If I want my LLC bank account approved fast, I need three things up front: matching business records, unexpired ID, and proof that I’m allowed to open the account.

Here’s the short version:

- I open the account in my LLC’s legal name, not my personal name.

- I keep business and personal money separate to help protect your personal assets.

- I gather my Articles of Organization, EIN letter, operating agreement, and photo ID before I apply.

- I make sure my LLC name, EIN, address, and owner details match exactly across every document.

- I pick the account based on how I use money: cash deposits, ACH, wires, fees, debit cards, and bookkeeping sync.

- I expect the bank to check owners with 25% or more ownership and at least one person who controls the company.

- I avoid delays by fixing common issues first: expired ID, P.O. Box as the main address, missing authority papers, or name mismatches.

A lot of applications get delayed over small errors, not big ones. One wrong business name, one missing ownership detail, or one old ID can stop the process.

Quick comparison

| Account type | Best for | Main tradeoff |

|---|---|---|

| Bank with branches | LLCs that handle cash often | Higher fees are common |

| Online bank | Low-fee businesses that bank online | Cash deposits may be limited |

| Fintech platform | Remote owners, e-commerce, startup-style setups | Cash support is often weak or missing |

I’d treat this as a checklist job, not a banking job. If my documents match and my account fits how the LLC gets paid, the process is usually much smoother.

sbb-itb-ba0a4be

1. What Banks Check Before Approving an LLC Account

Banks look at more than the form you fill out. Before they approve an LLC account, they check identity, business records, ownership, and risk.

That usually means verifying each signer and beneficial owner with a government-issued ID plus an SSN or ITIN, confirming the LLC’s formation through Secretary of State records, and matching the EIN with IRS records. Many banks also review ChexSystems or Early Warning Services for negative banking history.

Why Single-Member LLC Owners Still Need a Separate Account

Even if you run a single-member LLC, you still need a bank account in the LLC’s name. Banks often ask for an operating agreement or another authority document to show who has permission to sign for the business.

How KYC and Ownership Verification Affect Your Application

Banks must identify anyone who owns 25% or more of the LLC, plus at least one control person. If your LLC has more than one member, the bank may ask for documents for each qualifying owner. Some banks also require all signers to show up in person.

Banks also look at your business risk profile. That can include your industry, expected monthly transaction volume, and source of funds. Some industries draw extra scrutiny, and banks often reject businesses tied to cannabis, cryptocurrency, or firearms.

One small detail trips people up all the time: name mismatches. Your LLC name should match exactly across the application, formation documents, and EIN records.

Once you know what banks review, the next step is pulling together the documents they use to confirm each detail.

