Corporate tax policies in the U.S. vary widely by state, impacting businesses differently depending on their location. Here’s what you need to know:

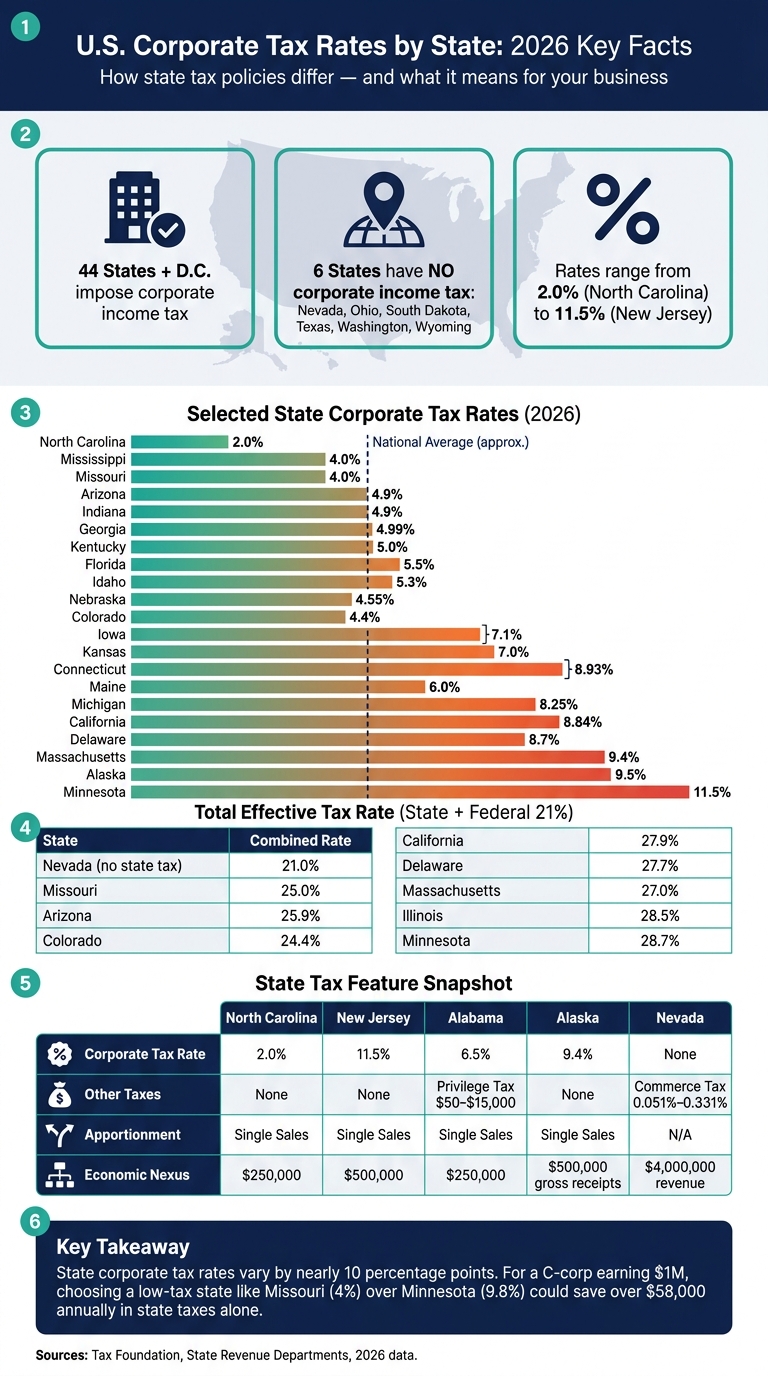

- Corporate Income Tax: 44 states and Washington, D.C. impose corporate income taxes, while six states (Nevada, Ohio, South Dakota, Texas, Washington, and Wyoming) do not.

- Tax Rates: Rates range from 2% in North Carolina to 11.5% in New Jersey in 2026.

- Additional Taxes: Some states levy other taxes like franchise taxes, gross receipts taxes, or privilege taxes.

- Apportionment Methods: States use different formulas (e.g., single sales factor) to calculate taxable income for multistate businesses.

- Tax Incentives: Many states offer credits, deductions, or exemptions to attract businesses.

- Economic Nexus: Thresholds for tax liability vary, often based on in-state sales or transactions.

Quick Comparison

| State | Corporate Tax Rate | Other Taxes | Apportionment | Economic Nexus |

|---|---|---|---|---|

| North Carolina | 2.0% | None | Single sales factor | $250,000 in sales |

| New Jersey | 11.5% | None | Single sales factor | $500,000 in sales |

| Alabama | 6.5% | Privilege Tax ($50–$15,000) | Single sales factor | $250,000 in sales |

| Alaska | 9.4% | None | Single sales factor | $500,000 in gross receipts |

| Nevada | None | Commerce Tax (0.051%–0.331%) | N/A | $4,000,000 in revenue |

This overview highlights the complexity and diversity in state tax systems. Businesses must carefully assess tax rates, additional levies, and available incentives when deciding where to operate.

1. Alabama

Alabama applies a flat corporate income tax rate of 6.5% on net income earned within the state. This rate has remained unchanged since January 1, 2001, and is higher than neighboring states like Mississippi (5.0%), Georgia (5.75%), and Florida (5.5%). However, the actual tax burden can be lower than the headline rate suggests.

One key factor is that corporations in Alabama can deduct all federal income taxes paid or accrued from their state taxable income. This deduction effectively reduces the overall tax liability below the statutory 6.5% rate.

In addition to corporate income tax, Alabama imposes an annual Business Privilege Tax (BPT). This tax is based on a company’s net worth apportioned to the state, with rates ranging from $0.25 to $1.75 per $1,000 of net worth. The BPT has a minimum tax of $50 and is capped at $15,000 per year for most businesses. Because the tax is calculated on net worth rather than profitability, even companies with lower income but significant assets may be subject to it.

Starting with tax years beginning on or after January 1, 2021, Alabama adopted a single sales factor for income apportionment. This method considers only in-state sales when calculating taxable income, which can benefit companies – like manufacturers or distributors – that have significant operations in Alabama but serve customers outside the state. The state also enforces an economic nexus threshold of $250,000 in annual in-state sales.

| Tax Type | Rate/Range | Key Detail |

|---|---|---|

| Corporate Income Tax | 6.5% (flat) | Federal income taxes are fully deductible |

| Business Privilege Tax | $0.25 – $1.75 per $1,000 net worth | Minimum of $50; capped at $15,000 for most entities |

| Minimum Corporate Income Tax | $0 | No minimum required |

| Apportionment Method | Single sales factor | Based solely on in-state sales; $250,000 nexus threshold |

Alabama does not impose a minimum corporate income tax, which can be particularly advantageous for startups or businesses operating at a loss. Moreover, the state offers targeted incentives, such as the Enterprise Zone and Growing Alabama Credits, to attract and support businesses. These programs underscore Alabama’s efforts to create a competitive and appealing tax environment for companies considering where to establish or expand their operations.

Next, let’s take a closer look at Alaska’s corporate tax structure.

sbb-itb-ba0a4be

2. Alaska

Alaska employs a graduated corporate income tax system with ten brackets, starting at 1% for the first $10,000 of taxable income and climbing to a top rate of 9.4% for income over $90,000. This top rate places Alaska fifth nationally as of 2026, comparable to Illinois (9.5%) and Minnesota (9.8%), making it one of the pricier states for C-corporations. When combined with the federal corporate tax rate of 21%, the effective tax burden for top-tier C-corporations in Alaska reaches 28.3%.

| Taxable Income | Tax Rate |

|---|---|

| $0 – $10,000 | 1.0% |

| $10,001 – $20,000 | 2.0% |

| $20,001 – $30,000 | 3.0% |

| $30,001 – $40,000 | 4.0% |

| $40,001 – $50,000 | 5.0% |

| $50,001 – $60,000 | 6.0% |

| $60,001 – $70,000 | 7.0% |

| $70,001 – $80,000 | 8.0% |

| $80,001 – $90,000 | 9.0% |

| Over $90,000 | 9.4% |

Despite its corporate tax rates, Alaska offers some relief in its overall tax landscape. The state has no personal income tax and no state-level sales tax, which can be a big advantage for owners of flow-through entities like S-corporations, partnerships, or LLCs. These entities avoid double taxation by passing income directly to owners’ personal tax returns, avoiding Alaska’s corporate tax altogether. For businesses weighing options between Alaska and states that impose both corporate and personal income taxes, this absence of additional layers can make a notable difference.

