If you’re a business owner, you might be paying too much in self-employment taxes. By electing S Corporation (S Corp) status, you can legally reduce the 15.3% self-employment tax burden on your business profits. Here’s how it works:

- Lower Taxable Income: S Corps split income into two parts: a W-2 salary (taxed at 15.3% for Social Security and Medicare) and shareholder distributions (not subject to self-employment tax).

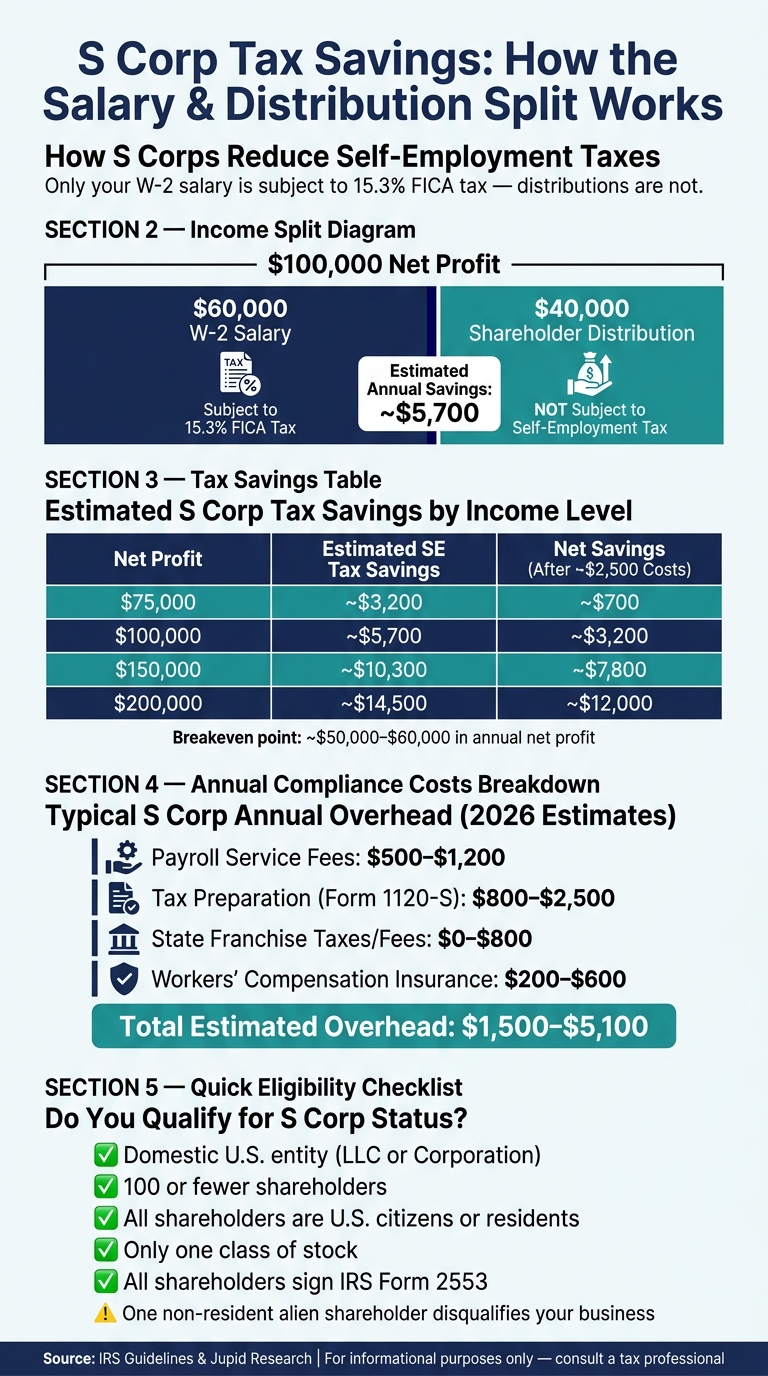

- Potential Savings: For example, if your business earns $100,000 in profit and you set your salary at $60,000, you could save around $5,700 in taxes annually.

- Eligibility: Your business must meet IRS rules, such as being a domestic entity, having 100 or fewer shareholders, and filing Form 2553 on time.

