No – your LLC does not need a business credit card by law. But if you run regular business spending through your personal card, you can blur the line between you and your LLC, potentially compromising your personal asset protection.

Here’s the short version:

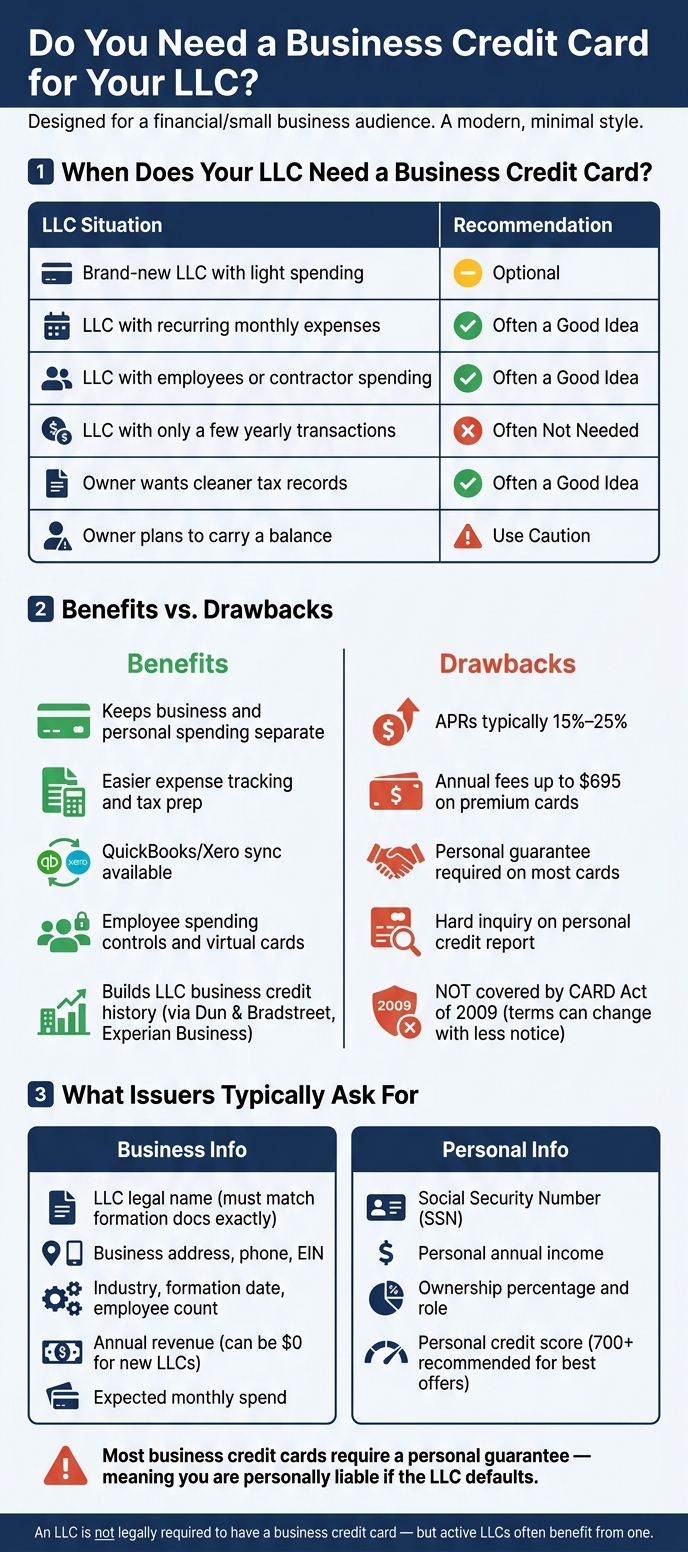

- Legally optional: No rule says an LLC must have a business credit card.

- Often worth it: A separate card helps keep business and personal spending apart.

- More useful as spending grows: If you pay subscriptions, ads, contractors, or employee costs, a business card can make recordkeeping easier.

- Less urgent for low-volume LLCs: If you only have a few expenses each year, you may be fine without one.

- Approval often leans on you: New LLCs usually need the owner’s personal credit, and many cards require a personal guarantee.

- Watch the trade-offs: APRs often run around 15% to 25%, and some annual fees can reach $695.