In March 2026, the Alaska Senate passed an amendment, spearheaded by Sen. Forrest Dunbar (D-Anchorage), applying the 9.4% corporate tax rate to oil and gas S-corporations with taxable income exceeding $5 million. This measure is projected to generate over $100 million annually. Additionally, legislation enacted in May 2026 targets online businesses, such as Netflix and Facebook, that earn significant revenue from Alaskan consumers without maintaining a physical presence in the state. This law is expected to bring in $10 million to $15 million annually. As Sen. Bill Wielechowski put it:

"This bill is a small step toward leveling the playing field [between out-of-state online businesses and local businesses]."

These legislative updates reflect Alaska’s evolving corporate tax framework, addressing both traditional industries and the growing digital economy. The state has also set an economic nexus threshold of $500,000 in annual gross receipts. Remote sellers and digital service providers exceeding this threshold must file taxes, even if they lack physical property or payroll in Alaska. With the state actively pursuing market-based sourcing, this is an area businesses should watch closely.

3. Arizona

Arizona applies a flat corporate income tax rate of 4.9%. There are no graduated tax brackets, no corporate franchise tax, and no alternative minimum tax (AMT). When combined with the federal corporate tax rate of 21%, Arizona C-corporations face an effective tax rate of 25.9%.

To put this into perspective, Arizona’s rate is nearly 4 percentage points lower than California’s 8.84% rate. For a business generating $1 million in C-corp income, this difference could result in approximately $39,500 in annual state tax savings for companies relocating from California to Arizona.

"Arizona’s corporate income tax difference (8.84% vs 4.9%) is the line most worth modeling for a profitable C-corp." – Ontrack Moving

Another appealing feature for multistate businesses is Arizona’s flexibility in choosing an apportionment method each year. Corporations can opt for either a single sales factor (100% based on sales) or a three-factor formula that considers property, payroll, and double-weighted sales. Businesses with substantial in-state infrastructure but primarily out-of-state customers often find the single sales factor advantageous, making it worthwhile to reassess these methods annually.

For S-corporations, Arizona offers an elective Pass-Through Entity (PTE) tax rate of 2.5%. Additionally, businesses can carry forward net operating losses (NOL) for up to 20 years, although carrybacks are not permitted. Starting with the 2025 tax year, Arizona will require corporate income tax returns to be filed electronically.

| Tax Feature | Arizona Policy |

|---|---|

| Corporate Income Tax Rate | 4.9% (Flat) |

| Franchise Tax | None |

| Alternative Minimum Tax (AMT) | None |

| Pass-Through Entity (PTE) Tax | 2.5% (Elective for S-Corps) |

| NOL Carryforward | 20 years; no carryback |

| Economic Nexus Threshold | $100,000 in annual in-state sales |

With its competitive tax policies and flexibility, Arizona stands out as a favorable option for businesses exploring relocation. Next, let’s dive into Arkansas’s corporate tax structure.

4. Arkansas

Arkansas uses a graduated corporate income tax system, where the tax rate increases with net income. Starting January 1, 2024, the top rate is set at 4.3% for net income exceeding $11,000. The state has adjusted its rates in recent years to stay competitive.

| Net Income Bracket | Tax Rate |

|---|---|

| First $3,000 | 1.0% |

| $3,001 – $6,000 | 2.0% |

| $6,001 – $11,000 | 3.0% |

| Over $11,000 | 4.3% |

(Source: Arkansas Code § 26-51-205)

Since 2021, Arkansas has significantly lowered its top corporate income tax rate, dropping from 6.2% in 2021 to 5.9% in 2022, 5.1% in 2023, and now 4.3% in 2024. For example, a C-corporation with $1 million in earnings now saves around $19,000 annually compared to what it paid in 2021.

Arkansas has also updated how it taxes multistate businesses. Beginning January 1, 2026, the state transitioned from the "cost of performance" method to market-based sourcing for sales of services and intangibles. Under this system, income is allocated based on the customer’s location rather than where the service or intangible was performed.

"The Act aligns Arkansas with other states by adopting Market-Based Sourcing for Sales of Services and Intangibles, which is based on the location where they are delivered to the customer." – Arkansas Department of Finance and Administration

This shift is advantageous for companies with customers primarily outside Arkansas. However, providers of telecommunications, internet access, and cable television services can choose to stick with the "cost of performance" method until December 31, 2035.

For pass-through entities, Arkansas offers an optional Pass-Through Entity Tax (PTET), allowing businesses to pay taxes at the entity level instead of passing the liability to individual members. Additionally, for tax years beginning on or after January 1, 2021, net operating losses can be carried forward for up to 10 years, though carrybacks are not permitted.

Before we dive into California’s unique corporate tax system, you may want to compare business formation services to ensure your entity is structured correctly for these state-specific rules.

5. California

California charges a flat 8.84% tax rate on C-corporations, making it the 9th highest in the U.S.. S-corporations, however, benefit from a reduced rate of 1.5% on net income. All corporations operating in the state must pay an $800 annual minimum franchise tax, which is waived for the first year, regardless of the company’s activity or profitability. This tax structure, coupled with federal taxes, shapes the overall financial burden for corporations.

When combined with the federal corporate tax rate of 21%, C-corporations in California face a total effective tax rate of 27.9%, which is about 7 percentage points higher than states without corporate income taxes.

| Tax Feature | Rate / Detail |

|---|---|

| C-Corporation Rate | 8.84% (flat) |

| S-Corporation Rate | 1.5% |

| Minimum Franchise Tax | $800/year (waived 1st year) |

| Alternative Minimum Tax (AMT) | 1.5% |

| Apportionment Method | Single Sales Factor |

| Economic Nexus Threshold | $601,967 in annual sales |

| Combined State + Federal Rate | 27.9% |

California’s single sales factor apportionment plays a big role in how businesses view the state’s tax competitiveness. This method bases taxes entirely on in-state sales. For companies considering relocation, this can be a challenge:

"A corporation moving its headquarters or other locations out of state will not reduce its tax liability as long as it continues to make sales to California’s customer base." – Kayla Kitson, California Budget & Policy Center

Interestingly, a study of over 100 corporations that announced plans to leave California revealed that 60% paid only the $800 minimum tax. Collectively, these companies ended up paying more in taxes to California the year after they left.

For the 2024–2026 tax years, California has implemented temporary measures to boost state revenue. These include suspending net operating loss (NOL) carryover deductions for corporations with taxable income over $1 million and capping business tax credits at $5 million per year. Large corporations with significant credit balances will need to adjust their tax strategies during this period.

6. Colorado

Colorado imposes a flat 4.40% corporate tax on the portion of federal taxable income attributed to the state. When combined with the federal corporate tax rate of 21%, businesses in Colorado face a total effective rate of 24.4%. This is noticeably lower than states like California (27.9%) or Minnesota (28.7%).

