Yes, you can build business credit from zero. In most cases, it starts with 4 steps: form an LLC or corporation, get an EIN, open a business bank account, and add reporting trade lines with bureaus like Dun & Bradstreet, Experian Business, and Equifax Business.

If I were starting from scratch, I’d keep it simple:

- Set up a legal business entity separate from my personal identity

- Make sure my business name, address, and phone number match everywhere

- Get a D-U-N-S Number

- Open 3 to 5 vendor accounts that report

- Pay invoices 10 to 20 days early

- Keep card use under 30% – and under 10% if I can

- Check reports every quarter for errors

A few numbers matter right away:

- PAYDEX 80 = pays on time

- Experian Intelliscore 76+ = often seen as lower risk

- Many lenders want 3 to 6 months of bank history

- A late payment can take 6 to 12 months to recover from

Business credit does not build by itself. Accounts must report. And if I use the wrong setup, mixed business details, or non-reporting vendors, I can waste months with nothing to show for it.

That’s the whole path in plain English: set up the business right, open reporting accounts, pay early, keep balances low, and monitor the files.

Set Up Your Business So Credit Bureaus and Lenders Can Find It

Before you apply for even one vendor account or business credit card, credit bureaus and lenders need a clear way to verify that your business is real. That starts with three basics: a legal business entity, a federal tax ID, and a business bank account. Just as important, all of them need to point to the same business identity.

These records are what bureaus and lenders use to report, match, and verify accounts. If your business isn’t easy to find on paper, things can stall fast. Once your business is legally visible, every record needs to line up.