My takeaway: if your LLC has regular expenses, a separate business card is often the simpler setup. If spending is light and you keep clean records with a separate business checking account, you may not need one yet.

Business Credit Card for Your LLC: Do You Need One?

Quick Comparison

| Situation | Business credit card |

|---|---|

| Brand-new LLC with light spending | Optional |

| LLC with recurring monthly expenses | Often a good idea |

| LLC with employees or contractor spending | Often a good idea |

| LLC with only a few yearly transactions | Often not needed |

| Owner wants cleaner tax records | Often a good idea |

| Owner plans to carry a balance | Use caution due to APR and term changes |

The choice comes down to one thing: does a separate card make it easier for you to maintain clean books and keep your LLC separate from your personal finances?

sbb-itb-ba0a4be

What an LLC Needs to Qualify for a Business Credit Card

An LLC doesn’t need a business credit card to exist. But getting approved is a lot easier when the business and the owner’s finances are clearly documented.

Basic Application Details Issuers Usually Ask For

Issuers usually ask for the LLC’s exact legal name as it appears in your formation documents, plus the business address, phone number, EIN, industry, formation date, employee count, annual revenue, and expected monthly spend. On the personal side, they usually want the applicant’s SSN, personal annual income, ownership percentage, and role in the LLC. In most cases, the person filling out the application should be an owner or an authorized manager named in the operating agreement.

Small mismatches can slow things down. The business name and address should match your formation documents exactly. Even leaving off "LLC" can delay approval. It also helps to have your Articles of Organization and Operating Agreement ready, because some issuers may ask for them to confirm the LLC’s legal structure and standing.

For a brand-new LLC, the owner’s credit often matters more than the business’s track record.

When a New LLC May Need the Owner’s Personal Backing

With a new LLC, the card is often less about borrowing muscle and more about keeping business and personal spending separate. If the LLC is new or brings in little revenue, issuers usually put more weight on the owner’s credit and income than on the business’s history. A 700+ personal credit score is a common mark for stronger card offers.

Most business credit cards also require a personal guarantee. That means the owner is personally on the hook for repayment. And if the LLC is brand new, it’s fine to report $0 in annual revenue on the application.

Once you’re approved, the main upside isn’t just access to credit. It’s the cleaner split between personal and business purchases, easier expense tracking, and better support for day-to-day business spending.

When a Business Credit Card Makes Sense for an LLC

Keeping Personal and Business Spending Separate from Day One

Once an LLC starts spending money on a regular basis, a separate card becomes an everyday business tool, not just a legal safeguard. The main reason to get a business credit card is simple: keep business spending separate from personal spending.

A dedicated business card puts LLC expenses in one place. Common LLC startup and maintenance costs, such as state filing fees, software subscriptions, and inventory purchases, all show up on the same account. That means nothing spills onto your personal statement.

Managing Recurring Expenses and Employee Spending

If your LLC pays for recurring software, digital ads, or contractor costs, a business card helps keep those charges sorted by default. Many issuers also offer vendor-specific virtual cards. That makes it easier to see what each subscription costs and shut one off without changing your main card number.

For LLCs with employees or contractors, business cards also give you more control over spending. You can issue employee cards with spending limits and merchant category controls. Employees can upload receipt photos for faster matching and reimbursement, which cuts down on manual reimbursement requests and gives you real-time visibility into team spending.

That same separation helps even more when the business is still taking on startup costs.

Tracking Startup Costs and Building a Business Credit History

Startup costs like formation fees, a domain, software renewals, and opening inventory are much easier to track when they all sit on one card. If you connect that card to your accounting software from day one, each charge can be categorized automatically. You end up with one clean record that’s much easier to use at tax time.

There can also be a second upside. If the issuer reports account activity tied to the LLC’s EIN to business credit bureaus like Dun & Bradstreet or Experian Business, on-time payments can start building the LLC’s own credit profile. That can help later if the business applies for a loan or tries to negotiate vendor terms.

When a Business Credit Card Is Optional or Not Needed

Low-Expense LLCs That Can Stay Organized Without a Card

For a low-volume LLC, the answer is often no. Not every LLC needs a business credit card right away. In some cases, it adds more hassle than help.