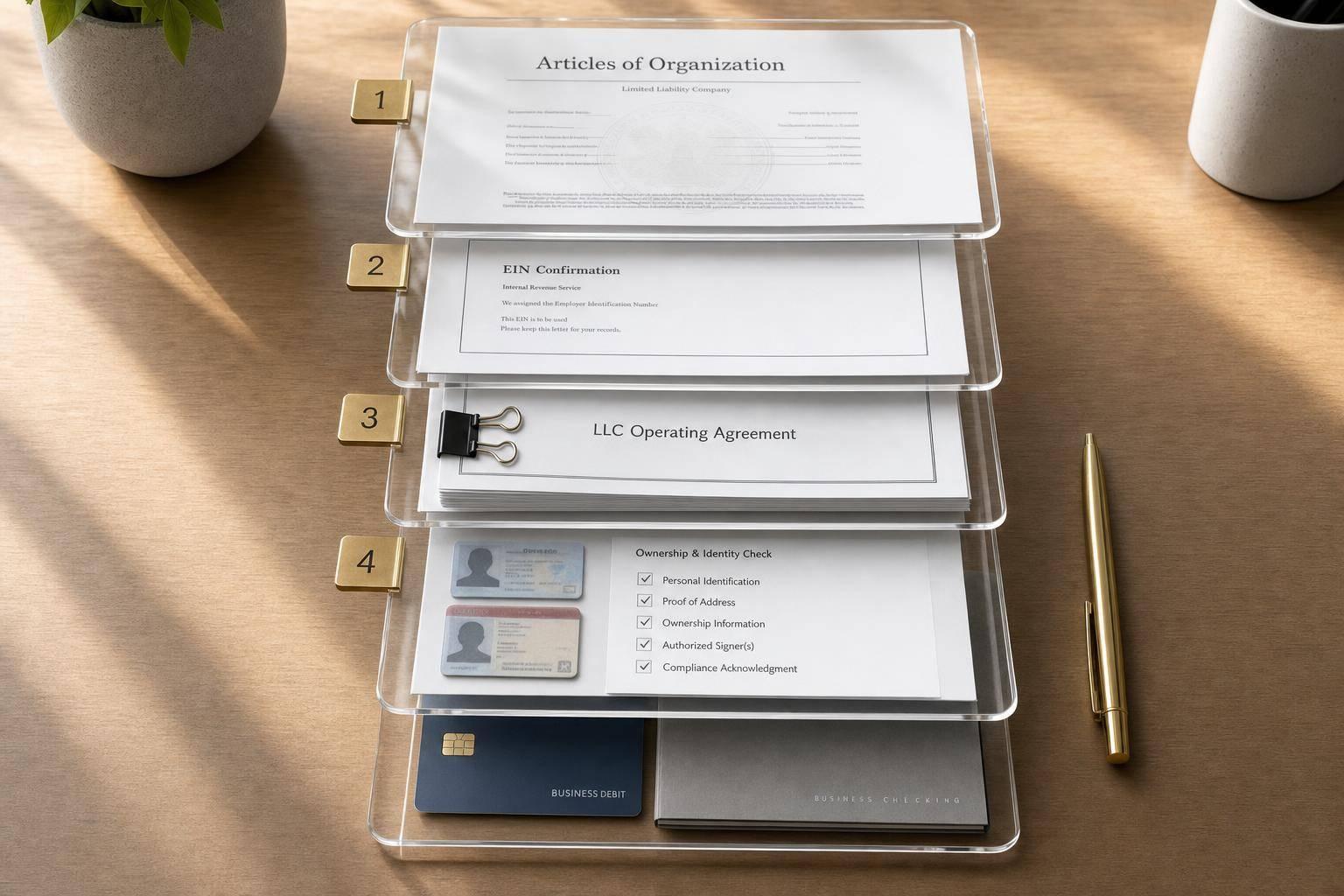

2. Documents You Need to Open a Business Bank Account for Your LLC

Gather these documents before you apply so you don’t get stuck in a back-and-forth with the bank. They use them to confirm your LLC exists, who owns it, and how it’s taxed.

Core Formation and Tax Documents

A small set of records sits at the center of most LLC bank account applications.

Your Articles of Organization – sometimes called a Certificate of Formation – proves your LLC legally exists because it’s the document your state approved and filed. Banks want the filed version, not a draft.

Your EIN confirmation letter ties your business to its federal tax ID. In most cases, that’s the IRS CP 575. If you need a replacement, banks may accept a Letter 147C.

Your operating agreement shows who owns the LLC and who can manage money in the account. Even if your state doesn’t require one, many banks still ask for it. For multi-member or manager-managed LLCs, this document should clearly name the signers and managers. If that part is vague, the bank may pause the application.

Owner ID, Address Proof, and Extra Documents Some Banks Request

Once the bank checks the LLC records, it turns to the people behind the account.

Each authorized signer needs a valid government-issued photo ID, such as:

- Driver’s license

- U.S. passport

- State ID

Expired IDs are one of the most common reasons an application gets held up.

Banks also want a verifiable physical business address. A P.O. Box by itself won’t work as the main address. If you run the business from home or use a different mailing address, bring something that proves the location, like a utility bill or lease.

Some banks may also ask for extra paperwork depending on your setup:

| Document | When You Need It |

|---|---|

| Good standing certificate | LLC active for more than one year |

| DBA certificate | LLC operates under a trade name |

| License or permit | Regulated industries such as healthcare, construction, or food service |

| Banking resolution | Multi-member LLCs formally authorizing specific signers |

| ITIN + Passport | Non-U.S. owners without an SSN |

| Certificate of Authority | LLC formed in one state but banking or doing business in another |

Once you have these documents in hand, you’re ready to pick an account and move on to the application itself.

3. Step-by-Step: How to Apply and Get Approved

Choose the Right Account Features for Your LLC

Once your LLC paperwork is ready, the next step is picking an account that fits how your business actually handles money.

Choose based on how your LLC gets paid, sends money out, and holds funds. The main things to check are monthly fees, minimum balance rules, cash deposit access, ACH transfers, wire transfers, subaccounts, debit cards, and bookkeeping integrations.

If your LLC deals with physical cash on a regular basis, you’ll want an account with branch access and cash deposit support. If you run an online business, fees tend to matter more when you send lots of transfers or process a high number of transactions. Remote and nonresident-owned LLCs often do best with accounts that have no minimum balance and allow you to open a US business bank account remotely.