The state uses a single sales factor apportionment method, which bases tax liability solely on the proportion of in-state sales. This approach is particularly advantageous for businesses with substantial in-state operations. Below is a breakdown of Colorado’s key tax features:

| Tax Feature | Detail |

|---|---|

| Corporate Tax Rate | 4.4% (flat) |

| Combined Rate (State + Federal) | 24.4% |

| Apportionment Method | Single Sales Factor (100% of receipts) |

| Economic Nexus Threshold | $100,000 in annual sales |

| Pass-Through Entity Option | SALT Parity Act election at 4.4% for S-corporations, LLCs, and partnerships |

| Alternative Gross Receipts Tax | Repealed effective July 1, 2025 |

Colorado also sets an economic nexus threshold of $100,000 in annual in-state sales. Once this threshold is exceeded, businesses are required to file taxes, even without a physical presence in the state. This requirement is a core component of sales tax nexus for online businesses.

For pass-through entities like S-corporations, LLCs, and partnerships, the SALT Parity Act election allows owners to claim federal tax deductions that might otherwise be unavailable. This option can be a valuable tool and is worth discussing with a tax professional.

Historically, Colorado’s corporate tax rate has decreased from 5.0% in 1994 to its current 4.4% as of 2022. The state’s TABOR Amendment, which limits government revenue, often leads to temporary rate reductions during surplus periods. This creates a stable and predictable tax environment, making Colorado attractive for long-term business planning.

With its streamlined tax policies and predictable framework, Colorado provides a solid foundation for businesses, setting the stage for further comparisons with other states.

7. Connecticut

Connecticut stands out with its dual-track tax system, offering businesses two ways to calculate their tax obligations. The state imposes a 7.5% corporate income tax on the net income of C-corporations operating within its borders. However, companies must pay the higher of two amounts: the net income tax (7.5%) or the Capital Base Tax, which is calculated based on the average value of a company’s capital stock and surplus.

The Capital Base Tax is being phased out over the next few years:

| Income Year | Capital Base Tax Rate |

|---|---|

| 2024 | 0.26% (2.6 mills) |

| 2025 | 0.21% (2.1 mills) |

| 2026 | 0.16% (1.6 mills) |

| 2027 | 0.11% (1.1 mills) |

| 2028 and after | 0.00% |

Additionally, businesses with annual gross income of $100 million or more are subject to a 10% surtax through 2028.

For LLCs and S-corporations, Connecticut provides an elective Pass-Through Entity Tax (PTET) at 6.99%. Understanding C-Corp vs S-Corp state tax policies is essential for choosing the right structure. This option allows businesses to sidestep the federal $10,000 SALT deduction cap. Another noteworthy feature is the reduced tax rate on business-use SaaS, which is taxed at just 1%, far below the standard 6.35% sales tax rate.

Out-of-state businesses should also be aware of Connecticut’s nexus rules. Any company with at least one employee in the state or more than $500,000 in income sourced from Connecticut is required to file a corporate tax return. These rules are especially important for businesses considering expansion or relocation.

For those navigating these tax complexities, platforms like BusinessAnywhere (https://businessanywhere.io) can simplify U.S. business registration, compliance, and ongoing management, making it easier to adapt to Connecticut’s tax framework.

8. Delaware

Delaware is a popular choice for business incorporation – it’s where over 60% of Fortune 500 companies, including Amazon, Alphabet, and Tesla, are registered. In fact, more than 90% of U.S.-based companies that went public in 2021 were incorporated in Delaware. However, it’s important to distinguish between incorporating in Wyoming, Delaware, or Nevada and actually conducting business there, as the tax implications can be quite different.

For corporations incorporated in Delaware but operating solely outside the state, there’s no state corporate income tax. However, these companies are still required to pay an annual Franchise Tax. On the other hand, businesses actively operating in Delaware are subject to an 8.7% corporate income tax on their federal taxable income allocated to the state. When combined with the federal corporate tax rate of 21%, the total effective tax rate comes to 27.7%.

"Many corporations incorporate in Delaware for legal reasons – favorable corporate law and the Court of Chancery – but incorrectly assume Delaware incorporation reduces their tax burden." – BermudaFin Editorial Team

Delaware also stands out for having no sales tax. Instead, the state imposes a Gross Receipts Tax (GRT) on sellers, which ranges from 0.0945% to 1.9914% depending on the type of business. This tax is applied to total revenue without deductions for costs, which can be particularly challenging for businesses with high revenue but low profit margins.

Here’s a breakdown of Delaware’s key business taxes and fees: Tax / Fee Rate or Cost Who Pays

Delaware offers another benefit for holding companies: those managing intangible assets like patents or trademarks and earning income from them may qualify for an exemption from the corporate income tax. To take advantage of this, companies must file Form CIT-EXM with the Division of Revenue for a formal ruling.

For businesses considering Delaware, proper structuring from the outset is crucial. The state’s tax system, which combines no sales tax with specific exemptions and requirements, makes it essential to understand its dual tax framework before making any decisions about relocation or operations.

9. Florida

Florida stands out for its straightforward tax system, offering a 5.5% corporate income tax on net income earned within the state. This aligns with Florida’s reputation as a business-friendly state.

The tax is calculated based on federal taxable income, with adjustments made at the state level. One key rule is that Florida does not permit net operating loss (NOL) carrybacks – losses can only be carried forward. These state-specific adjustments play a role in determining a company’s final tax liability.

Another advantage is Florida’s lack of a throwback rule. This means that sales of products shipped from Florida to customers in other states are excluded from in-state sales calculations. For manufacturers and distributors, this can lower the proportion of income subject to Florida’s corporate tax.

Businesses can also take advantage of several tax credits, including:

- Capital Investment Credit

- Research and Development Credit

- Rural Job Credit

These credits can help reduce the effective tax rate for eligible companies.

| Feature | Detail |

|---|---|

| Standard Corporate Tax Rate | 5.5% |

| Alternative Minimum Tax Rate | 3.3% |

| Apportionment Formula | 50% Sales, 25% Property, 25% Payroll |

| Throwback Rule | None |

| Net Operating Losses | Carryforward only; no carryback |

One notable aspect of Florida’s tax system is its treatment of LLCs and partnerships. These pass-through entities are exempt from the 5.5% corporate income tax because Florida’s constitution prohibits an income tax on individuals. This provides a considerable advantage for business owners deciding on entity structures when planning a move to the state.

Next, we’ll dive into Georgia’s corporate tax landscape to see how it stacks up against Florida’s. Stay tuned as we continue exploring corporate tax environments across different states.

10. Georgia

Georgia keeps things simple with a flat corporate income tax rate of 4.99% for the 2026 tax year. This rate applies to both domestic and foreign corporations operating within the state.

For C-corporations, there’s an additional net worth tax based on their apportioned net worth in Georgia. However, this tax is structured to ease the burden on smaller companies. Businesses with a net worth under $100,000 owe nothing, while those with a net worth exceeding $22 million are capped at an annual tax of $5,000. Meanwhile, LLCs taxed as partnerships or disregarded entities are not subject to this net worth tax.

Georgia uses a single sales factor apportionment formula. This means only sales generated within the state are used to calculate the portion of a multi-state company’s income subject to Georgia’s tax. This setup can favor companies that operate or manufacture in Georgia but generate most of their sales elsewhere.

However, there are some adjustments to keep in mind. Georgia decouples from federal bonus depreciation (IRC § 168(k)) and the Qualified Business Income deduction (IRC § 199A). Businesses must add these amounts back when calculating their Georgia taxable income, often requiring a separate depreciation schedule specifically for the state.

| Feature | Detail |

|---|---|

| Corporate Income Tax Rate | 4.99% flat |

| Net Worth Tax (C‑Corps) | $0 to $5,000 annually |

| Apportionment Formula | Single sales factor |

| Federal Bonus Depreciation | Decoupled (add-back required) |

| NOL Carryforward | Indefinite; limited to 80% of Georgia taxable income |

| PTE Entity-Level Election | Available for S‑Corps and partnerships |

For pass-through entities like S-corporations and partnerships, Georgia offers an option to pay taxes at the entity level. This allows businesses to bypass the federal SALT deduction cap. However, once this election is made, it’s irrevocable.