An LLC with only a few transactions each year may do fine without one. That can include a holding company or a real estate LLC that pays just a small number of property bills. The same goes for a startup that’s still pre-revenue, especially when spending is light and cash flow moves up and down.

You can also pay an occasional business expense out of pocket and reimburse yourself from the LLC. That setup can work. But the paperwork still matters. Keep receipts, log every transaction, and write down the business purpose. If that trail is missing, you could lose tax deductions for LLC owners and make it harder to show the LLC is separate from you.

Even if you skip the card, keep a separate business checking account.

Drawbacks to Weigh Before Applying

The trade-off is pretty simple: cleaner separation and easier tracking versus fees, interest, and personal risk.

Business credit cards often come with APRs in the 15% to 25% range, which is higher than many personal cards. Premium options can also charge annual fees of up to $695. For an LLC with light spending, the key question is whether those costs are worth it just for better organization. On top of that, most issuers ask for a personal guarantee. So if the LLC defaults, your own assets may be on the line. A card application also usually leads to a hard inquiry on your personal credit report, which can cause a temporary drop in your score.

There’s another catch. Business credit cards are not covered by the CARD Act of 2009. That means issuers can usually change terms with less notice than they can for consumer cards. If you ever carry a balance, that detail matters.

If a card still seems like a good fit, the next step is to compare the features that make bookkeeping and spending control easier.

How a Business Credit Card Supports Bookkeeping, Compliance, and Card Selection

Cleaner Records for Taxes, Accounting, and Liability Separation

A business credit card can make day-to-day bookkeeping a lot less messy. Many cards sort charges into categories on their own, which helps keep your books up to date and makes tax prep easier.

It gets even smoother when the card connects straight to QuickBooks or Xero. In that setup, transactions move into your accounting software without manual imports. Some cards also include receipt capture tools, so you can snap a photo of a receipt and match it to the related transaction automatically. That gives you a clean paper trail for deductible purchases.

Using a card only for business spending also helps keep business and personal finances separate. That matters for accounting, taxes, and liability separation. And once you see how those tools work in practice, it becomes easier to sort through card options.

What to Compare Before Choosing a Card

After that, the next step is simple: pick a card based on how your LLC spends money.

Start by looking at recent expenses. Where does most of your spending go?

- Flat-rate cards work well if spending is spread across lots of different categories.

- Category-based cards make more sense if most spending lands in a few areas.

Rewards are only part of the picture, though. You should also check whether the card:

- syncs with your accounting software

- gives you employee spending controls

- offers virtual cards

- reports to business credit bureaus such as Dun & Bradstreet

That last point matters more than many owners think. Not every issuer reports, and that bureau reporting is what helps you build business credit for your LLC over time.

If your LLC has strong cash flow, you may also want a card that does not require a personal guarantee. That adds another layer of separation between you and the business.

Conclusion: Match the Card to Your Transaction Volume and Recordkeeping Needs

The choice mostly comes down to transaction volume, spending controls, and accounting needs. An LLC does not have to use a business credit card, but many active LLCs get a lot out of having one. If your business has only a few transactions and simple records, you can skip it. If spending happens often, a business card usually makes the work easier.

FAQs

Can I use my EIN to get a business credit card?

Yes – you should provide your EIN when applying for a business credit card because it helps build your business credit profile.

That said, most card issuers also ask for your SSN and require a personal guarantee. So even if you apply with an EIN, you’re still usually on the hook as an individual.

EIN-only applications are usually reserved for larger companies with strong revenue.

Will a business credit card protect my personal credit?

No. A business credit card does not automatically protect your personal credit, and it can even hurt it.

Most issuers require a personal guarantee. That means you’re still personally liable if the business can’t pay the bill.

On top of that, some issuers may report account activity to personal credit bureaus. If you miss payments, your personal credit score can take a hit.

What is the best time to get a business credit card for an LLC?

Usually, the best time to get a business credit card is right after you file your LLC paperwork. That gives you a clean split between personal and business money from day one. It also helps your company start building its own credit profile.

You should move it higher on your to-do list when you’re getting ready to grow, need a simple way to track employee spending, or want bookkeeping to be less of a headache.

That said, timing still matters. If your LLC is brand new and cash flow isn’t steady yet, it’s smarter to wait until you can pay the full balance each month.