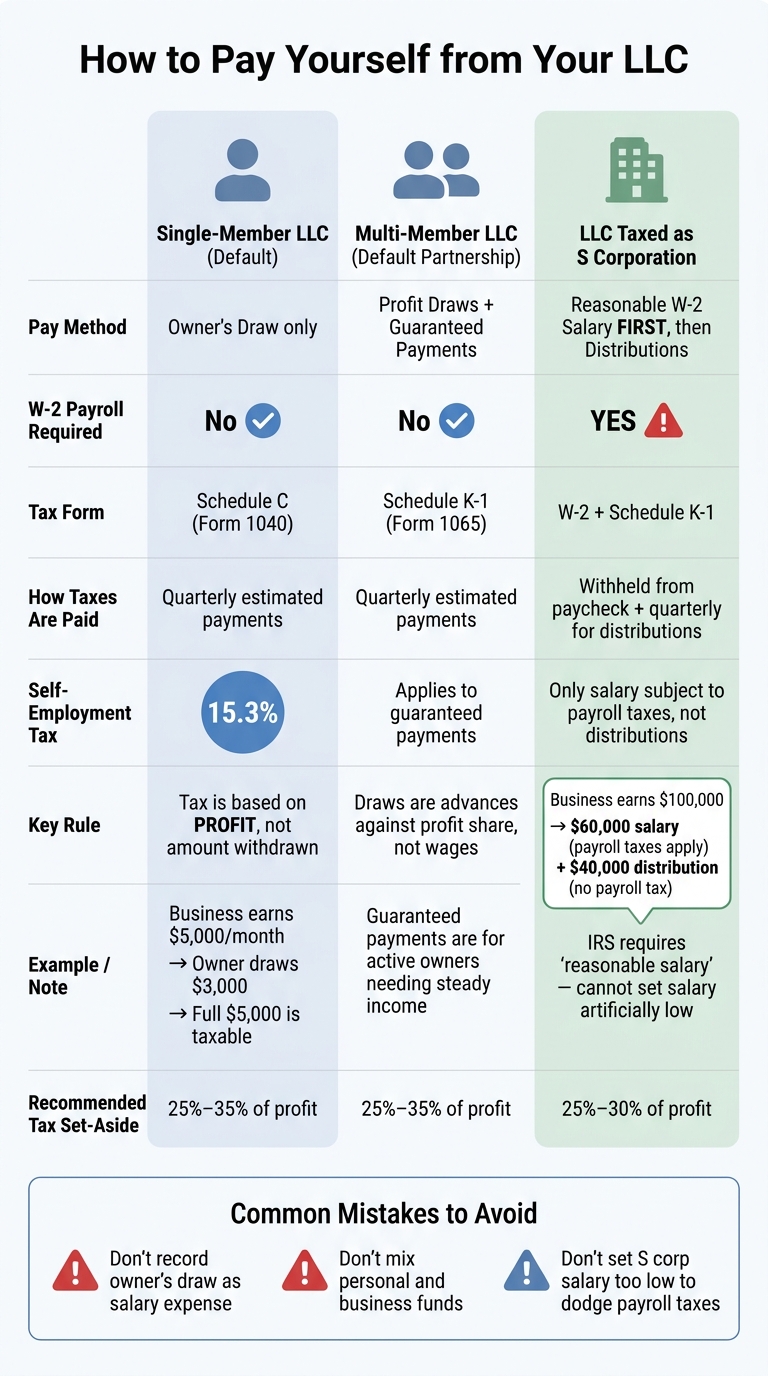

Your LLC does not decide how you pay yourself. Your tax status does. In most cases, a default single-member LLC owner takes an owner’s draw, a multi-member LLC owner takes draws or guaranteed payments, and an LLC taxed as an S corporation must pay an active owner a W-2 salary first, then distributions.

Here’s the short version:

- If I own a single-member LLC, I usually pay myself with draws, not payroll.

- If I own a multi-member LLC, I usually take draws and may receive guaranteed payments.