Georgia’s straightforward tax structure, combined with its specific adjustments, creates a unique environment for businesses. It’s a balance of simplicity and strategic considerations, offering distinct advantages for some companies while requiring careful planning for others.

11. Hawaii

Hawaii employs a graduated corporate income tax system with three brackets determined by taxable income levels. Here’s how the rates are structured for 2026:

| Taxable Income | 2026 Tax Rate |

|---|---|

| Up to $25,000 | 4.4% |

| $25,001 to $100,000 | 5.4% |

| Over $100,000 | 6.4% |

The top rate of 6.4% is moderate when compared to states with higher tax rates like New Jersey (11.5%) or Minnesota (9.8%). However, it exceeds the flat rates of neighboring states such as Arizona (4.9%) and Utah (4.5%). These rates apply to all corporations operating in Hawaii, including professional corporations and those participating in partnerships.

While corporate income tax is an important consideration, it represents a relatively small portion of overall business taxes in Hawaii. For example, in FY2021, corporate income tax revenue amounted to about $200 million, dwarfed by $1.5 billion in property tax revenue and $1.3 billion generated by the General Excise Tax (GET). The GET is particularly notable because it applies to transactions at multiple points along the supply chain, including intermediate inputs and capital expenditures. This layered taxation can significantly impact businesses and is a critical factor for companies evaluating relocation and state selection for their business.

Hawaii’s effective business tax rate (TEBTR) was 6.6% in FY2021, higher than the national average of 4.9%. Economists William H. Oakland and William A. Testa provide insight into the purpose of such taxes:

"The primary basis for general business taxation is to recover the costs of government services rendered to the business community."

For businesses structured as REITs (Real Estate Investment Trusts) or RICs (Regulated Investment Companies), there’s an additional administrative requirement: notifying Hawaii’s Department of Taxation within 15 days of starting operations. Failure to comply results in a $50 daily penalty. This requirement underscores the importance of understanding state-specific tax obligations, particularly for REIT operators, as they plan their business strategies. Hawaii’s tax framework, especially the GET and REIT-specific rules, highlights the complexity of doing business in the state.

12. Idaho

Starting in 2025, Idaho will implement a flat corporate income tax rate of 5.3%. This rate applies uniformly to both the corporate income tax and the franchise tax, meaning corporations are only responsible for one tax. According to Henry Shin, an IRS Enrolled Agent:

"The Gem State offers a highly competitive and straightforward tax environment for modern businesses, characterized by a flat corporate rate that ranks among the lowest in the Western United States."

Idaho’s corporate tax rate has steadily decreased over the years, dropping from 7.4% in 2012–2017 to 5.3% in 2025. Here’s a breakdown of the tax rate changes:

| Year | Idaho Corporate Tax Rate |

|---|---|

| 2012–2017 | 7.4% |

| 2018–2020 | 6.925% |

| 2021 | 6.5% |

| 2022 | 6.0% |

| 2023 | 5.8% |

| 2024 | 5.695% |

| 2025 | 5.3% |

In addition to the income tax, corporations must pay a $10 Permanent Building Fund (PBF) tax, and there is a minimum tax of $20 required for all corporations filing a return, even if they have no taxable income. Idaho simplifies tax calculations for multistate businesses by using a single sales factor as its default apportionment method.

Another notable advantage is that Software as a Service (SaaS) and electronically delivered software are exempt from Idaho’s 6% sales tax. Furthermore, with the passage of House Bill 559 in February 2026, businesses can fully deduct eligible research and experimentation (R&E) expenses starting in 2025. This aligns Idaho’s tax policies with federal guidelines and adds to its business-friendly reputation.

For entrepreneurs thinking about incorporating or relocating their businesses to Idaho, tools like BusinessAnywhere can simplify U.S. business registration, compliance, and ongoing maintenance services.

13. Illinois

Illinois stands out as one of the most expensive states for corporate taxes. The state uses a flat tax system, meaning all corporations, regardless of their income size, are taxed at the same rate – and that rate is notably high.

At the state level, Illinois imposes a combined corporate tax rate of 9.5%, which includes a 7% corporate income tax and a 2.5% Personal Property Replacement Tax (PPRT). The PPRT is a distinctive tax introduced to compensate local governments after personal property taxes were eliminated. It applies to the net income of both corporations and pass-through entities. Adding the federal corporate tax of 21% brings the total effective tax rate for businesses in Illinois to approximately 28.5%.

This 9.5% rate places Illinois just behind Minnesota’s 9.8%, making it one of the highest in the nation. For comparison, neighboring states like Indiana and Missouri have much lower rates, at 4.9% and 4.0%, respectively.

Illinois also has a notably low economic nexus threshold: $100,000 in sales or 200 transactions can trigger a filing requirement, even if the business has no physical presence in the state. Additionally, businesses must add back federal bonus depreciation when calculating taxable income in Illinois. Starting with tax years ending on or after December 31, 2025, the state will adopt the Finnigan method for apportioning income among unitary business groups, which could expand the tax base for corporations operating across multiple states. These factors combine to make Illinois a difficult state for businesses from a tax perspective.

"Graduated corporate rates are inequitable – that is, the size of a corporation bears no necessary relation to the income levels of the owners." – Jeffrey Kwall, Professor of Law, Loyola University Chicago School of Law

Illinois employs a single sales factor apportionment formula, which can benefit manufacturers with significant in-state operations that primarily sell out-of-state. However, this formula may work against remote sellers or digital service providers with high in-state sales but little physical presence. Any business considering a move to Illinois should carefully evaluate its nexus and tax obligations before making a decision. Implementing proactive state tax nexus planning can help mitigate these risks.

14. Indiana

Indiana has a flat corporate income tax rate of 4.9% on adjusted gross income. Combined with the federal corporate tax rate of 21%, businesses face an effective tax rate of 25.9%, which is about 3 percentage points lower than neighboring Illinois. Unlike some states, Indiana does not impose franchise or capital stock taxes, focusing solely on taxing profits. The statewide sales tax is set at 7%, with no additional local sales taxes. These factors contribute to Indiana’s reputation as a business-friendly state.

One standout feature is Indiana’s use of the single-sales factor apportionment formula. This means only sales made within the state are used to determine the taxable portion of a company’s income. For technology companies, Indiana offers a notable advantage: SaaS products accessed remotely are exempt from tax, provided no physical goods are transferred.

"Indiana’s tax system is already highly competitive nationally… [ranking] 9th overall and has the highest ranking among its geographic neighbors." – Andrey Yushkov and Katherine Loughead, Senior Policy Analysts, Tax Foundation

Indiana also supports innovation through targeted incentives for research and development (R&D). The state offers a tiered R&D credit: 15% on the first $1 million of qualifying excess expenses and 10% on amounts above that, adjusted by the company’s Indiana apportionment percentage. Additionally, Indiana has opted out of the federal TCJA Section 174 changes, allowing businesses to immediately deduct research and experimental costs instead of spreading them over five years. However, companies using third-party fulfillment centers in Indiana should be aware that storing inventory in the state may create a physical nexus, subjecting them to corporate income tax.

These policies, along with the state’s simplified tax structure, make Indiana an attractive option for businesses aiming to minimize tax burdens when they register a business in the US.

| Tax Feature | Rate/Status |

|---|---|

| Corporate Income Tax | 4.9% flat |

| Franchise/Capital Stock Tax | None |

| Statewide Sales Tax | 7.0% (no local add-ons) |

| SaaS Taxability | Generally exempt |

| Apportionment Method | Single-sales factor |

| R&D Credit (Regular) | 15% on first $1M; 10% on excess |

15. Iowa

Iowa uses a graduated corporate tax system for 2026, with rates set at 5.5% on the first $100,000 of taxable income and 7.1% on amounts exceeding that. This represents a significant drop from past higher rates. The state has plans to shift to a flat 5.5% corporate tax rate for all income levels. However, this transition depends on whether net corporate income tax receipts surpass $700 million in a fiscal year, which would automatically trigger the reduction.

