treated as partnerships, may require additional filings and have different tax consequences.

The table below highlights key considerations when transferring property titles to an LLC:

| Consideration | Transfer Implications |

|---|---|

| Mortgage | Could activate a due-on-sale clause, requiring full repayment. |

| Property Tax | May result in reassessment to current market value in some states. |

| Income Tax | Typically tax-neutral for single-member LLCs. |

| Insurance | Personal policies need to be updated to list the LLC as the insured party. |

| Section 121 | Loss of primary residence capital gains exclusion (up to $250,000/$500,000). |

If you’re transferring a primary residence, be aware that you may lose the homestead exemption and the Section 121 exclusion, which can shield up to $250,000 (single filers) or $500,000 (married couples) in capital gains. This makes transferring a primary residence less practical compared to investment properties, where this strategy is more beneficial.

Keeping Your LLC’s Finances and Operations Separate

After transferring property titles properly, the next step is ensuring a clear separation between your LLC’s finances and your personal accounts. This isn’t just about staying organized – it’s essential for maintaining the liability protection your LLC provides.

Best Practices for Financial Separation

Start by opening a dedicated business checking account for each LLC using its EIN. Avoid mixing personal and business transactions. Every expense – whether it’s rent payments, repairs, or vendor invoices – should go through this account. Keeping finances separate reinforces the legal distinction between you and your LLC.

When signing documents, always use your LLC title, such as "Member" or "Manager." This step protects your personal liability. Attorney David J. Willis emphasizes the importance of this practice:

"The goal should be to make sure the payee is always the management LLC, never the investor personally and never the holding LLC."

For those managing multiple properties or expanding their portfolio, a two-company structure can offer added protection. In this setup, a Management LLC handles the day-to-day tasks like collecting rent, hiring contractors, and signing leases. Meanwhile, a separate Holding LLC owns the property titles. Because tenants and vendors interact only with the Management LLC, the Holding LLC remains shielded from direct legal exposure. This structure not only strengthens your asset protection but also simplifies operations.

Another tip: keep the cash balance in your operating LLC low. Any funds exceeding $25,000 should be transferred to a separate holding entity. By reducing the cash available in the LLC that faces public liability, you minimize potential exposure in case of legal issues.

While these steps help safeguard your LLC, staying alert to common missteps is equally important.

Common Mistakes to Avoid

One major mistake is neglecting corporate formalities. Even single-member LLCs need to maintain annual meeting minutes and a written operating agreement. These documents prove your LLC operates as a legitimate business, not just a legal formality.

Another pitfall is disorganized bookkeeping. Poor record-keeping can lead to missed tax deductions, costing you 8–15% in potential savings. Worse, reconciling messy finances could result in CPA fees ranging from $1,500 to $3,500.

To avoid these issues, keep thorough records. Here’s a quick guide to the key documents your LLC should maintain and how long to keep them:

| Record Type | Purpose | Retention Period |

|---|---|---|

| Settlement Statements (HUD-1) | Establishes property basis | Until sold + 7 years |

| Capital Improvement Receipts | Adjusts basis/depreciation | Until sold + 7 years |

| Tenant Rent Rolls | Income substantiation | 7 years |

| Bank/Credit Card Statements | Audit trail | 7 years |

| Mileage Logs | Substantiates auto deductions | 4 years |

Tax and Compliance Requirements for Real Estate LLCs

Staying compliant is just as important as keeping your finances in order when it comes to protecting your LLC. Following these requirements helps preserve the legal and tax benefits tied to your business.

Annual State Filings and Licenses

Most states require LLCs to submit an annual report (also referred to as a periodic report or biennial statement) to the Secretary of State. These reports don’t involve financial details but instead confirm your LLC’s address, registered agent, and member information. Missing this filing can result in administrative dissolution, which removes your LLC’s legal protections.

"Administrative dissolution means your entity is legally defunct… LLC members or corporate shareholders can be held personally liable for business debts." – SMBRegs Editorial Team

The rules, fees, and deadlines for these filings vary by state. For example, California imposes an $800 annual franchise tax regardless of income, while states like Arizona, Missouri, New Mexico, and Ohio don’t require annual reports at all. Florida’s deadline is May 1, and filing even a day late results in a $400 late fee. To avoid penalties, set reminders: one 60 days before the due date to check fees and another 30 days before to file. Once submitted, verify your LLC’s status as "Active" or "Good Standing" on your state’s business registry within 1–3 days.

| State | Annual Fee | Late Penalty |

|---|---|---|

| California | $20 (biennial) + $800 tax | $250 + potential suspension |

| Florida | $138.75 | $400 supplemental fee |

| Massachusetts | $500 | Administrative dissolution |

| Nevada | ~$350 | $150 + revocation |

| Texas | $0 (if revenue < $2.47M) | 5%–10% penalty |

| Wyoming | $60 minimum | $50 + administrative dissolution |

While state filings are essential for maintaining local compliance, federal tax obligations bring another layer of requirements.

