Choosing the right LLC tax election for S Corp taxation can reduce self-employment taxes by splitting income into two parts: a reasonable salary (taxed at 15.3%) and distributions (not subject to self-employment tax). However, this comes with additional costs, including payroll, quarterly filings, and tax preparation fees. Understanding how to file taxes for an LLC is essential before making this switch.

- Key Savings: For profits of $100,000, you could save around $7,500 annually after compliance costs.

- Break-Even Point: S Corp benefits typically start when profits exceed $60,000–$80,000.

- Compliance Costs: Expect annual expenses of $1,500–$4,500 for payroll and filings.

- Risks: Failure to pay a "reasonable salary" can trigger IRS audits.

This tax strategy works best for businesses with steady profits over $60,000. Below that, the added costs often outweigh the savings. Always consult a tax professional to ensure this approach aligns with your financial goals and state-specific rules.

How LLCs and S Corps Are Taxed

Default LLC Taxation

When you set up an LLC, the IRS automatically classifies it as a "disregarded entity." For a single-member LLC, this means it’s taxed like a sole proprietorship. If the LLC has multiple members, it’s taxed as a partnership. In both cases, the profits pass directly to your personal tax return.

Here’s the catch: you’ll owe a 15.3% self-employment tax on your net profits, though you can lower this by claiming tax deductions for LLC owners. This tax covers 12.4% for Social Security (up to $184,500 in earnings for 2026) and 2.9% for Medicare. For instance, if your LLC brings in $80,000 in net profit, you’d pay roughly $12,240 in self-employment tax – before factoring in income taxes. The upside? You don’t need to worry about running payroll or filing W-2 forms under this setup.

But what if you want to reduce that self-employment tax burden? That’s where electing S Corp status comes into play.

S Corporation Tax Election Explained

Choosing S Corp status doesn’t change your LLC’s legal structure – it’s purely a federal tax decision. By filling out IRS Form 2553, your LLC stays the same under state law, but it gets taxed like an S Corporation at the federal level.

This election allows you to split your income into two parts: a reasonable salary (subject to the 15.3% payroll tax) and shareholder distributions (which are exempt from self-employment tax). For example, if your LLC earns $100,000, you could pay yourself a $50,000 salary and take the other $50,000 as distributions. This setup could save you around $7,500 annually in self-employment taxes – before accounting for compliance costs.

However, there are strings attached. S Corp status requires you to run a formal payroll, file quarterly Form 941s, and submit a separate corporate tax return (Form 1120-S). The IRS also insists that your salary be "reasonable" based on industry norms – usually between 30% and 50% of your net profits. If you set your salary too low to maximize distributions, you risk audits and penalties.

To clarify the differences, here’s a quick comparison: Feature LLC (Default) LLC Taxed as S Corp

Understanding these tax treatments lays the groundwork for evaluating the potential benefits and compliance requirements in future sections.

Benefits of S Corp Taxation for LLCs

Lower Self-Employment Taxes

One of the biggest perks of choosing S Corp taxation is the potential to cut down on self-employment taxes. Typically, LLC owners pay a 15.3% self-employment tax on their entire profit. However, with S Corp status, you only pay this tax on your salary. The rest of the income, taken as distributions, isn’t subject to self-employment tax.

Here’s an example: Imagine your LLC earns $150,000 in profit annually. As a standard LLC, you’d owe $22,950 in self-employment taxes. But with S Corp status, you might pay yourself a $60,000 salary and take $90,000 as distributions. This setup reduces your self-employment tax to about $9,180 – a savings of over $13,000 (before considering compliance costs). This is why many small business owners start exploring S Corp taxation when their profits reach a level where these strategies make sense.

It’s important to ensure your salary aligns with industry standards to avoid drawing attention from the IRS. Using resources like the Bureau of Labor Statistics or Glassdoor can help you determine a reasonable salary for your role.

Beyond lowering self-employment taxes, S Corp status provides additional tax benefits.

Pass-Through Taxation and QBI Deduction

S Corps retain the pass-through taxation structure that LLCs already enjoy. This means your business profits flow directly to your personal tax return, avoiding corporate-level taxes. Additionally, you may qualify for the Qualified Business Income (QBI) deduction, which can reduce your taxable income by up to 20%.

However, the QBI deduction only applies to the distributions portion of your income – not your W-2 wages. According to Tom Woolley, MBA at Today CFO, the tax savings from S Corp status often outweigh the slightly reduced QBI deduction. For instance, if you earn $150,000 and allocate $75,000 as salary, you might lose about $3,600 in QBI deduction value (assuming a 24% tax bracket). But you’d still save around $9,593 in self-employment taxes.