- Compliance Costs: Expect annual expenses like payroll services, tax filings, and state fees, typically ranging from $1,500 to $5,100.

This strategy is most effective for businesses with net profits over $60,000. However, you must pay yourself a reasonable salary and follow IRS guidelines to avoid penalties.

What Is an S Corporation and How Does It Work?

An S Corporation isn’t a unique business entity – it’s actually a federal tax election made with the IRS under Subchapter S of the Internal Revenue Code. Choosing this status doesn’t change how your business is classified at the state level; it only alters how the IRS taxes your business. This structure can be a game-changer for reducing self-employment taxes, so understanding how it works is key.

"An S-Corporation isn’t a business entity type – it’s a tax election that LLCs and corporations can make with the IRS." – SDO CPA

S Corps as Pass-Through Entities

When a business elects S Corp status, its income flows directly to the shareholders’ personal tax returns, avoiding federal income tax at the corporate level. Compare this to a C Corporation, where profits are taxed twice – first at the corporate level and again when distributed as dividends.

One of the biggest perks of an S Corp is how it handles self-employment taxes. Unlike a sole proprietorship or a default LLC, which subject all net profits to self-employment tax, an S Corp allows you to split your income. You pay yourself a W-2 salary, which is subject to FICA taxes, while the remaining profit taken as a shareholder distribution isn’t subject to the 15.3% self-employment tax.

Here’s a quick comparison of S Corps and other common business structures:

| Feature | S Corp | Sole Prop / Default LLC | C Corp |

|---|---|---|---|

| Taxation | Pass-through | Pass-through | Double taxation |

| Self-Employment Tax | Only on W-2 salary | On 100% of net profit | Only on salary |

| Max Shareholders | 100 (U.S. residents only) | Unlimited | Unlimited |

| Stock Classes | One class only | N/A | Multiple classes allowed |

| Payroll Required | Yes, for owner-employees | No | Yes, for owner-employees |

These features make S Corps an attractive choice for many businesses. However, to take advantage of these benefits, you’ll need to meet specific IRS requirements for S Corp status.

IRS Eligibility Requirements for S Corp Status

Not every business can qualify for S Corp status. The IRS has strict rules, including:

- The business must be a domestic U.S. entity, either a corporation or an LLC electing corporate treatment.

- It can have no more than 100 shareholders, though family members can count as a single shareholder.

- All shareholders must be U.S. citizens or permanent residents. A single non-resident alien shareholder disqualifies the business.

- Shareholders must be individuals, certain trusts, or estates. Partnerships and corporations cannot hold shares in an S Corp.

- The company can issue only one class of stock. While voting rights can vary, all shareholders must have identical economic rights.

- Every shareholder must unanimously agree to the S Corp election by signing IRS Form 2553.

A practical tip: Make sure to get an Employer Identification Number (EIN) before filing Form 2553. The IRS won’t process your election without it.

How S Corps Lower Self-Employment Taxes

An S Corp gives business owners a way to reduce self-employment taxes by splitting income into two parts: a W-2 salary (subject to FICA taxes) and shareholder distributions (which avoid the 15.3% self-employment tax).

The Salary and Distribution Split

As an S Corp owner-employee, you pay yourself a W-2 salary. This salary is subject to FICA taxes – 12.4% for Social Security and 2.9% for Medicare. Any remaining profit is distributed to you as a shareholder. While distributions are still taxed as ordinary income, they are not subject to FICA or self-employment taxes.

"The concept behind the S Corp tax advantage is simple: only your W-2 salary is subject to FICA taxes. Every dollar of profit above that salary passes through as a distribution – completely free from the 15.3% self-employment tax." – Slava Akulov, Founder, Jupid

Let’s break it down with an example: If your business earns $100,000 in net profit and you set your salary at $60,000, you could save around $5,700 in self-employment taxes. If your net profit increases to $200,000, the annual tax savings could climb to about $14,500. After deducting typical S Corp compliance costs of approximately $2,500 per year, the savings can still be substantial, especially at higher income levels.

| Net Profit | Estimated SE Tax Savings | Net Savings (After ~$2,500 in Costs) |

|---|---|---|

| $75,000 | ~$3,200 | ~$700 |

| $100,000 | ~$5,700 | ~$3,200 |

| $150,000 | ~$10,300 | ~$7,800 |

| $200,000 | ~$14,500 | ~$12,000 |

Next, it’s important to understand the IRS rules regarding reasonable compensation to ensure your salary complies with federal guidelines.