Subaccounts make it easier to split money for taxes, payroll, and day-to-day operations without opening several separate accounts. On the bookkeeping side, make sure the account connects straight to QuickBooks, Xero, or FreshBooks so transactions sync on their own.

Here’s a simple way to compare options:

| Feature | What to Look For |

|---|---|

| Monthly fee | $0 or waivable with a low balance |

| Minimum deposit | $0 or low threshold |

| Cash deposits | Branch or ATM network access |

| ACH transfers | Included, no per-transfer fee |

| Wire transfers | Low or $0 domestic fee |

| Subaccounts | Multiple accounts under one login |

| Debit cards | Included with spending controls |

| Bookkeeping sync | QuickBooks, Xero, or FreshBooks integration |

Match those features against your LLC’s day-to-day transaction patterns. A single-member LLC with simple cash flow usually needs less than a multi-member LLC that runs payroll or manages several income streams.

After you pick the account type, fill out the application using the exact legal details listed in your LLC records.

Complete the Application and Respond to Follow-Up Requests

Online applications at fintech platforms usually take 15 to 30 minutes to finish. Traditional banks often take more time and may ask you to visit a branch with paper documents.

Most applications ask for:

- LLC legal name

- EIN

- Formation date

- Business address

- Industry code

- Owner details

Your LLC legal name, EIN, and formation records need to match exactly. Even a small mismatch can slow down approval.

After you submit the application, the bank may ask for ID uploads, a video selfie, or automated document checks as part of KYC compliance. Reply as soon as you can. If you wait too long, the application may be canceled.

Set Up the Account After Approval

Once you’re approved, finish the setup before you start routing business payments into the account.

Turn on 2FA and account alerts first. Then connect your accounting software – QuickBooks, Xero, or FreshBooks – and check the first few transactions to make sure dates, labels, and money flow are recorded the right way.

Next, order debit cards, set spending controls for anyone who can use the account, and use subaccounts or automatic transfers to split income into tax, payroll, and operating buckets. After that, update every payment source with the new account details.

With the account open and set up, the next step is looking at which account type makes sense for your LLC structure and how bank, online, and fintech options stack up.