For financial institutions like banks and credit unions, Iowa imposes a separate franchise tax, while other corporations adhere to the graduated tax schedule.

Tech companies operating in Iowa should note that Software-as-a-Service (SaaS) and remote software are subject to a 6% state sales tax, with many counties adding an additional 1% local tax. This can significantly impact tech businesses’ pricing and compliance strategies.

Iowa enforces an economic nexus threshold of $100,000 in gross revenue from in-state customers. Additionally, having even a single remote employee working in Iowa establishes a physical nexus, which requires businesses to register for corporate income tax. These rules are crucial for companies assessing the tax implications of operating or relocating to Iowa.

| Tax Feature | Rate/Status |

|---|---|

| Corporate Income Tax (up to $100,000) | 5.5% |

| Corporate Income Tax (over $100,000) | 7.1% |

| Flat Rate Target | 5.5% (pending revenue triggers) |

| Franchise Tax | Financial institutions only |

| State Sales Tax | 6% (up to 7% with local option) |

| SaaS Taxability | Taxable |

| Apportionment Method | Single-sales factor |

| Economic Nexus Threshold | $100,000 in gross revenue |

For calendar-year C-corporations, Iowa tax returns (IA 1120) are due April 30, and at least 90% of the tax liability must be paid by the original deadline.

Next, we’ll explore how Iowa’s tax policies stack up against its neighboring states.

16. Kansas

Kansas uses a two-tier system for corporate income taxes. All corporations are required to pay a 4% base tax on their taxable income, along with a 3% surtax applied to income exceeding $50,000. This creates a top marginal rate of 7%. For instance, a business with $200,000 in taxable income would pay 4% on the entire amount and an additional 3% on the $150,000 that exceeds the $50,000 threshold.

This setup is particularly beneficial for smaller businesses, as those with taxable income below $50,000 only face the 4% rate. By 2026, 24 states will have higher marginal corporate tax rates than Kansas, placing the state in a mid-range position nationally. Kansas’s tax policies are especially appealing to smaller, service-oriented businesses.

Kansas also stands out by not imposing a general corporate franchise tax on net worth or capital stock. Additionally, there is no gross receipts tax for standard corporations. However, financial institutions are subject to a separate Privilege Tax, leaving the corporate income tax as the primary state-level tax for most businesses, especially startups and service providers.

This perspective is echoed by experts in the field:

"For the majority of startups and service-based businesses, the corporate income tax is the primary levy you will encounter when assessing your Kansas corporate state taxes liability." – Cleer Tax

Cleer Tax highlights that the corporate income tax is the main tax burden for most startups and service companies in Kansas. The state also offers a tax credit of 95% of the income tax liability for resident individuals earning income from business activities at facilities relocated to Kansas. To take advantage of this credit, businesses must file Form K-120 by April 15.

| Tax Feature | Rate / Detail |

|---|---|

| Corporate Income Tax (Base) | 4% on all Kansas taxable income |

| Corporate Income Surtax | 3% on income over $50,000 |

| Top Marginal Rate | 7% |

| Franchise Tax | None for general corporations |

| Privilege Tax | Financial institutions only |

| State Sales Tax | 6.5% (local rates may increase totals to 8%–11%) |

| Economic Nexus Thresholds by State | $100,000 in annual gross sales |

| NOL Carryforward | 10 years |

For entrepreneurs thinking about moving their businesses to Kansas, platforms like BusinessAnywhere can simplify the process of U.S. business registration, compliance, and ongoing management.

17. Kentucky

Kentucky keeps things simple with its corporate tax structure: a flat 5% corporate income tax rate on all taxable income for C-corporations. This rate has been in effect since January 1, 2018. When combined with the federal corporate tax rate of 21%, businesses in Kentucky face a combined effective tax rate of 25%.

What makes Kentucky stand out is its Limited Liability Entity Tax (LLET). Unlike a standard franchise tax, the LLET applies to both C-corporations and pass-through entities like LLCs and S-corporations. It’s calculated based on Kentucky gross receipts or gross profits. Importantly, corporations can offset their income tax liability with a credit for the LLET paid, which helps reduce the overall tax load.

For businesses operating in multiple states, Kentucky uses a single sales factor apportionment formula. This means your tax obligation in Kentucky is determined solely by the percentage of your total receipts attributable to Kentucky customers. This method provides a straightforward way to determine tax liability, especially for businesses with operations in multiple states.

Kentucky’s 5% corporate tax rate is competitive when compared to neighboring states. It’s lower than Illinois (9.5% plus a 2.5% Personal Property Replacement Tax) and West Virginia and Tennessee (both at 6.5%), though it’s slightly higher than Indiana (4.9%) and Missouri (4.0%).

Here’s a quick breakdown of Kentucky’s key tax features:

| Tax Feature | Detail |

|---|---|

| Corporate Income Tax Rate | 5% flat |

| Alternative Business Tax | Limited Liability Entity Tax (LLET) |

| Apportionment Method | Single sales factor |

| Combined State + Federal Rate | 25% |

| Key Incentives | Kentucky Business Investment (KBI) Act Credit, LLET Credit |

For businesses considering a move to Kentucky, it’s crucial to account for the LLET separately from income tax, as it applies regardless of the entity type. If you’re navigating U.S. business entity formation or compliance, BusinessAnywhere offers remote services to simplify the process.

18. Louisiana

Starting January 1, 2025, Louisiana will implement a revamped tax structure, shifting from a tiered corporate income tax system – previously maxing out at 7.5% for income over $150,000 – to a flat 5.5% corporate income tax rate across all taxable income. This change simplifies the tax process and benefits businesses that would have been subject to higher tax brackets under the old system.

The updated system also introduces a $20,000 standard deduction for corporations and allows businesses to elect Section 179 and 100% bonus depreciation on qualified property and R&D expenses. This means companies can fully deduct these costs in the year they are incurred, providing immediate financial relief.

One of the most impactful changes is the repeal of the corporate franchise tax, effective for tax periods starting January 1, 2026. Previously, this tax required businesses to pay $2.75 per $1,000 of capital employed in the state, creating challenges for capital-heavy industries. Jeff Glickman, JD, LL.M, State & Local Tax Leader at Aprio, highlighted the significance of these reforms:

"Louisiana enacted significant tax reform, including the repeal of the corporate franchise tax, the expansion of the sales tax base to digital products and SaaS, and current deductions for research and experimentation expenses."

However, there is a trade-off. While corporate income taxes are decreasing, Louisiana is broadening its state sales tax base to include digital products, SaaS, and information services starting January 1, 2025. Additionally, the state sales tax rate will rise from 4.45% to 5.0%, a rate that will remain in effect until December 31, 2029. Businesses using digital services will need to determine if they qualify for the commercial-purpose exemption. Here’s a quick overview of the key tax changes:

| Tax Feature | Rate / Status (2025–2026) |

|---|---|

| Corporate Income Tax | 5.5% flat rate |

| Corporate Franchise Tax | Repealed as of January 1, 2026 |

| Standard Deduction | $20,000 |

| Bonus Depreciation (Qualified Property & R&D) | 100% election available |

| State Sales Tax | 5.0% (includes SaaS/digital products) |

| Apportionment Method | Single sales factor |

Louisiana also employs a single sales factor apportionment formula, which benefits companies that generate significant revenue from Louisiana customers but have most of their physical assets located elsewhere. For businesses managing compliance across multiple states, services like BusinessAnywhere simplify the process by offering remote registration and compliance tools through an online platform. These reforms align with broader national trends aimed at modernizing tax systems and creating a more business-friendly environment.