The IRS Reasonable Salary Requirement

The IRS requires S Corp owner-employees to pay themselves a "reasonable salary" before taking distributions. This prevents individuals from avoiding taxes by setting artificially low salaries. While there’s no strict formula, the IRS evaluates factors like industry standards, your role and responsibilities, time spent on the business, and what someone in a similar position might earn. A common practice is to use a 60/40 split between salary and distributions, but this may need adjustment based on your specific situation.

Failing to meet the reasonable salary requirement can trigger IRS scrutiny. In fact, about 73% of S Corp audits focus on this issue, with an average of $31,000 in additional taxes assessed for misclassification. One notable case involved David E. Watson, P.C. v. United States (2012), where an owner paid himself just $24,000 in salary on over $200,000 in business earnings. The IRS reclassified much of his distributions as wages, resulting in back payroll taxes, penalties, and interest.

To avoid issues, benchmark your salary using resources like the Bureau of Labor Statistics, Glassdoor, or PayScale. Keep detailed records of how you determined your salary in case of an audit.

How to Set Up an S Corp for Tax Savings

Once you’ve determined the right balance between salary and distributions, the next step is to formalize your S Corp election with the IRS. While the process itself is straightforward, it’s important to pay attention to deadlines, state-specific rules, and paperwork requirements.

Filing Form 2553 with the IRS

To elect S Corp status, you need to file Form 2553 (Election by a Small Business Corporation) with the IRS. Before filing, make sure your business qualifies. The key requirements include:

- Being a domestic entity

- Having no more than 100 shareholders

- Issuing only one class of stock

- Ensuring all shareholders are U.S. residents or citizens (no nonresident alien shareholders)

If your business operates on a calendar year, you must file by March 15 to elect S Corp status for the current tax year. For newly formed businesses, the deadline is within 75 days of formation. If you miss the deadline, the IRS offers late election relief under Rev. Proc. 2013-30.

Submit Form 2553 via mail or fax to the appropriate IRS Service Center. If you choose to fax, keep the transmission confirmation. For mailing, use certified mail with a return receipt to ensure delivery. The IRS usually processes the form within 60 days and sends a CP261 acceptance notice upon approval. If you don’t hear back within 60 days, you can contact the IRS Business line at 1-800-829-4933.

For LLCs electing S Corp status, complete Part IV of Form 2553, which allows the IRS to treat the LLC as a corporation for tax purposes. Avoid filing Form 8832 along with Form 2553, as it may delay processing.

Finally, don’t forget to review state tax policies and filing rules to ensure full compliance at the state level.

State-Level Tax and Filing Considerations

After filing with the IRS, you’ll also need to address state-level requirements. Some states require additional forms to recognize your S Corp status. For instance:

- New York: File Form CT-6

- New Jersey: File Form CBT-2553

- Ohio: Follow specific state procedures

Even in states that automatically follow the federal election, there may still be associated costs. For example:

- California charges a 1.5% net income tax plus an $800 minimum franchise tax annually, regardless of profit.

- Texas doesn’t have a state income tax but still requires franchise tax filings.

Annual state compliance costs for S Corps typically range from $0 to about $800. To avoid surprises, visit your state’s Department of Revenue website for detailed requirements.

Using BusinessAnywhere to Simplify the Process

If managing IRS forms and state filings feels daunting, BusinessAnywhere offers a streamlined solution. Their S-Corp Tax Election service handles Form 2553 for you at a cost of $97. This service includes preparation, submission, and follow-up, so you won’t need to deal with fax machines or certified mail.