Keep in mind that the QBI deduction starts phasing out in 2026 for single filers earning $191,950 or more, and for married couples filing jointly at $383,900. This is especially relevant for specified service businesses like consulting, law, or medicine. If you’re nearing these income thresholds, structuring your payroll carefully can help you meet the wage requirements to maximize the deduction.

While enjoying these tax benefits, your LLC’s liability protection remains intact with S Corp status.

Flexibility with LLC Liability Protection

Electing S Corp status doesn’t change your LLC’s legal structure. You’ll still have the same liability protection, which keeps your personal assets safe from business debts or lawsuits. This setup offers more flexibility compared to forming a C Corporation, as you avoid double taxation and don’t need to deal with complex corporate requirements like board meetings or shareholder resolutions. Your LLC’s operating agreement and management structure remain unchanged.

The trade-off? You’ll face additional administrative tasks. As an "employee-shareholder", you’ll need to manage payroll, file quarterly Form 941s, and submit a separate corporate tax return (Form 1120-S). Still, for many business owners earning over $60,000 in annual profit, the tax savings from S Corp status often outweigh the added paperwork.

Drawbacks and Compliance Requirements

While choosing S Corp taxation can help reduce taxes, it also brings additional compliance requirements that could offset some of the savings.

Higher Administrative Costs

Switching to S Corp taxation means taking on more administrative work – and the associated costs. For starters, you’ll need to manage formal payroll for yourself, file quarterly Form 941s, and submit an annual Form 1120-S. These tasks aren’t free. On average, they can cost anywhere from $1,200 to $9,900 annually when you factor in payroll services, tax preparation, and bookkeeping.

California business owners face an extra challenge: the state imposes an $800 minimum franchise tax every year, even if the business doesn’t turn a profit. For startups or businesses with slim profit margins, these compliance costs can quickly eat into any tax savings. In short, while these administrative expenses are manageable, they’re an important part of the bigger picture when considering S Corp taxation.

And that’s just the start. IRS salary rules add another layer of complexity.

IRS Reasonable Salary Rules

The IRS has strict guidelines about paying yourself a reasonable salary before taking distributions. While there’s no official percentage, many tax experts recommend allocating 40% to 60% of your net business income as your salary.

"The IRS actively targets unreasonably low salaries. A business generating $200,000 while paying the owner $30,000 will almost certainly trigger audit." – IRSProb.com

If the IRS decides your salary is too low, they can reclassify your distributions as wages. This could lead to back payroll taxes, penalties, and interest on the reclassified amounts. To avoid this, it’s wise to document your salary decisions using reliable data sources like Bureau of Labor Statistics reports or industry-specific surveys. Following these steps can help you stay compliant and avoid costly mistakes.

State Tax Implications

State-specific rules add yet another wrinkle to the S Corp equation. Not all states treat S Corps the same way. For instance, New York City doesn’t recognize S Corp status at all, taxing these businesses as C Corps. Meanwhile, Illinois imposes a 1.5% replacement tax on S Corp income, and California adds a 1.5% tax on net income in addition to its $800 franchise fee.

Some states, like New Jersey, even require a separate state-level S Corp election. Forgetting to file that election could result in your business being taxed as a C Corp at the state level, even if it’s treated as an S Corp federally. Before making the switch, it’s crucial to check whether your state recognizes S Corp status and account for any extra taxes or fees that could impact your savings.

These administrative hurdles, salary rules, and state-specific requirements highlight why it’s essential to carefully evaluate whether S Corp taxation is the right fit for your business.