Federal Tax Filing Requirements

Federal tax filing for your LLC depends on its structure. A single-member LLC is treated as a disregarded entity, with rental income reported on Schedule E. In contrast, a multi-member LLC must file Form 1065 and issue Schedule K-1 forms to each member, outlining their share of profits and losses. The deadline for Form 1065 is March 16, 2026, one month before personal tax filings.

Failing to file Form 1065 on time triggers a $220 monthly penalty per partner. For a four-member LLC, that’s $880 per month in late fees. Rental income is typically classified as passive under Section 469, meaning losses can only offset other passive income – unless you qualify as a Real Estate Professional by logging at least 750 hours of real estate activity annually.

Two major tax benefits have been confirmed for 2026. The One Big Beautiful Bill Act (OBBBA) permanently reinstated 100% bonus depreciation, allowing investors to deduct the full cost of qualifying improvements in the first year. Additionally, the 20% Qualified Business Income (QBI) deduction remains available for eligible pass-through owners. To safely claim the QBI deduction, you’ll need to document at least 250 hours of real estate service activity annually.

If your LLC doesn’t yet have an EIN, you can apply for one for free at IRS.gov. This step is essential for opening business bank accounts and maintaining the separation between your personal and business finances.

Insurance and Risk Management for Real Estate LLCs

An LLC offers a shield by restricting which assets creditors can access, but it doesn’t cover legal expenses. That’s where insurance steps in. Together, they create a two-pronged defense: the LLC defines what’s at risk, while insurance handles legal costs and settlements. This combination ensures that while your LLC provides structural protection, insurance reduces the financial strain of legal claims.

"The LLC and insurance protect against different things. The LLC prevents a judgment from reaching your personal assets. Insurance pays the claim so the LLC’s assets – your rental property – don’t get consumed by it." – LegalClarity Team

Insurance Policies Every Real Estate LLC Should Have

The cornerstone of protection is landlord insurance. It covers the property itself, liability for injuries on-site, and lost rental income. Costs typically range from $800 to $2,000 per year per property. Once a property is under an LLC, your personal homeowner’s policy no longer applies. Instead, you’ll need a commercial landlord policy listing the LLC as the insured.

An umbrella policy acts as an additional layer, increasing liability coverage by $1 million to $5 million. This extra protection usually costs between $150 and $300 annually for each $1 million in coverage. For context, slip-and-fall settlements often fall between $10,000 and $50,000, while severe injury claims can exceed $100,000.

Title insurance is another critical, yet often overlooked, policy. Transferring a property into an LLC may void your personal title insurance. Before recording the deed, contact your title company to either update the policy to include the LLC or secure a new one in the LLC’s name.

Having these policies in place is only part of the equation. It’s equally important to understand how they work in tandem with your LLC structure.

How Insurance Works Alongside an LLC

Your LLC limits creditors’ access to personal assets, but insurance is what addresses legal fees and claims. Together, they create a layered safety net. Insurance takes care of immediate costs, the LLC provides a legal barrier, and your personal savings remain untouched.

"An LLC is not a substitute for landlord insurance. Insurance pays first and covers legal defense costs. The LLC is the backup protection." – Shepherd Nyakudya, Founder, USLLCGlobal

Critical steps include activating a commercial landlord policy under the LLC’s name and ensuring you have written confirmation of its start date before recording the deed. This avoids coverage gaps.

It’s also important to note that an LLC won’t protect you from personal negligence. For example, ignoring a known hazard like a broken railing or a faulty smoke detector could lead to personal liability, regardless of the LLC structure.

| Protection Layer | What It Does | What It Doesn’t Do |

|---|---|---|

| Landlord Insurance | Covers legal defense and settlements up to limits | Won’t protect personal assets if claims exceed policy limits |

| Umbrella Policy | Extends liability coverage by $1M–$5M | Doesn’t separate personal and business assets legally |

| LLC Structure | Shields personal savings and investments | Doesn’t cover legal costs or personal negligence |

Tools and Services to Manage Your Real Estate LLC

Keeping your LLC running smoothly requires staying on top of daily tasks and avoiding legal missteps. Missing important filings or compliance checks can put your LLC at risk. Thankfully, there are tools available to help you manage these responsibilities, especially those that combine registered agent services with virtual mailbox solutions.

Virtual Mailbox and Registered Agent Services

Every LLC is required to have a registered agent in its formation state. This agent acts as the official point of contact for receiving legal documents, government notifications, and other critical correspondence. Without one, your LLC could face administrative dissolution in as little as 30 to 60 days.