If you don’t yet have an Employer Identification Number (EIN) – which is required before filing Form 2553 – BusinessAnywhere can assist with that too. Their EIN Application Service is also $97. Both services are accessible through an online dashboard, allowing you to complete the process entirely remotely. This approach helps ensure your S Corp election is accurate and hassle-free.

sbb-itb-ba0a4be

Is an S Corp the Right Choice for Your Business?

An S Corp isn’t the perfect fit for every business owner. While the tax savings can be appealing, they come with added responsibilities and costs. The key question is whether your tax savings will outweigh the extra administrative expenses.

Tax Savings vs. Added Costs: A Direct Comparison

Operating as an S Corp introduces costs that an LLC doesn’t typically face. These include handling payroll, filing a corporate tax return (Form 1120-S), and staying on top of state-level compliance requirements. Here’s a breakdown of the estimated annual expenses for 2026:

| Expense | Estimated Annual Cost |

|---|---|

| Payroll service fees | $500 – $1,200 |

| Tax preparation (Form 1120-S) | $800 – $2,500 |

| State franchise taxes/fees | $0 – $800 |

| Workers’ compensation insurance | $200 – $600 |

| Total estimated overhead | $1,500 – $5,100 |

Now, let’s compare these costs with potential tax savings. For various net profit levels, the net tax savings (after accounting for approximately $3,000 in compliance costs) are as follows:

| Net Profit | Estimated SE Tax Savings | Net Savings (After ~$3,000 in Costs) |

|---|---|---|

| $75,000 | ~$4,590 | ~$2,090 |

| $100,000 | ~$4,950 | ~$2,450 |

| $150,000 | ~$9,719 | ~$6,719 |

| $200,000 | ~$16,524 | ~$13,524 |

If your net profit is around $50,000, the compliance costs may outweigh the tax benefits. Experts generally agree that the breakeven point for making S Corp status worthwhile falls between $50,000 and $60,000 in annual net profit.

When an S Corp Makes Financial Sense

Once your business generates consistent profits, it’s time to evaluate whether S Corp status is worth the added complexity. Typically, an S Corp becomes a smart choice when your annual net profit consistently exceeds $60,000. A tax professional explains:

"If you expect net income above $80,000 for at least two consecutive years, S-Corp election typically makes sense. One-time spikes may not justify the additional complexity." – SDO CPA

For example, a marketing consultant earning $350,000 in net income saved $37,000 annually in taxes by switching to S Corp status. However, if your net profit regularly falls below $60,000, the compliance costs could outweigh the tax advantages.

That said, S Corps aren’t suitable for every scenario. If you’re planning to raise venture capital, most investors will expect your business to be structured as a C Corp or S Corp. Additionally, if your market-rate salary is close to your total profit, the "reasonable compensation" requirement can leave little room for tax-free distributions, minimizing the tax savings.

Ultimately, S Corp status makes sense only when consistent, higher income justifies the added setup and compliance costs.

Staying Compliant as an S Corp

Choosing S Corp status isn’t a one-and-done decision – it comes with responsibilities you need to handle every year to keep those tax benefits rolling. Staying on top of compliance is just as important as setting up your S Corp in the first place. If you miss deadlines or skip required steps, you could face audits, penalties, or even lose your S Corp status altogether.

Payroll Processing and Tax Filing Requirements

If you’re an S Corp owner, running payroll isn’t optional. You’re required to pay yourself a reasonable W-2 salary on a regular schedule – monthly or quarterly at a minimum. This salary must have federal income tax and FICA taxes (15.3% for Social Security and Medicare) withheld. Consistency is key here; processing payroll only at year-end is a big no-no.

Tax filing is another critical piece of the puzzle. You’ll need to file Form 941 quarterly and submit Form 1120-S by March 15 every year – this is one month earlier than the personal tax filing deadline. Shareholders also receive a Schedule K-1, which outlines their share of the company’s income, deductions, and credits. Missing the Form 1120-S deadline can be costly, with penalties of $210 per month, per shareholder. If your S Corp has multiple owners, those fines can rack up quickly.