sbb-itb-ba0a4be

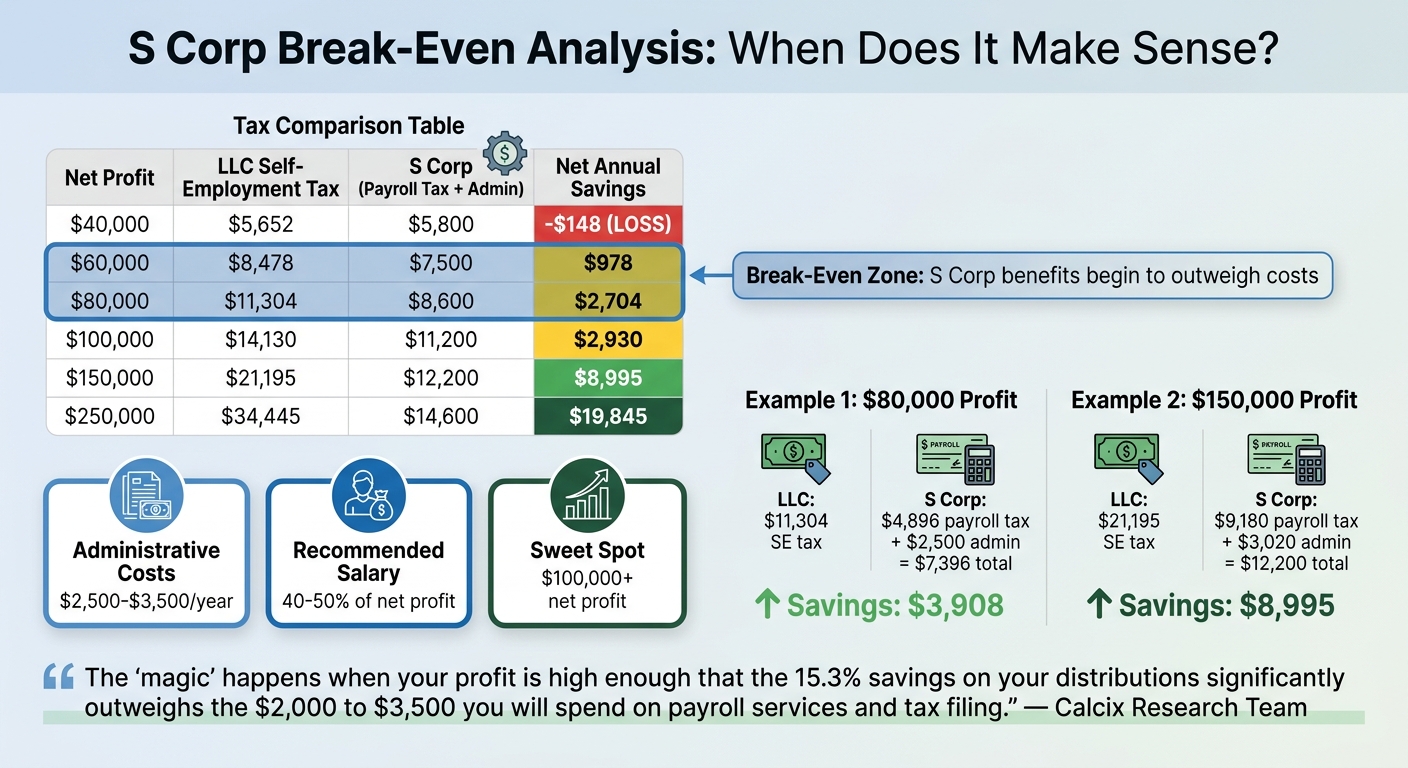

How to Calculate Your Break-Even Point

To figure out if S Corp taxation is worth it for your business, you need to compare potential tax savings against the additional costs involved. This depends on factors like your profit level, what counts as a reasonable salary, and essential business services that impact your administrative expenses. Let’s break down the income levels where S Corp benefits start to outweigh those extra costs.

The Break-Even Income Range

S Corp advantages generally kick in when your net profits fall between $60,000 and $80,000. Below this range, the annual administrative costs (around $2,500–$3,500) can cancel out any savings. Once your profits exceed $100,000, the benefits grow significantly, with some scenarios showing savings close to $9,000 or more.

"The ‘magic’ happens when your profit is high enough that the 15.3% savings on your distributions significantly outweighs the $2,000 to $3,500 you will spend on payroll services and tax filing." – Calcix Research Team

This calculation builds on earlier discussions about tax strategies and compliance considerations.

Example Calculation

Here’s how the numbers play out in practice:

- $80,000 profit:

With default LLC taxation, you’d pay about $11,304 in self-employment taxes. Under S Corp rules, assuming a $32,000 salary and $2,500 in administrative costs, payroll taxes would total around $4,896, bringing your total S Corp costs to approximately $7,396. That translates to net savings of about $3,908 compared to LLC taxation. - $150,000 profit:

Default LLC taxation would result in roughly $21,195 in self-employment taxes. With S Corp election and a $60,000 salary, total payroll taxes and compliance costs would come to around $12,200, leaving you with net savings of approximately $8,995.

Tax Comparison Table: LLC vs. S Corp

Here’s a quick look at how costs and savings stack up across different profit levels: Net Profit LLC SE Tax S Corp Payroll Tax + Admin Costs Net Annual Savings

These figures assume a reasonable salary falls between 40% and 50% of profits, with administrative costs ranging from $2,500 to $3,500. Your actual savings might vary depending on how you set your salary and meet state-specific requirements. However, the trend is clear: as your profits rise above the break-even point, the savings grow larger.

When S Corp Election Doesn’t Make Sense

While S Corp taxation can offer tax savings for certain businesses, it’s not a one-size-fits-all solution. In some situations, opting for S Corp status can actually work against your business goals. Here are some scenarios where it may not be the right choice.