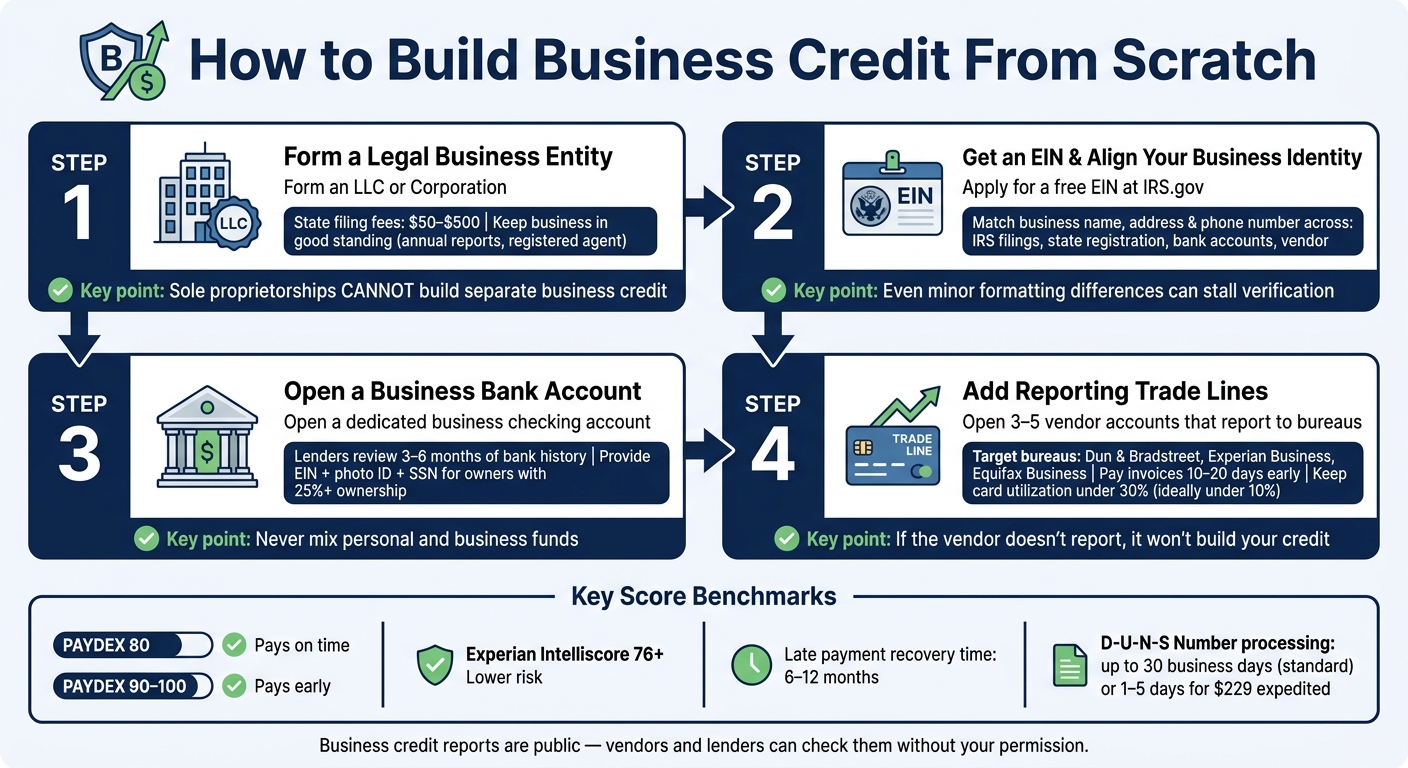

Form an LLC or Corporation and Keep It in Good Standing

A sole proprietorship vs. LLC comparison shows that a sole proprietorship can’t build credit apart from the owner. As Yossi Eldad, Product Manager at Lili, puts it:

"As a sole proprietorship, your business does not have a separate legal entity. That means it cannot build its own business credit profile."

An LLC or corporation gives your business its own legal identity, which means it can build its own credit file. In the U.S., state filing fees usually range from $50 to $500, depending on the state. You may also need to pay annual report fees and other compliance costs over time.

After you form the business, you need to keep it in good standing. That usually means filing annual reports, paying state fees on time, and keeping a registered agent in place. If the state administratively dissolves the business, lenders may not be able to verify it.

Once the entity is set, the next piece is making sure your EIN and contact details match everywhere.

Get an EIN and Use Consistent Business Contact Details Everywhere

An Employer Identification Number (EIN) is your business’s federal tax ID. It’s used in place of your personal SSN for bank accounts, tax filings, payroll, and credit applications. You can get one for free directly at IRS.gov.

This is where small mistakes can cause big headaches. Your business name, address, and phone number should match across:

- IRS filings

- State registration

- Bank accounts

- Vendor applications

- Credit bureau profiles

Even minor formatting differences can slow down verification. A business phone line and an email address that matches your domain can also help lenders confirm the business is legit.

Use an address lenders can verify, like a commercial suite or registered agent address. A dedicated business phone line listed in 411 directories can strengthen that match even more.

With your business easy to identify, the last part of the setup is a bank account used only for business activity.

Open a Business Bank Account and Keep Business Money Separate

A business checking account separates your business finances from your personal finances and starts your banking history. That matters because many lenders look at 3 to 6 months of business bank statements.

When you open the account, expect to provide:

- Your EIN

- A government-issued photo ID

- Social Security numbers for each beneficial owner with 25% or more ownership

Federal ownership-verification rules require banks to collect ID and ownership details for major owners.

Once the account is open, keep it clean. Don’t pay personal expenses from the business account. Mixing funds weakens the legal separation your LLC or corporation was meant to create.

With the entity, EIN, and bank account in place, you’re ready to open accounts that report payment history.

sbb-itb-ba0a4be

Create Your Business Credit Profile With the Major Bureaus

Once your entity, EIN, and bank account are set up, make sure the credit bureaus can actually find your business and start a file. This part matters more than many people think. If your business details don’t match across systems, your profile can end up scattered or hard to locate.

Each bureau builds files a little differently.

Apply for a D-U-N-S Number and Check Your Experian Business and Equifax Business Profiles

Dun & Bradstreet requires you to register on purpose. Apply for a D-U-N-S number – a free, nine-digit business identifier – as soon as your entity is formed. Standard processing can take up to 30 business days. If you need it sooner, D&B also offers expedited processing for about $229, which usually takes 1–5 business days.

