As an S Corp owner, you can pay yourself in two ways: salary (W-2 wages) and distributions (profit withdrawals). Each has different tax implications:

- Salary: Subject to a 15.3% payroll tax (Social Security and Medicare). The IRS mandates taking a "reasonable salary" based on industry standards before distributions.

- Distributions: Not subject to payroll taxes, offering potential savings. However, they require compliance with IRS rules, including matching ownership percentages if there are multiple shareholders.

The 2025 One Big Beautiful Bill Act made distributions eligible for the 20% Qualified Business Income (QBI) deduction, increasing their tax efficiency. Balancing salary and distributions can save thousands annually while ensuring compliance. Missteps, like underpaying salary, risk audits, back taxes, and penalties. Accurate recordkeeping and regular reviews are essential to avoid issues.

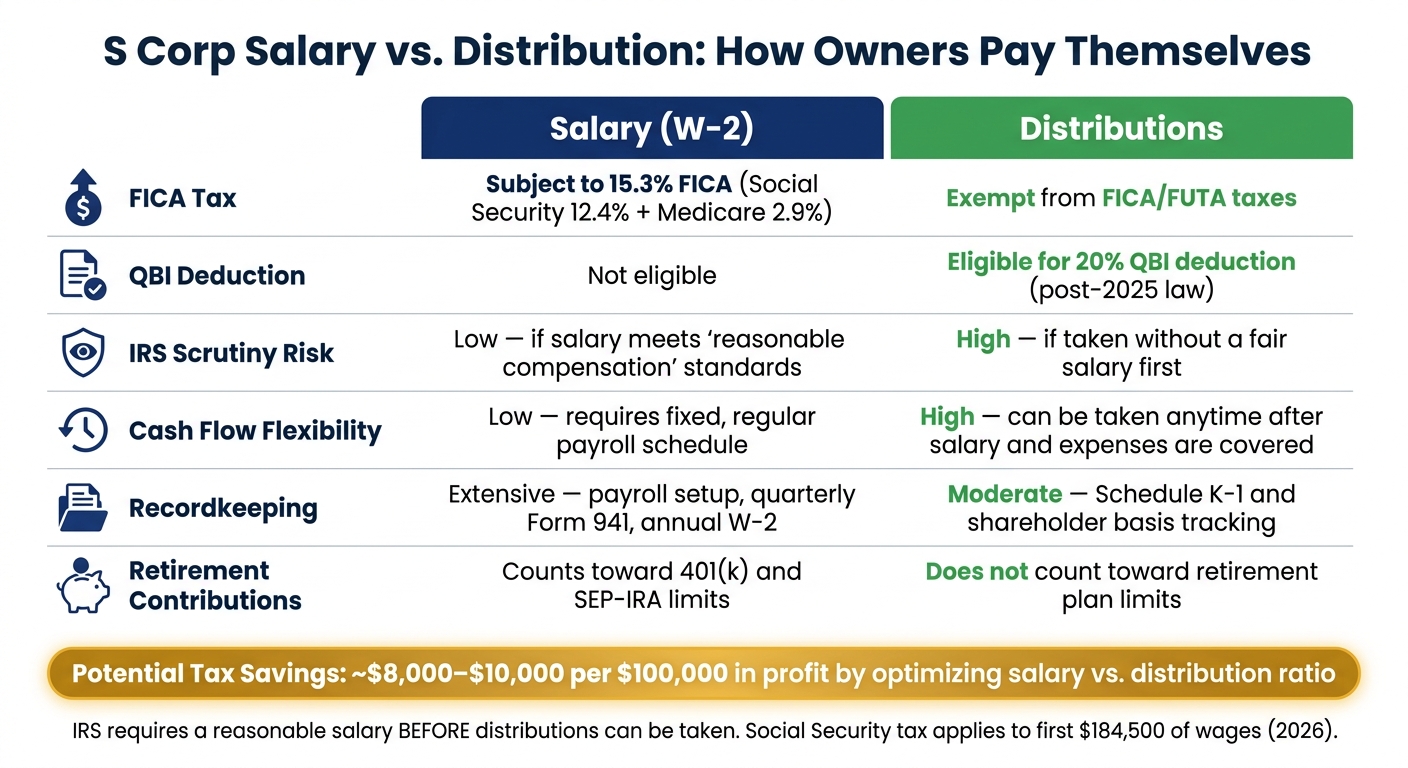

Quick Comparison

| Feature | Salary (W-2) | Distributions |

|---|---|---|

| Tax Treatment | Subject to 15.3% FICA tax | Exempt from FICA tax |

| QBI Deduction | Not eligible | Eligible (post-2025 law) |

| IRS Scrutiny Risk | Low if salary is reasonable | High if no salary is paid first |