Here’s a quick look at the key deadlines and penalties:

| Deadline | Requirement | Penalty for Non-Compliance |

|---|---|---|

| January 31 | Issue W-2s and 1099s | $290 per form |

| March 15 | File Form 1120-S and issue Schedule K-1s | $210/month per shareholder |

| Quarterly | Payroll tax deposits and Form 941 | 10% penalty + interest |

| December 31 | Complete 401(k) employee deferrals | Loss of deduction for that tax year |

To avoid trouble with the IRS, document how you determine your salary using data from reliable sources like the Bureau of Labor Statistics or industry surveys. This creates a solid paper trail in case your compensation ever comes under scrutiny.

But payroll isn’t the only thing to worry about – staying compliant also means adhering to corporate formalities.

Keeping Up with Corporate Formalities

Proper payroll management is just one piece of the puzzle. To maintain your S Corp tax benefits, you need to follow corporate formalities that demonstrate your company operates as a legitimate corporation in the eyes of the IRS. This includes holding annual shareholder meetings, recording meeting minutes, and passing corporate resolutions for significant business decisions – even if you’re the sole shareholder.

Another critical rule: don’t mix personal and business funds. Keep a separate business checking account and make sure all business transactions go through it. Commingling funds can jeopardize your liability protection and raise red flags with auditors.

Additionally, track your shareholder basis each year to avoid unexpected taxable capital gains on distributions that exceed your basis. Regularly check that you’re meeting IRS eligibility requirements, such as:

- Having no more than 100 shareholders

- Issuing only one class of stock

- Ensuring all shareholders are U.S. citizens or residents

Failing to meet these criteria can lead to the termination of your S Corp status. For example, if a shareholder transfers stock to someone who isn’t eligible, your S Corp status could be revoked. And here’s the kicker: you’d typically have to wait five years before you can reapply. Staying vigilant about these rules is essential to keeping your S Corp intact and your tax strategy on track.

Conclusion: Reducing Self-Employment Taxes with an S Corp

The S Corp approach helps reduce self-employment taxes by applying FICA taxes only to your W-2 salary, not to all distributions. This can lead to considerable tax savings, as shown in earlier examples.

To make the most of this strategy, focus on three key steps: ensure you meet IRS eligibility requirements and file Form 2553 on time, pay yourself a reasonable and well-documented salary (not just a nominal amount), and stay on top of payroll filings, Form 1120-S, and other corporate formalities. Cases like Watson v. Commissioner and Radtke v. United States highlight the importance of compliance – if the IRS reclassifies your distributions as wages, the average audit assessment could cost you about $31,000.

This strategy only makes sense when your business consistently generates profits above the breakeven point.

Once you’ve got the basics covered, services like BusinessAnywhere can handle the rest. From filing Form 2553 (for $97) to managing tax filings and annual compliance, everything can be done through a streamlined online dashboard.

The bottom line? Pay yourself a fair salary, stick to deadlines, and keep detailed records to lock in those tax savings. Precision and compliance are your best tools for success.

FAQs

What counts as a reasonable S Corp salary?

A reasonable S Corp salary usually falls between 40% and 70% of net profit, though this can vary based on several factors. These include industry standards, the owner’s responsibilities, level of experience, hours worked, and local wage rates. The IRS mandates that salaries must represent fair market value for the work performed. To comply, business owners should back up their salary decisions with documentation, such as salary surveys or data on comparable wages within the industry.

Do S Corp distributions avoid income tax too?

S-Corp distributions typically aren’t taxed as income, provided they don’t exceed the shareholder’s basis. These distributions are treated as a return of the shareholder’s investment rather than taxable income. However, the income generated by the S-Corp is taxed when it’s earned and reported on the shareholder’s Schedule K-1, not when the distributions are actually paid out. This setup allows S-Corps to avoid double taxation while ensuring the income is taxed properly.

When do S Corp savings outweigh the extra costs?

When your business’s net profit reaches $50,000 to $60,000 or more annually, the tax savings from an S Corp often outweigh the added expenses. This is because you can balance a reasonable salary with distributions, reducing overall tax liability. For businesses earning between $75,000 and $100,000 in net profit, the potential savings can become even more pronounced. However, if your net profit is below $50,000, the extra costs of payroll and filing might surpass any tax benefits, making S Corp status less appealing in such cases.