- If my LLC chose S corp tax treatment, I must run payroll and pay myself a reasonable salary.

- With draws, I pay taxes through quarterly estimated payments.

- With salary, taxes come out of each paycheck through withholding.

- For many owners, the biggest mistake is thinking tax is based on what they withdraw. It usually isn’t. It’s based on profit.

A few numbers make this easier to grasp:

- Self-employment tax is often 15.3%

- Many owners set aside about 25% to 35% of profit for taxes

- An S corp owner might split pay between, for example, $60,000 in salary and $40,000 in distributions if the business earned $100,000

Quick Comparison

| LLC tax setup | How I usually pay myself | W-2 payroll | Main tax form |

|---|---|---|---|

| Single-member LLC | Owner’s draw | No | Schedule C |

| Multi-member LLC | Draws + guaranteed payments | No | Schedule K-1 |

| LLC taxed as S corp | Salary + distributions | Yes | W-2 + Schedule K-1 |

Bottom line: if I match my pay method to my LLC’s tax treatment, keep business and personal money separate, and track each payment the right way, I can avoid tax problems and messy books.

How Your LLC’s Tax Status Controls How You Pay Yourself

Your LLC’s tax status decides how you get paid. That’s the big idea.

In some setups, you take owner’s draws. In others, you need to run W-2 payroll. And in one case, you may use both. The table below gives you the quick version of how to set up an LLC and pay yourself, then the sections after it explain how each setup works.

| LLC Tax Classification | Primary Payment Method | Payroll (W-2) Required? | Tax Form for Owner Income |

|---|---|---|---|

| Single-Member (Default) | Owner’s Draw | No | Schedule C (Form 1040) |

| Multi-Member (Partnership) | Draw + Guaranteed Payments | No | Schedule K-1 (Form 1065) |

| S Corporation Election | Reasonable Salary + Distributions | Yes | W-2 and Schedule K-1 |

Single-Member LLC: Taking Draws Instead of W-2 Wages

By default, the IRS treats a single-member LLC and its owner as one taxpayer. So instead of paying yourself wages, you move money from the business account to your personal account. That transfer is called an owner’s draw.

You do not need payroll or a W-2 in this setup. Your business profit goes on Schedule C, and you owe income tax plus self-employment tax on that profit whether you take the money out or leave it in the business.

That last part trips people up all the time. The tax is based on the profit, not on the amount you draw.

You also should not run payroll for yourself in a default single-member LLC. It adds extra cost and paperwork without the tax upside tied to an S corporation election.

Multi-member LLCs follow a different set of rules because owners are not treated as employees by default.

Multi-Member LLC: Draws, Profit Allocations, and Guaranteed Payments

A multi-member LLC is taxed as a partnership by default. Each member gets a share of the profits, and that share is reported on Schedule K-1 (Form 1065) based on the operating agreement and the ownership split.

Members can take draws during the year, but those draws are not a salary. They’re advances against that member’s share of profits.

If one active member needs steady pay, the operating agreement can allow guaranteed payments. These are set payments for services or capital, even when profits are low. That can be useful when one owner does more day-to-day work and needs a steady amount coming in.

A few points matter here:

- Guaranteed payments are still subject to self-employment tax

- The member getting the payment is not treated as an employee

- Regular draws still count as part of the member’s profit allocation, not wages

If the LLC elects S corporation status, the playbook changes. At that point, owner pay starts with W-2 wages.

LLC Taxed as an S Corporation: Salary First, Distributions Second

When an LLC elects S corporation tax treatment, active owners must be treated as employees. That means they need to be paid a reasonable salary through W-2 payroll before taking profit distributions.

This is where the tax angle changes. Owner pay is split into two buckets: salary and distributions.

Only the salary portion is subject to payroll taxes. Distributions taken above that salary are not. That’s where the tax savings can come from.

Owner’s Draw vs. Salary: Taxes, Payroll, and Recordkeeping Compared

Once your tax status is set, the next step is simple: how do you actually pay yourself? In practice, it usually comes down to an owner’s draw, a payroll salary, or a mix of both, depending on how the LLC is taxed.