Low-Profit or Startup Businesses

For businesses earning less than $50,000–$60,000 annually, S Corp election often costs more than it saves. The administrative expenses alone – such as payroll processing ($500–$2,400 per year), preparing Form 1120-S ($1,000–$3,000), and additional bookkeeping – can add up to $2,000 to $4,500 annually. For smaller businesses, these fixed costs can wipe out any potential tax benefits.

"For a $50,000 business, the simplicity might win. For a $150,000 business, you’re likely overpaying by thousands." – SDO CPA

In addition, the requirement to pay yourself a reasonable salary can severely limit distributions. For instance, if your business earns $45,000 in profit and you allocate $35,000 as your salary, you’re left with just $10,000 for distributions. That’s hardly enough to justify the added administrative burden. Plus, startup losses are often harder to deduct under S Corp rules because shareholders can’t use entity-level debt to increase their tax basis.

Businesses with Fluctuating or Passive Income

S Corp status works best for businesses with steady, predictable income. If your revenue fluctuates significantly from month to month, managing payroll can become a headache. S Corp owners are required to process payroll and make tax deposits regardless of cash flow, which can be especially challenging during lean months.

For businesses with passive income – like rental properties, royalties, or investment earnings – S Corp taxation offers little benefit. The tax savings from splitting income into salary and distributions only apply to active business income. Passive income doesn’t fit this model, and forcing it into an S Corp structure adds unnecessary complexity without delivering tax advantages. Additionally, if an S corporation has excess passive investment income and was previously a C corporation, it may face corporate-level taxes under Section 1375.

Multi-Member LLCs with Unequal Ownership

S Corps require profits to be distributed strictly according to ownership percentages. For multi-member LLCs where partners contribute varying levels of capital, time, or expertise, this rigid structure can cause problems. Standard LLCs allow for flexible allocations, enabling partners to receive distributions based on their actual contributions. S Corps, however, don’t permit this flexibility – a 60% owner must receive 60% of all distributions, no exceptions.

This lack of flexibility can make it difficult to address differing salary needs or reward sweat equity differently from financial investments. For partnerships that rely on adaptable profit-sharing arrangements, sticking with default LLC taxation is often the better choice. These factors play a crucial role in determining whether S Corp status aligns with your business strategy.

Conclusion

Choosing S Corp taxation for your LLC could save you anywhere from $5,000 to $20,000+ annually, provided your net profit justifies the costs. This works by splitting income into a reasonable salary – subject to the 15.3% self-employment tax – and distributions that are exempt from that tax. However, this setup comes with annual compliance costs ranging from $1,500 to $4,500.

Not all businesses will benefit equally. Generally, businesses with net profits exceeding the break-even point are the best candidates. Those earning over $100,000 in net profit often see the most savings. It’s also important to consider state-specific taxes, which can impact your overall savings. Understanding these thresholds is key to deciding if S Corp taxation is right for your business.

"The decision between LLC default taxation and S Corp taxation depends on which aligns with your financial profile." – Landau Lang, Director of Research & Strategy, Crane Financial

This insight underscores the importance of seeking professional advice. A tax professional can help you evaluate your options before filing Form 2553. They can assist in determining a defensible salary using data from the Bureau of Labor Statistics, assess how this decision impacts your Qualified Business Income deduction, and navigate state-level tax considerations. Timing is also critical – if your business operates on a calendar year, the deadline to file Form 2553 is March 15.

While S Corp taxation can offer meaningful financial benefits, it can also lead to unnecessary costs if applied incorrectly. Carefully calculate your break-even point, account for state tax rules, and consult a professional to ensure the S Corp election aligns with your business needs.

FAQs

What counts as a “reasonable salary” for an S Corp owner?

A “reasonable salary” for an S Corp owner is what someone in a similar role and industry would normally earn. The IRS requires you to pay yourself this salary to stay compliant and avoid penalties. It should represent the fair market value of the work you do for the business.

How do I estimate my LLC-to-S Corp break-even profit?

To figure out your LLC-to-S Corp break-even profit, you’ll need to determine when the tax savings from lower self-employment taxes outweigh the additional expenses, such as payroll and compliance costs. Generally, this happens when your net profit reaches $40,000 to $50,000 after covering a reasonable salary for yourself. The key benefit comes from how profits above your salary are taxed – only once as distributions – making the S Corp election a smart move as your income grows.

What state taxes or fees could reduce my S Corp savings?

State taxes and fees – such as income taxes, franchise taxes, or other charges specific to businesses – vary widely depending on where your business operates. These additional costs can chip away at the tax savings that come with choosing S Corp status. When weighing the advantages of this tax structure, it’s crucial to factor in these expenses to determine if it truly supports your financial objectives.