| Recordkeeping | Requires payroll setup and filings | Requires basis tracking |

| Retirement Contributions | Counts toward 401(k)/SEP-IRA limits | Does not count |

To stay compliant and maximize your income, prioritize a reasonable salary, follow payroll procedures, and use distributions strategically.

1. Salary in an S Corp

If you’re an active owner of an S Corp, you’re required to take a W-2 salary before drawing distributions. The IRS makes this clear in its Form 1120-S instructions:

"Distributions and other payments by an S corporation to a corporate officer must be treated as wages to the extent the amounts are reasonable compensation for services rendered to the corporation."

This salary is subject to federal income tax and the full 15.3% FICA tax (split between Social Security at 12.4% and Medicare at 2.9%). The FICA tax is divided equally between you and the business. For 2026, Social Security tax applies only to the first $184,500 of wages – any income above that amount is exempt from the Social Security portion. To stay compliant, it’s essential to understand what the IRS considers "reasonable compensation."

What Counts as "Reasonable"?

The IRS uses a "facts and circumstances" approach to determine reasonable compensation. Factors like industry norms, your job responsibilities, and the time you dedicate to the business all play a role. A good way to establish a fair salary is by consulting wage data from the Bureau of Labor Statistics (BLS) or reviewing industry-specific salary surveys. These tools can help you set a defensible salary and avoid compliance issues. A critical example is the case of David E. Watson, P.C. v. United States, which highlights the consequences of underpaying yourself.

Payroll Procedures Matter

Once you’ve determined a reasonable salary, it’s important to follow proper payroll practices. This means processing your salary through a formal payroll system, which includes withholding taxes, filing Forms 941 and 940, and issuing a W-2. Irregular payments, like lump sums or informal bank transfers, can raise red flags with the IRS.

Additionally, if your S Corp covers your health insurance premiums and you own more than 2% of the company, those premiums must be reported as wages in Box 1 of your W-2. However, these amounts are not subject to FICA taxes.

sbb-itb-ba0a4be

2. Distribution in an S Corp

Once you’ve met the IRS requirement of paying yourself a reasonable salary, distributions offer a way to access remaining profits with a tax advantage. Unlike your W-2 wages, distributions aren’t subject to the 15.3% FICA tax, making them a more efficient way to take income from your business. This tax savings is why many S Corp owners rely on distributions as a supplement to their salaries.

Distributions are reported on Schedule K-1 (attached to Form 1120-S) and flow through to your personal Form 1040 as pass-through income. It’s important to note that you’re taxed on your share of the S Corp’s total profits, not just the cash you withdraw. So even if you leave money in the business, you’ll still owe income tax on that amount. To avoid surprises at tax time, many S Corp owners make quarterly estimated tax payments.

Your Basis Matters

The amount you can receive tax-free depends on your stock basis – essentially your total economic investment in the company, adjusted for profits, losses, and any prior distributions. If a distribution exceeds your basis, the excess is treated as a long-term capital gain and taxed accordingly. Keeping detailed and accurate records of your stock basis is essential to avoid unexpected tax liabilities.

The QBI Deduction Advantage

Distributions also play a role in maximizing your tax strategy by qualifying for the 20% Qualified Business Income (QBI) deduction, provided your income meets certain thresholds. For single filers, the full deduction applies if your taxable income is below $197,300, and for married couples filing jointly, the limit is $394,600.

One Rule You Can’t Ignore

If your S Corp has multiple shareholders, distributions must strictly match ownership percentages. For example, a 40% shareholder must receive 40% of the total distributions. Unequal payouts can draw IRS attention and even risk your S Corp status. To stay compliant, always document distributions in your corporate minutes and ensure they are accurately recorded in your accounting software.