19. Maine

Maine uses a graduated corporate tax system with four brackets, ranging from 3.5% to 8.93%. Its top rate ranks as the 8th highest in the nation, which stands out in the Northeast, where the average combined rate is around 27.3%. Unlike flat-rate systems in states like Colorado or Indiana, Maine’s tiered structure creates unique considerations for businesses deciding where to operate.

| Adjusted Federal Taxable Income | Tax Rate |

|---|---|

| $0 – $350,000 | 3.5% |

| $350,001 – $1,050,000 | $12,250 + 7.93% of the excess over $350,000 |

| $1,050,001 – $3,500,000 | $67,760 + 8.33% of the excess over $1,050,000 |

| Over $3,500,000 | $271,845 + 8.93% of the excess over $3,500,000 |

This tiered system means careful tax planning is key, especially as businesses approach income thresholds.

The structure favors smaller businesses. For example, a company earning $500,000 in Maine would owe about $24,145 in taxes – calculated as $12,250 plus 7.93% of the $150,000 above $350,000. In comparison, the same income in a flat-rate state like North Carolina (2.5%) would result in a tax of roughly $12,500. As income increases, Maine’s higher rates become more noticeable, encouraging larger firms to compare its 8.93% top rate with nearby options such as New Hampshire’s 7.5% business profits tax.

Maine also has specialized tax rules. Financial institutions and insurance companies, for instance, aren’t subject to the standard corporate income tax – banks pay a franchise tax, while insurers pay a premiums tax. Additionally, the state enforces an economic nexus threshold: corporations are taxed if they exceed $500,000 in sales, $250,000 in property, or $250,000 in payroll.

One potential advantage for businesses is the Pine Tree Development Zone (PTDZ) Program, which offers tax reductions for companies in specific sectors or regions. However, businesses near the $350,000 or $1,050,000 thresholds should plan carefully, as crossing these limits triggers a significant rate increase – from 3.5% to 7.93%.

For those managing compliance across multiple states, tools like BusinessAnywhere can streamline processes, including remote business registration and regulatory requirements.

20. Maryland

Maryland’s corporate tax policies are a major factor for businesses considering relocation. Before establishing a presence, companies must secure an EIN for tax identification. The state imposes a flat 8.25% corporate income tax on apportioned net income, ranking as the 14th highest in the U.S. as of 2026. When combined with the federal corporate tax rate of 21%, businesses in Maryland face a combined effective tax rate of 27.3%.

One standout feature of Maryland’s tax system is its single-sales factor apportionment formula, which has applied to most unitary businesses since January 1, 2022. This formula calculates taxable income solely based on Maryland-sourced sales, excluding property and payroll costs. For businesses with significant operations in Maryland but most of their sales occurring out-of-state, this approach can lead to a reduced state tax liability. This setup also lays the groundwork for Maryland’s specific digital tax initiatives.

The state has introduced a dual-rate "Tech Tax" on digital services: 3.0% for B2B enterprise software and 6.0% for B2C digital products. IRS Enrolled Agent Henry Shin comments:

"Maryland provides a challenging but rewarding regulatory environment, especially with the introduction of its new ‘Tech Tax.’"

To benefit from the lower B2B rate, businesses must confirm that their software qualifies as enterprise-grade.

Maryland also enforces an economic nexus threshold of $100,000 in annual sales or 200 transactions. Additionally, businesses enrolled in the MarylandSaves retirement program enjoy a waiver of the standard $300 SDAT annual report fee. Unlike many states, Maryland prohibits local jurisdictions from imposing additional sales taxes, maintaining a consistent statewide 6% sales tax rate.

| Tax/Fee | Rate | Notes |

|---|---|---|

| Corporate Income Tax | 8.25% | Flat rate on apportioned net income |

| B2B Tech Tax | 3.0% | Applies to enterprise software for business use |

| B2C Tech Tax | 6.0% | Applies to digital products for personal use |

| Sales and Use Tax | 6.0% | Uniform statewide; no local add-ons |

| Annual Report Fee | $300 | Waived with MarylandSaves enrollment |

| Underpayment Interest | 11.48% | 2026 calendar year rate |

Regionally, Maryland’s 8.25% corporate tax rate is lower than Pennsylvania’s 8.99% and Delaware’s 8.7%, yet higher than Virginia’s 6.0% and North Carolina’s 2.5%. These comparisons highlight the need for tech-driven and multi-state businesses to carefully evaluate Maryland’s tax structure, especially its apportionment rules and Tech Tax policies.

21. Massachusetts

Massachusetts takes a different approach to business taxation by using a Corporate Excise Tax instead of a traditional corporate income tax. This tax has three parts: an income-based tax, a non-income-based tax, and a minimum excise tax.

For standard C-corporations, the income-based tax rate is 8.0% on net income. When combined with the federal corporate tax rate of 21%, the total effective tax rate reaches 27.0%, placing Massachusetts 11th highest in the nation as of 2026. The non-income component is calculated at $2.60 per $1,000 of Massachusetts tangible property or net worth, regardless of whether the business is profitable. Meanwhile, the minimum excise tax is set at $456.

The Massachusetts Department of Revenue explains:

"A security corporation is subject to an excise based on its gross income, and also to a minimum excise that applies when that measure is below a certain dollar threshold."

Starting January 1, 2025, Massachusetts adopted a single sales factor apportionment formula for all business corporations. Under this system, taxable income is determined solely by in-state sales, which can benefit companies with strong local operations. If you’re considering relocating, it’s a good idea to calculate how this formula might impact your tax liability.

For S-corporations, Massachusetts applies a tiered tax rate based on total receipts. Companies with receipts between $6 million and $9 million pay 2.0%, while those with receipts of $9 million or more pay 3.0%. However, Massachusetts requires businesses to add back federal bonus depreciation (IRC § 168(k)) when calculating state taxable income. This could be a key factor for businesses with significant investments in capital equipment.

| Entity Type | Income Rate | Non-Income Measure | Minimum Excise |

|---|---|---|---|

| C-Corporation | 8.0% | $2.60 per $1,000 | $456 |

| S-Corp (Receipts $6M–$9M) | 2.0% | $2.60 per $1,000 | $456 |

| S-Corp (Receipts $9M+) | 3.0% | $2.60 per $1,000 | $456 |

| Financial Institution | 9.0% | N/A | $456 |

| Security Corporation (Class 1) | 0.33% (gross income) | N/A | $456 |

Additionally, out-of-state businesses selling into Massachusetts may establish economic nexus if their in-state sales exceed $500,000 in a taxable year. This threshold requires careful monitoring to avoid unexpected filing obligations. Massachusetts’ unique tax structure sets it apart from many other states, making it essential for businesses to understand their obligations before expanding or relocating operations.

22. Michigan

Michigan has a flat 6.0% Corporate Income Tax (CIT), which applies to C-corporations and other federally taxed corporate entities. The state does not impose a general corporate franchise tax based on net worth or capital stock.

For small businesses, Michigan offers a Small Business Alternative Credit. This credit can reduce the effective tax rate to 1.8% of adjusted business income for qualifying companies. To be eligible, a business must meet the following criteria: gross receipts of $20 million or less, business income of $1.3 million or less, and individual officer compensation below $180,000.

S-corporations and LLCs are exempt from the CIT. Instead, their income is passed through to owners and taxed at the individual rate of 4.25%. Different rules apply to insurance companies and financial institutions. Insurers pay a 1.25% tax on gross direct premiums, while financial institutions are taxed at 0.29% on net capital.

Michigan uses a single-sales factor apportionment formula, which excludes sales to states where a company lacks a tax presence from the sales factor. This can be a significant advantage for businesses operating in multiple states, as the state does not apply throwback sales rules.