Use the exact same business details on your D&B application. Same business name. Same address. Same phone number. It sounds small, but this is where many files get messy.

Experian Business and Equifax Business usually begin building your profile on their own after vendors, lenders, or credit card issuers start reporting payment activity. Go to each bureau’s business portal, claim your profile, and confirm that your business name, address, and phone number are correct.

Once the bureaus can identify your business, you can move on to opening accounts that report payment history.

Understand the Scores That Drive Business Credit Decisions

These are the scores lenders look at most often.

| Bureau | Score Name | Score Range | Main Focus | How To Improve |

|---|---|---|---|---|

| Dun & Bradstreet | PAYDEX | 0–100 | Payment timing – how early or late you pay | Pay invoices 10–20 days before the due date |

| Experian Business | Intelliscore Plus | 1–100 | Risk of severe delinquency | Keep credit utilization low and maintain steady on-time payments |

| Equifax Business | Business Credit Risk Score | 101–992 | Likelihood of severe delinquency or failure | Make sure all trade lines report steadily and avoid liens or public records |

A few score benchmarks are worth knowing:

- A PAYDEX score of 80 means you pay on time. To score above 80, you need to pay early.

- For Experian Intelliscore Plus, a score of 76 or higher is usually seen as low risk.

- To get a PAYDEX score at all, D&B needs at least two trade lines and three trade experiences on file.

One more thing: business credit reports are public. Vendors and lenders can check them without asking for your permission.

With your bureau profiles set up, the next move is building trade lines through vendor accounts and starter credit.

Build Your First Payment History With Vendor Accounts and Starter Credit

Start With Net-30 Vendors That Report to Business Credit Bureaus

Once your bureau profiles are live, it’s time to open reporting trade lines.

Net-30 accounts let you buy now and pay within 30 days. For a new business with no credit history, they’re often the easiest place to start. Why? Many vendors approve you based on your business details alone, without a personal credit check or a long time in business.

One thing matters more than anything else here: make sure the vendor reports. Before you place an order, get written confirmation that the account reports to D&B, Experian Business, or Equifax Business. If it doesn’t report, it won’t help build your credit file.

Here are six vendors often used for starter trade lines:

| Vendor | Typical Products | Net Terms Offered | Reports To | Best Use Case |

|---|---|---|---|---|

| Uline | Shipping, packaging, industrial supplies | Net-30 | D&B, Experian, Equifax | Startups needing shipping materials |

| Quill | Office supplies, paper, cleaning products | Net-30 | D&B, Experian | General office needs |

| Grainger | Industrial, safety, MRO supplies | Net-30 | D&B, Experian, Equifax | Maintenance and safety equipment |

| Crown Office Supplies | Office supplies, stationery | Net-30 | D&B, Experian, Equifax | Brand-new businesses; easy approval |

| The CEO Creative | Marketing and branding materials | Net-30 | D&B, Experian, Equifax | Service-based businesses |

| Summa Office Supplies | Paper, folders, copy supplies | Net-30 | D&B, Experian | Fast reporting for credit building |

A good target is 3 to 5 reporting trade lines. That’s usually enough to help generate your first PAYDEX score. When you check out, choose invoice billing or Net-30 terms instead of paying by card. That way, the account reports as trade credit.

Payment timing matters a lot. Pay each invoice 10 to 20 days before the due date. Paying on time can earn a PAYDEX of 80, while paying early can move it into the 90–100 range.

You also need activity. Try to make at least one small purchase on each account every month, usually around $50 to $100. If an approved account sits unused for 60 days, it may stop reporting.

Add a Business Credit Card and Keep Utilization Low

After a few months of vendor payments are reporting, the next step is revolving credit.

Once you’ve built 3 to 5 vendor trade lines and have 3 to 6 months of steady payment history, you’re in a better spot to apply for a business credit card. Most major issuers want to see that kind of track record before they approve a new business.

If you get denied for an unsecured card, don’t panic. A secured business credit card can still help you build revolving credit history.