Here’s how the two payment methods stack up when it comes to taxes, payroll, and bookkeeping:

| Factor | Owner’s Draw | Salary (W-2) |

|---|---|---|

| Typical LLC type | Default-taxed LLCs | LLCs taxed as S corps |

| Payroll required? | No | Yes |

| How taxes are paid | Quarterly estimated tax payments | Withheld from each paycheck and remitted by the business |

| Withholding applies? | No | Yes – income tax, Social Security, Medicare |

| Timing flexibility | High – take money as cash allows | Low – fixed amounts on a set schedule |

| Bookkeeping entry | Debit Owner’s Equity; credit Cash. | Debit Wage Expense; credit Cash and payroll liabilities. |

| Tax deductible for the business? | No | Yes |

How Owner’s Draws Work in Practice

An owner’s draw is just a transfer of money from the business to you personally. No taxes come out at the time of the transfer. That means you have to pay those taxes yourself through quarterly estimated tax payments.

In your books, each draw should be recorded as a debit to your Owner’s Equity or Capital account and a credit to your Business Checking account. It should not be recorded as salary expense. That’s a common mistake, and it can muddy your books fast.

A good rule of thumb is to set aside 25% to 35% of your profits for federal and state taxes, so quarterly payments don’t hit like a brick.

This setup is common for default-taxed LLCs. If your LLC is taxed as an S corporation, owner pay works differently because compensation goes through payroll.

How Salary Works in Practice

A salary is paid through W-2 payroll. Each paycheck has federal income tax, Social Security, and Medicare taxes withheld. On top of that, the business also pays its share of FICA.

From an accounting standpoint, salary is recorded as a deductible wage expense, which lowers the business’s net profit. You also need to handle the payroll forms that come with it, including issuing yourself a Form W-2 at year-end and filing Form 941 for payroll taxes.

There’s less wiggle room here too. Salary payments follow a fixed schedule, not an as-needed cash transfer.

Payment Scenarios by LLC Type

These examples show what the rules look like when money starts moving.

Single-member LLC: The business earns $5,000 in monthly profit. The owner transfers $3,000 to their personal account as a draw. Even so, the full $5,000 is taxable, not just the amount withdrawn. The owner also owes self-employment tax at 15.3% on that profit.

Two-member LLC: Two members split profits based on their LLC operating agreement. Neither takes a W-2 salary. Each gets a Schedule K-1 showing their share of profits, and both owe self-employment tax on that allocated income, no matter how much they actually pulled out during the year.

LLC taxed as an S corporation: The business earns $100,000 in net profit. The owner pays themselves a $60,000 reasonable salary through payroll, and payroll taxes apply to that amount. The other $40,000 is taken as a distribution, which is not subject to self-employment tax. So in this setup, only the $60,000 salary gets hit with payroll tax.

sbb-itb-ba0a4be

How to Pick the Right Pay Method and Avoid Common Mistakes

Which Pay Method Fits Each LLC Setup

Now that the pay options are clear, the next step is to match them to your LLC’s tax setup.

| LLC Type | Pay Method | Key Requirement |

|---|---|---|

| Single-member LLC (default) | Owner’s draw only | Members are taxed as partners |

| Multi-member LLC (default) | Profit distributions and guaranteed payments for services | Members are taxed as partners |

| LLC taxed as an S corporation | Reasonable salary first, then distributions | Formal payroll required |

Owner’s draws give you more flexibility. Salary is a different animal. It needs steady cash flow, a payroll system, and yearly filings. If your LLC is taxed as an S corporation, that setup can make sense when the S corp vs LLC tax benefits outweigh the payroll and filing costs.

Once you choose a method, the hard part isn’t picking it. It’s using it the right way so you don’t run into IRS trouble or messy books.