Beginning January 1, 2025, Michigan introduced an R&D Tax Credit for eligible CIT filers, with an annual cap of $100 million. Businesses aiming to claim this credit for the 2025 tax year must file a tentative claim with the Michigan Department of Treasury by April 1, 2026.

"This synergy between a streamlined tax rate and a robust innovation incentive reflects a broader state-level economic shift toward attracting knowledge-based industries while maintaining a predictable revenue environment."

| Tax Type | Rate | Applicable Entity |

|---|---|---|

| Standard Corporate Income Tax | 6.0% | C-Corporations |

| Small Business Alternative Credit | 1.8% | Eligible small businesses |

| Individual Income Tax (Flow-through) | 4.25% | S-Corporations, LLCs |

| Insurance Premiums Tax | 1.25% | Insurance companies |

| Financial Institution Tax | 0.29% | Banks and savings associations |

Michigan’s straightforward tax structure, attractive small business incentives, and new R&D credit highlight its efforts to support businesses while encouraging innovation and economic growth.

23. Minnesota

Minnesota imposes a flat 9.8% Corporate Income Tax (CIT) on all C-corporations operating within the state. By 2026, this rate will stand as the highest statutory corporate income tax rate in the U.S.. When combined with the federal rate of 21%, the total effective rate companies face is 28.7%. For context, a corporation with $10,000,000 in taxable income would owe approximately $980,000 in state taxes – over $770,000 more than in states with no corporate income tax, like Wyoming.

Minnesota’s tax burden is further shaped by its apportionment methods. The state uses a single sales factor apportionment formula, meaning a corporation’s tax liability is determined solely by the percentage of its total sales made within Minnesota. Factors like property and payroll locations are not considered. This method can benefit manufacturers with significant operations in the state, as their in-state sales may represent a smaller portion of their total revenue. In contrast, remote sellers with high Minnesota sales could face a heavier tax burden. Additionally, out-of-state corporations earning $500,000 or more annually from Minnesota sources are subject to economic nexus rules, requiring them to file taxes even without a physical presence in the state.

Another key issue is Minnesota’s nonconformity with federal bonus depreciation rules. Corporations must add back any federal bonus depreciation deductions when calculating taxable income for the state. This can increase tax liability, especially after large capital investments. These factors combine to make Minnesota a challenging environment for many businesses.

"The test the federal government uses to establish when a foreign corporation is subject to its jurisdiction to tax – which can involve establishment of an ‘effective connection’ – is different from the test Minnesota uses to establish its jurisdiction to tax which involves constitutional nexus." – Terese Mitchell, General Counsel, Minnesota Department of Revenue

It’s worth noting that flow-through entities – such as S-corporations, partnerships, and LLCs – are not subject to corporate income tax at the entity level. Instead, their income passes through to the owners, who are taxed individually. Certified 501(c) nonprofit organizations are fully exempt as well.

For C-corporations, however, Minnesota’s high tax rate, lack of alignment with federal bonus depreciation, and broad nexus rules make it one of the more tax-heavy states for businesses. These policies also reflect broader trends in how state tax structures influence business relocation decisions.

| Tax Component | Detail |

|---|---|

| Statutory Corporate Tax Rate | 9.8% (Flat) |

| Combined Rate (State + Federal) | 28.7% |

| Apportionment Formula | Single Sales Factor (100% sales) |

| Economic Nexus Threshold | $500,000 in annual gross receipts |

| Federal Bonus Depreciation Conformity | Decoupled |

Businesses considering Minnesota for relocation or expansion should weigh these tax factors carefully. Tools like BusinessAnywhere can help simplify U.S. business registration and ensure compliance with state regulations.

24. Mississippi

Mississippi is making significant changes to its corporate tax structure, with a flat 4.0% Corporate Income Tax (CIT) set to take effect in 2026. This rate applies to all taxable income over $10,000, marking a reduction from the previous 5.0% rate in 2023. The transition includes intermediate reductions to 4.7% in 2024 and 4.4% in 2025.

The state also levies a Corporate Franchise Tax, which will be $0.50 per $1,000 of capital used in Mississippi by 2026. However, the first $100,000 of capital is exempt, and there is a minimum payment requirement of $25. This tax is set to be fully repealed by January 1, 2028, a move that simplifies compliance and reduces costs for businesses with significant capital investments.

"The state is systematically moving toward a flatter income tax and a total repeal of the corporate franchise tax by 2028. For a business owner, this means less paperwork and lower overhead every year." – Henry Shin, IRS Enrolled Agent

Mississippi uses a single sales factor apportionment formula, which calculates tax liability based solely on the percentage of total sales made within the state. This system can benefit manufacturers producing goods in Mississippi but selling primarily outside the state. However, the state also enforces a throwback rule, which could increase tax liability for companies selling into states where they lack tax nexus compliance. Additionally, Mississippi taxes business inventory as tangible personal property.

These tax reforms are part of Mississippi’s strategy to attract businesses. The state ranks #6 nationally for corporate tax competitiveness in the 2026 State Tax Competitiveness Index. To further incentivize businesses, Mississippi offers a $1,000-per-employee R&D Skills Tax Credit for qualifying technical positions. This credit is available annually for up to five years and can offset up to 50% of a company’s income tax liability. Businesses must secure a "Letter of Authorization" from the Mississippi Department of Revenue to claim this credit.

| Tax Component | Detail |

|---|---|

| CIT Rate (2026) | 4.0% flat (on income over $10,000) |

| Franchise Tax Rate (2026) | $0.50 per $1,000 of capital (exempt: first $100,000) |

| Franchise Tax Repeal | January 1, 2028 |

| Apportionment Formula | Single Sales Factor |

| Economic Nexus Threshold | $250,000 in annual sales |

| R&D Skills Tax Credit | $1,000/year per qualifying employee, up to 5 years |

Mississippi’s streamlined tax policies make it an appealing option for businesses looking to relocate. With reduced tax rates, simplified compliance, and targeted incentives, the state is positioning itself as a competitive choice for companies. Next, we’ll explore how these changes stack up against policies in other states.

25. Missouri

Missouri boasts a flat 4.0% corporate income tax rate on C-corporations, which ties for the second-lowest among states with such taxes. When combined with the federal rate, businesses face a total tax rate of 25.0% – a clear advantage over neighboring states like Illinois (28.5%) and Iowa (26.1%).

This low tax rate is a key factor in Missouri’s business-friendly reputation:

"Missouri is widely recognized for having one of the most pro-business tax climates in the United States, currently ranking 12th overall in the 2026 State Tax Competitiveness Index." – Henry Shin, IRS Enrolled Agent, Cleer Tax

Missouri’s appeal is further strengthened by the elimination of its corporate franchise tax for tax years starting January 1, 2016.

The state employs a single sales factor apportionment formula, meaning businesses are taxed only on sales sourced to Missouri. This is particularly beneficial for manufacturers, as revenue from out-of-state sales is excluded from their tax base.

Tech and digital companies also find Missouri attractive. The Department of Revenue considers Software as a Service (SaaS) to be non-taxable because it does not involve tangible personal property.

| Tax Feature | Missouri Policy |

|---|---|

| Corporate Income Tax Rate | 4.0% (Flat) |

| Franchise Tax | $0 (Repealed) |

| Apportionment Formula | Single Sales Factor |

| State Sales Tax | 4.225% |

| Economic Nexus Threshold | $100,000 in cumulative gross receipts |

| SaaS Taxation | Generally non-taxable |

Missouri’s compliance requirements are straightforward. Corporations must file an Annual Registration Report with the Secretary of State to avoid administrative dissolution, even though the franchise tax has been repealed. Online filing costs $20, while paper filings are $45. Additionally, businesses with a Missouri tax liability exceeding $250 must make quarterly estimated payments.

These policies make Missouri an appealing option for businesses looking for a favorable tax environment.