For unsecured cards, lenders often look at:

- A personal credit score of about 680 or higher

- At least 6 months in business

- Steady business bank deposits

Many unsecured business credit cards also require a personal guarantee. That means you’re personally on the hook if the business defaults.

Once you’re approved, keep your credit utilization under 30%. Under 10% is even better. And pay the full statement balance every month.

Match Each Account Type to the Right Expenses and Avoid Early Mistakes

Use vendor accounts for routine purchases, and use a business credit card for expenses that change month to month.

This first year is where things can feel a little shaky. Business credit is still thin, and one mistake can hit hard. A single 30-day-late payment can drop a PAYDEX score from the high 80s to the low 70s. Getting back from that can take six to twelve months of perfect payments afterward.

That’s why it helps to move with some restraint. Open accounts gradually, no more than one vendor account per week. Keep balances low. And avoid collections at all costs.

Once the accounts start reporting, check each bureau file line by line. If a trade line is missing or the details are wrong, fix it early before the errors pile up.

Monitor Your Reports, Fix Errors, and Keep Your Business in Good Standing

Review D&B, Experian Business, and Equifax Business Reports for Errors and Missing Trade Lines

Once your first trade lines start reporting, check the files lenders are likely to review. Pull reports from D&B, Experian Business, and Equifax Business at least once per quarter.

Mistakes show up more often than most owners expect. You might see the wrong payment status, mixed records from a similar company, or trade lines that never appeared at all. Review each report for late payments that were actually paid on time, accounts that don’t belong to your business, old liens or judgments that should no longer be there, and missing trade lines. Also check that your business name, address, and phone number match exactly across all three reports.

If you spot an error, send a dispute to the bureau that shows it. Each bureau handles disputes on its own, so a fix on your D&B file won’t automatically update Experian Business. Include invoices, bank statements, and proof of payment. Bureaus usually investigate and resolve disputes within 30 days. If they can’t verify the item, they remove it.

If a vendor payment is missing from your file altogether, use D&B’s trade reference submission. That can help when a vendor you’ve been paying doesn’t report on its own.

Request Higher Limits, Add New Accounts, and Stay Compliant as Your Profile Grows

After you’ve cleaned up your reports, the next move is building more depth.

When a vendor account is at least 6 months old and has a clean payment record, ask for a higher credit limit. Repeat that every 6–12 months. Higher limits can improve your credit depth and show future lenders that your business can handle more credit. If you decide to apply for business credit cards, submit those applications within a short window to reduce the effect on your personal credit.

You’ll also want to keep your registered agent, filings, and state records up to date.

Conclusion: A Clear Path From Zero Business Credit to Better Financing

Each step matters. Choosing vendors that report, checking your files, fixing bad data, and keeping your LLC in good standing all add up to a credit profile that lenders and vendors can verify on their own. Over time, that reporting history gives a new business file more weight when it’s time to look for financing.

FAQs

How long does it take to build business credit?

Building business credit takes time. It doesn’t happen overnight.

If you take steady steps like forming a legal entity, getting an EIN, opening a business bank account, adding reporting net-30 vendor or trade lines, and paying on time, many businesses can build a fundable profile in about 6–12 months.

If you’re starting from zero, expect it to take longer. In many cases, a more complete profile takes around 12–18 months.

Can I build business credit without a personal guarantee?

Yes, but it usually takes time.

Most early-stage business credit cards and loans still require a personal guarantee. That means lenders look at you, not just your company.

If you want financing based on the business alone, you’ll usually need to:

- form a legal business entity

- get an EIN

- build a steady record of on-time payments

After 12 to 24 months of responsible activity, some lenders may start looking at the business on its own.

What if my vendors do not report to business credit bureaus?

If a vendor doesn’t report your payments to the major business credit bureaus, that account won’t help build your business credit profile.

Before you open an account, check that the supplier reports to at least one major bureau: Dun & Bradstreet, Experian Business, or Equifax Business. If they don’t, put your attention on vendors that do report, such as Uline, Quill, or Grainger.