Common Mistakes That Cause IRS and Bookkeeping Problems

One of the biggest mistakes S corp owners make is setting their salary too low to cut payroll taxes. That can backfire fast. An S corp owner must pay themselves a reasonable salary. The IRS looks at your duties, experience, time spent in the business, and what similar businesses pay for similar work. If your salary is too low, the IRS can treat distributions as wages and hit you with back taxes and penalties.

A good rule of thumb is to set aside 25% to 30% of profit for quarterly estimated taxes.

Another mistake is treating draws like free cash. Don’t base draws on profit alone. Base them on profit and the cash you need to keep in reserve. That buffer matters.

Here’s where people get into trouble:

- Recording an owner’s draw as a salary expense

- Paying personal bills straight from the business account

- Taking out too much cash before setting aside money for taxes

These aren’t small bookkeeping slipups. A draw is an equity transaction, not a deductible business expense. And once personal and business money start mixing, things can get messy in a hurry. That can pierce the corporate veil. On top of that, pulling too much cash before covering taxes and operating costs is the kind of bad management courts may look at when deciding whether to hold owners personally liable.

How to Set Up a Simple Owner Pay System for Your LLC

Banking, Bookkeeping, and Payroll Basics

Once you know whether you’ll use draws, payroll, or a mix of both, the next step is simple: build a system that keeps each payment clean and easy to track.

Start with a business bank account for your LLC. Keep business and personal money separate, and use a clear transfer process so every owner payment leaves a paper trail. Then set up bookkeeping that tracks income, expenses, and your equity balance in real time. That gives you a clear view of how much you can draw.

If your LLC is taxed as an S corporation, add payroll software. It helps you handle withholdings, Form 941 filings, and W-2s the same way each pay period.

For default-taxed LLCs, set aside 25% to 35% of profits in a separate savings account for federal and state taxes.

Records, Forms, and Support That Make Owner Payments Easier

Good records make owner pay easier to manage and easier to back up if anyone asks questions. Your paperwork should match your LLC’s tax treatment.

If you want audit-ready records, stay organized all year. Most LLC owners should keep these documents close at hand:

- Operating agreement – shows how members are paid and how profits are divided

- Draw history and capital account balances – shows equity over time

- Payroll reports and W-2s – needed for S corp owners

- Quarterly estimated tax payment confirmations – proof that payments were made on time

- Tax filings – Schedule C, Form 1065, or Form 1120-S based on your LLC’s tax status

| Payment Type | Key Tax Forms | Recordkeeping Focus |

|---|---|---|

| Owner’s Draw | Schedule C or Schedule K-1, Schedule SE | Draw history, capital accounts, equity balance |

| S Corp Salary | W-2, Form 941, Form 1120-S | Payroll reports, withholding records |

| Guaranteed Payments | Form 1065, Schedule K-1 | Partnership agreement terms, service records |

Conclusion: Match Your Pay Method to Your Tax Status

Your LLC’s tax status shapes how you pay yourself. Default-taxed LLCs usually use draws. Active multi-member partners may use guaranteed payments. S corporations use a reasonable W-2 salary plus distributions.

Clean banking, steady bookkeeping, and proper payroll records help keep that setup compliant throughout the year.

FAQs

Can I switch from draws to salary later?

Yes. You can switch from owner’s draws to a salary later, but it often takes more than a simple bookkeeping change.

You may need to make a formal tax election, file the right IRS forms, and set up payroll. That also means dealing with tax withholding and making sure your business structure lines up with IRS rules.

It’s worth looking at your options closely. A move like this can change how you’re taxed and what compliance steps you need to handle.

How do I know if my S corp salary is reasonable?

Your S corp salary is usually reasonable if it lines up with what similar businesses pay for similar work.

The IRS says to look at a few things, including industry pay, your job duties, your education, your experience, and your local cost of living.

What if my LLC has profit but not enough cash to pay me?

If your LLC is profitable but doesn’t have enough cash to pay you right now, you can take an owner’s draw based on the cash that’s actually available instead of forcing an immediate payment.

The big thing is balance: leave enough money in the business to cover bills, day-to-day costs, and upcoming needs.