26. Montana

Montana imposes a flat 6.75% corporate tax rate for C-corporations, placing it 29th in the nation. With a combined federal and state rate of 25.8%, Montana’s tax environment is more favorable than the Northeast average and significantly lower than states like Minnesota and Illinois. Beginning in 2026, this rate will drop by 0.25%, reflecting Montana’s effort to maintain a competitive tax structure.

One of the standout features of Montana’s tax policy is the absence of a state sales tax. Additionally, there are no taxes on gross receipts, inventory, or estates/inheritance, which translates to major savings for manufacturers that rely heavily on capital investments.

For corporations with gross sales of $100,000 or less – and no owned or rented real estate or tangible personal property in Montana – there’s an option to pay a 0.5% tax on gross sales instead of filing a standard return.

Montana also offers unique incentives for businesses. Research and development (R&D) firms domiciled in the state enjoy a 100% corporate income tax exemption for their first five taxable years. On top of that, all businesses benefit from a $1 million exemption on business equipment, reducing property tax burdens.

| Tax Feature | Montana Policy |

|---|---|

| Standard Corporate Income Tax Rate | 6.75% |

| Water’s Edge Election Rate | 7% |

| Alternative Gross Sales Tax | 0.5% (sales ≤ $100,000; no MT property) |

| Minimum Tax | $50 |

| R&D Firm Exemption | 100% for first 5 years |

| Business Equipment Exemption | First $1,000,000 exempt |

| State Sales Tax | None |

As of January 1, 2025, Montana adopted a single sales factor apportionment formula. This means only sales sourced within Montana are included in the tax base. This approach is particularly beneficial for manufacturers and businesses with significant property and payroll in Montana but generate substantial sales outside the state. By reducing taxable income for such companies, Montana strengthens its appeal as a destination for businesses looking to relocate or expand. Companies moving to the state must also appoint a registered agent in Montana to maintain legal compliance.

27. Nebraska

Nebraska is undergoing a major overhaul of its corporate tax system, aiming to create a simpler and more predictable structure for businesses. By the 2026 tax year, the state will implement a flat 4.55% corporate income tax rate on all taxable income, down from the 7.25% rate in 2023. This rate will drop further to 3.99% starting January 1, 2027. These changes reflect Nebraska’s push to make its tax environment more appealing to businesses.

Previously, Nebraska used a graduated tax system, where the first $100,000 of taxable income was taxed at a lower rate, and higher income was taxed at a higher rate. Starting in 2026, the state will simplify this by transitioning to a flat tax rate of 4.55%. This shift particularly benefits larger companies by making tax planning less complicated. Nebraska also uses a single sales factor apportionment, which calculates taxes based solely on in-state sales. This is especially advantageous for businesses like manufacturers and distributors with significant operations in Nebraska but customers primarily outside the state. For example, a company with a large warehouse in Nebraska but most of its sales out-of-state would only pay taxes on the revenue generated within Nebraska.

| Tax Year | Corporate Rate | Structure |

|---|---|---|

| 2024 | 5.58% / 5.84% (graduated) | Two-bracket |

| 2025 | 5.20% | Flat |

| 2026 | 4.55% | Flat |

| 2027+ | 3.99% | Flat |

Nebraska also offers several other tax provisions businesses should note:

- S-corporations and partnerships are not taxed at the entity level, as income passes through to the owners. However, businesses can opt for a Pass-Through Entity Tax (PTET) election.

- Net operating losses incurred from 2014 onward can be carried forward for up to 20 years, though carrybacks are not allowed.

- Businesses establish economic nexus in Nebraska once they exceed $100,000 in sales or 200 transactions within the state.

- For-profit corporations must file an Occupation Tax Report in even-numbered years (such as 2026) by March 1 to maintain their corporate charter.

These adjustments, coupled with the move toward a flat tax rate, position Nebraska as a more business-friendly state, particularly for companies with significant operations but limited in-state sales.

28. Nevada

Nevada stands out among U.S. states for its tax structure. It is one of only six states that do not impose a corporate income tax. The others include Ohio, South Dakota, Texas, Washington, and Wyoming, as of 2026. For businesses, this lack of a state income tax can be a significant financial benefit. For example, while a corporation in Minnesota faces a combined federal and state effective tax rate of around 28.7%, a similar business in Nevada only contends with an effective rate of about 21.0% – essentially the federal rate.

However, Nevada offsets the absence of a corporate income tax with other taxes. The state enforces a Commerce Tax, a gross receipts tax applied to businesses with Nevada-sourced gross revenue exceeding $4,000,000 in a fiscal year (July 1–June 30). The tax rates, which vary by industry, range from 0.051% to 0.331% on revenue beyond the threshold. Businesses must file Commerce Tax returns within 45 days after the end of the fiscal year.

One critical point about the Commerce Tax is that it applies to total revenue, not net profit. This means businesses must pay the tax even if they operate at a loss. Industries with high revenue but slim profit margins, such as wholesale or retail, should carefully evaluate their overall tax liabilities before assuming Nevada is the most cost-effective option.

| Tax Type | Rate | Threshold/Basis |

|---|---|---|

| Corporate Income Tax | 0% | N/A |

| Commerce Tax | 0.051% – 0.331% | Gross revenue > $4,000,000 |

| Modified Business Tax (MBT) | 1.475% | Quarterly wages > $50,000 |

| Business License Fee | Corporations: $500 / Others: $200 | Annual flat fee |

| State Sales Tax | 6.85% | Retail sales |

Nevada also imposes a Modified Business Tax (MBT) of 1.475% on wages exceeding $50,000 per quarter. However, businesses can reduce this liability by claiming a credit equal to 50% of the Commerce Tax they paid the prior year. Additionally, Nevada exempts SaaS products from sales tax, as electronically delivered software is not considered tangible personal property. While Nevada’s tax structure reflects the federal rate, additional taxes based on revenue and wages create a more nuanced picture.

For companies considering relocation to Nevada, the Governor’s Office of Economic Development (GOED) offers potential tax abatements. These abatements can lower liabilities related to sales and use tax, personal property tax, and the MBT. To qualify, businesses must meet at least two criteria, such as a minimum capital investment, creating a specific number of primary jobs, or meeting average wage requirements.

As we continue exploring state tax policies, it’s clear that each state offers its own mix of advantages and challenges for businesses. Nevada’s approach, while attractive in some respects, requires careful analysis to ensure it aligns with a company’s financial and operational goals.

FAQs

How do I know if my business has economic nexus in a state?

Economic nexus happens when your business crosses a state’s economic activity threshold – like hitting a certain sales figure or number of transactions – even if you don’t have a physical location there. These thresholds differ from state to state. For example, some states set the bar at $100,000 in sales or 200 transactions. To figure out your responsibilities, review each state’s tax laws or use their online nexus questionnaires.

What’s the difference between single sales factor and three-factor apportionment?

State corporate tax apportionment dictates how businesses operating in multiple states divide their income for tax purposes. Traditionally, the three-factor formula was used, which takes into account a company’s payroll, property, and sales within a state. However, many states have shifted to the single sales factor method, which focuses exclusively on a business’s sales within the state. This approach taxes companies based on where their customers are located, making it essential for businesses to stay on top of these evolving requirements to ensure compliance.

If a state has no corporate income tax, what other business taxes might apply?

Even if a state doesn’t have corporate income tax, businesses aren’t entirely off the hook. States like Nevada, Texas, and Washington impose gross receipts taxes, which are based on total revenue rather than profit. This can be particularly tough for companies with thin profit margins. Beyond that, businesses often deal with other financial obligations, such as:

- Property taxes

- Unemployment insurance taxes

- Excise taxes

- Business license fees

For pass-through entities, owners might also need to pay individual income taxes on the business’s earnings. Staying on top of these various taxes is essential, and services like BusinessAnywhere can help simplify compliance and streamline bookkeeping tasks.