Pros and Cons

Now that we’ve covered the mechanics and responsibilities of both methods, let’s dive into their strengths and weaknesses.

| Feature | S Corp Salary (W-2) | S Corp Distributions |

|---|---|---|

| Tax Treatment | Subject to 15.3% FICA (Social Security + Medicare) plus FUTA | Exempt from FICA/FUTA; qualifies for the 20% QBI deduction |

| IRS Scrutiny Risk | Low, if salary meets "reasonable compensation" standards | High, if taken without a fair salary in place – only distributions beyond a reasonable salary avoid scrutiny |

| Cash Flow Flexibility | Low; requires a fixed, regular payroll schedule | High; can be taken anytime after salary and expenses are covered |

| Recordkeeping | Extensive; payroll setup, quarterly Form 941, annual W-2s | Moderate; Schedule K-1 reporting and shareholder basis tracking |

| Retirement Contributions | Counts toward 401(k) and SEP-IRA limits | Does not count toward retirement plan contribution limits |

Key Takeaways

One of the biggest perks of taking distributions is the tax savings. By shifting part of your income from salary to distributions, you can save roughly $8,000 to $10,000 annually on every $100,000 in profit. However, these savings only kick in after you’ve set a defensible salary.

On the other hand, the payroll requirements for salaries can be a hassle. You’ll need to set up an EIN, withhold taxes, file Form 941 quarterly, and issue a W-2 at the end of the year. These steps add administrative costs and complexity.

Attorney Amanda Hayes emphasizes the heightened IRS focus on salary versus distributions for S corp employees: "The IRS has stepped up its scrutiny of salary versus distributions with S corp employees". Missteps in this area can lead to serious consequences. If distributions are reclassified as salary, you could face back taxes, interest, and a 20% accuracy-related penalty. For those who’ve underpaid salary over several years, the liabilities can easily climb past $20,000.

Conclusion

S Corp owners need to prioritize taking a reasonable salary before drawing distributions. Failing to do so – or underreporting your salary – can attract IRS attention and lead to back taxes, interest, and a 20% accuracy-related penalty.

To determine your salary, rely on market data from trusted sources like BLS.gov and keep detailed records explaining how you arrived at the figure. This documentation is crucial for justifying your compensation.

Once a fair salary is established, distributions offer a way to save approximately 15.3% in payroll taxes per dollar. Plus, the post-July 2025 One Big Beautiful Bill Act ensures the 20% QBI deduction remains a permanent benefit.

"The right balance of salary and distributions can reduce your tax burden, increase your retirement contributions, and free up cash for growth." – Business Advisory and Accounting Partners

Make it a habit to review your salary-to-distribution ratio each year and monitor your stock basis to avoid taxable excess distributions. Striking this balance is key to an effective S Corp tax strategy.

FAQs

How do I figure out a “reasonable salary” for my S Corp?

To figure out what counts as a “reasonable salary” for your S Corp, start by looking at what others with similar skills, experience, and responsibilities earn in your industry. Pay attention to factors like industry norms, your specific role, and your geographic location. Make sure to document your research by referencing comparable salaries from businesses that are similar to yours. This ensures your salary aligns with fair market value, keeping you in line with IRS guidelines and helping you avoid penalties or having distributions reclassified as wages.

How do I decide the right split between salary and distributions?

To figure out the best way to split your income as an S Corp owner, it’s crucial to set a reasonable salary that meets IRS standards. This means your salary should reflect what someone in a similar position, within the same industry and location, would typically earn.

A common approach is to allocate 30%-60% of the net profit to your salary, with the remainder taken as distributions. However, this isn’t a one-size-fits-all rule. You’ll need to consider factors like industry benchmarks, the specific responsibilities of your role, and available wage data. Striking the right balance ensures you stay compliant, make the most of tax advantages, and steer clear of potential IRS penalties.

What happens if my distributions exceed my stock basis?

If the distributions you receive go beyond your stock basis, the excess is usually taxed as a capital gain. This also lowers your basis in the S corporation stock. It’s important to keep track of your stock basis to steer clear of any unexpected tax consequences.