"A registered agent is your business’s official point of contact for receiving legal documents, government notices, and compliance materials." – Rick Mak, Founder, BusinessAnywhere

It’s important to note that a registered agent’s address and your business mailing address serve different purposes. For example, banks often reject registered agent addresses during account applications because they don’t represent an actual operational location. This is where a virtual mailbox comes in handy. It provides your LLC with a real street address – not a P.O. Box – that satisfies most bank Know Your Customer (KYC) requirements.

BusinessAnywhere offers registered agent services for $147 annually, with the first year free if bundled with a new LLC formation. Their virtual mailbox services start at $20 per month for the Basic plan or $30 per month for the Premium plan (billed annually).

If you own properties in multiple states, a registered agent service covering all 50 states can simplify things by consolidating billing and compliance tracking.

Compliance and Document Management Platforms

In addition to address services, centralized platforms can streamline compliance and document management. Having a compliance dashboard helps ensure you never miss a filing or update. These platforms manage everything from formation documents and virtual mail to compliance reminders and amendment filings, keeping your state records current.

"Operating with outdated state records creates serious risks. You may face penalties and fines… In some cases, your business can be administratively dissolved." – BusinessAnywhere

BusinessAnywhere also provides templates for essential documents like an Operating Agreement ($97) and a Banking Resolution ($27), both commonly required by banks and title companies. Need a document notarized remotely? Their online notary service costs $37 per document and covers items such as USPS Form 1583 and property-related agreements.

With a 4.5/5 Trustpilot rating, BusinessAnywhere is well-regarded for its responsive support and ability to help LLCs stay compliant without the constant stress of missing deadlines.

Conclusion: Key Takeaways for Real Estate Investors

Using an LLC to hold your real estate investments is a smart move for protecting your assets and managing taxes effectively. By creating a clear boundary between your personal finances and property-related risks, an LLC provides tax flexibility and demonstrates to lenders and partners that you’re running a professional operation.

The popularity of LLCs in the real estate world speaks volumes about their effectiveness in safeguarding assets and supporting growth. However, their benefits rely on disciplined management and strict compliance. To maintain these protections, it’s essential to keep your financial records separate, sign all property-related documents in the LLC’s name, and stay on top of your state’s filing requirements. As Angela Davis of Kiavi emphasizes:

"Mixing personal and LLC funds might break down your liability protection, a legal concept known as ‘piercing the corporate veil.’"

To strengthen your protection even further, consider pairing your LLC with solid insurance coverage, such as landlord liability and umbrella policies. This combination not only reduces potential risks but also simplifies tax and operational management.

Looking ahead, the decisions you make now – whether you’re managing a single property or building a larger portfolio – will shape your ability to grow, protect, and eventually pass on your investments. Treat your real estate ventures like a business. With a well-structured LLC, disciplined financial practices, and comprehensive insurance, you’ll set the stage for long-term success in real estate investing.

FAQs

Do I need a separate LLC for each rental property?

When deciding whether to set up a separate LLC for each rental property, it often comes down to the size of your portfolio and how much risk you’re comfortable taking on. If you own just one or two smaller properties, sticking with a single LLC could save you time and money while still providing some level of protection. However, as your portfolio expands, creating separate LLCs for each property can help shield your assets by isolating risks tied to individual properties. For those managing 11 or more properties, a Series LLC might be worth considering. This structure allows you to manage liability under one overarching entity while keeping each property legally distinct.

Will moving a mortgaged property into an LLC trigger the due-on-sale clause?

Yes, transferring a property with a mortgage to an LLC can activate a due-on-sale clause. This happens because transferring the title changes ownership, and such transfers aren’t covered under the protections of the Garn-St. Germain Act. That said, loans backed by Fannie Mae or Freddie Mac typically permit these transfers as long as you maintain control of the LLC and meet specific occupancy guidelines. For other types of loans, whether the clause is enforced often depends on your lender’s discretion and policy.

What’s the easiest way to avoid piercing the LLC veil?

Keeping your personal and business finances separate is the simplest way to protect the legal shield of your LLC. Start by opening a dedicated business bank account for all LLC transactions. Avoid mixing personal and business funds at all costs, and make sure to document any major business decisions or actions thoroughly. It’s also crucial to follow formalities like holding annual meetings and signing contracts in your capacity as an LLC representative, not as an individual. These practices help ensure your LLC retains its legal protections.

Related Blog Posts

- LLC for Rental Property: Do You Actually Need One to Protect Your Personal Assets?

- What Is a Holding Company LLC for Real Estate (and When Should You Form One)?

- The Most Common LLC Mistakes That Let Tenants’ Lawyers Come After Your Personal Assets

- From Side Hustle Landlord to Real Business: When It’s Time to Treat Your Rentals Like a Company