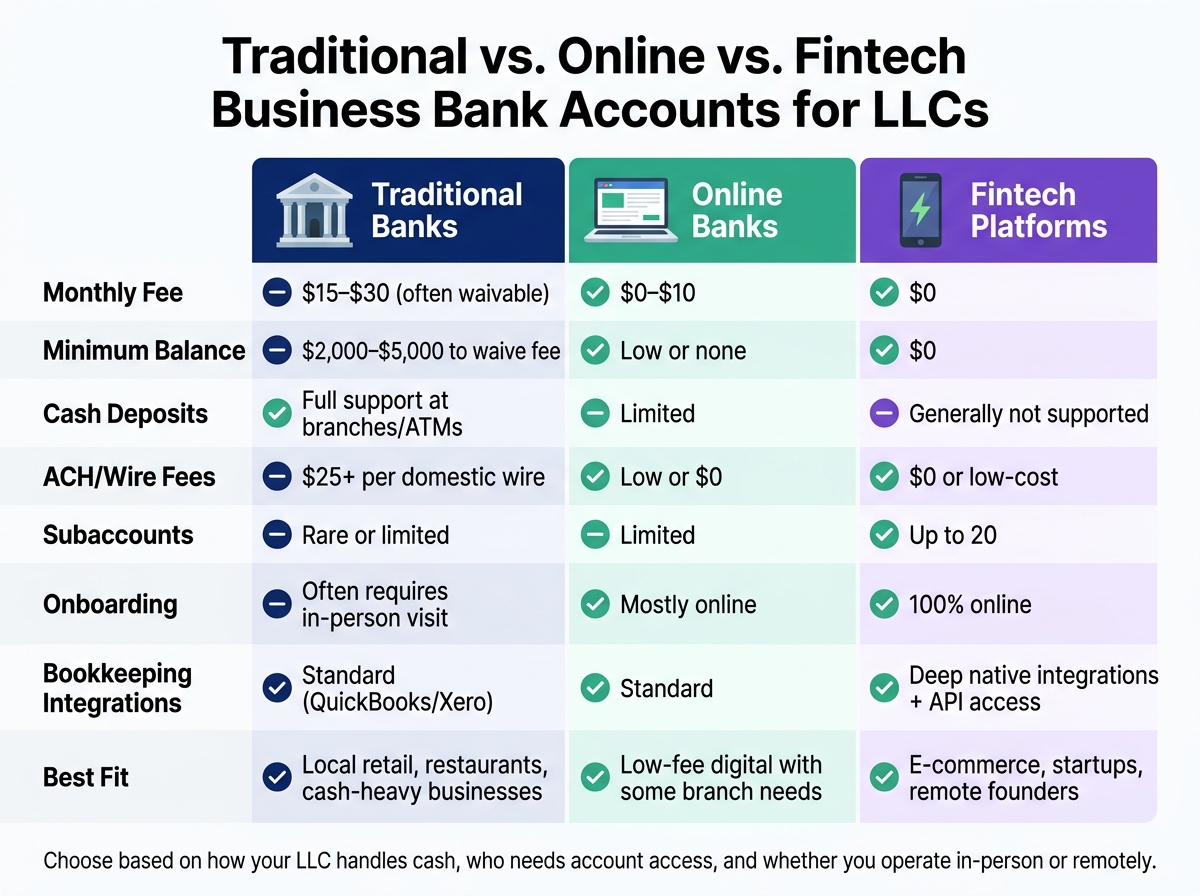

4. Compare Traditional, Online, and Fintech Business Accounts

Once your LLC is approved and your setup is done, the next step is picking the account type that matches how your business works day to day.

This choice comes down to a few simple things: how your cash moves, how your LLC is owned, and whether you run the business in person, online, or from different places.

Traditional Banks vs. Online Banks vs. Fintech Platforms

Business accounts usually fall into three groups: traditional banks, online banks, and fintech platforms.

Traditional banks give you branch access, face-to-face help, and full cash deposit support. That can matter a lot if you run a restaurant, retail shop, or any business that handles bills and coins on a regular basis. The downside is cost. Monthly fees, minimum balance rules, and wire charges tend to be higher than what you’ll see elsewhere.

Online banks keep things simple and lower-cost. They’re built for people who want to do most banking from a laptop or phone. The catch is that cash deposits can still be a pain.

Fintech platforms are geared toward digital-first owners. They often have no monthly fee, offer several subaccounts, and connect tightly with bookkeeping tools. But there’s a tradeoff here too: cash deposits usually aren’t part of the package.

| Feature | Traditional Banks | Online Banks | Fintech Platforms |

|---|---|---|---|

| Monthly fee | $15–$30 (often waivable) | $0–$10 | $0 |

| Minimum balance | $2,000–$5,000 to waive fee | Low or none | $0 |

| Cash deposits | Full support at branches/ATMs | Limited | Generally not supported |

| ACH/Wire fees | $25+ per domestic wire | Low or $0 | $0 or low-cost |

| Subaccounts | Rare or limited | Limited | Up to 20 |

| Onboarding | Often requires in-person visit | Mostly online | 100% online |

| Bookkeeping integrations | Standard (QuickBooks/Xero) | Standard | Deep native integrations + API access |

| Best fit | Local retail, restaurants, cash-heavy | Low-fee digital with some branch needs | E-commerce, startups, remote founders |

Online banks and fintech platforms often approve accounts faster than branch-based banks. For some LLCs, a split setup makes the most sense: one account for online operations, another for cash deposits. It’s not fancy, but it works.

The best fit depends on two practical questions: how many people need access, and how often you deal with cash.

Which Account Type Fits Single-Member, Multi-Member, and Remote LLCs

Your LLC structure changes what matters most in a business account.

Single-member LLC owners who run service businesses or freelance operations often do well with low-fee, online-first accounts. Built-in invoicing and bookkeeping connections can save time and cut down on manual work.

Multi-member LLCs need more control over who can do what. Look for accounts with support for multiple authorized users and role-based access. It also helps to have multiple debit cards and subaccounts, so partner distributions and shared expenses don’t turn into a mess.

Remote and nonresident LLC owners should put fully online onboarding near the top of the list. Before you apply, check that the mailing address you plan to use – such as a virtual mailbox or registered agent address – is accepted by the bank. Then make sure that address matches exactly across your Articles of Organization, EIN records, and bank application.

Next, review the approval problems that most often delay LLC applications.

5. Common Approval Problems, How to Avoid Delays, and Final Checklist

Once you’ve picked an account, the last step is simple: don’t give the bank a reason to slow you down.

Most LLC account rejections happen because of a few fixable mistakes:

- Name mismatch. Your LLC name should match exactly across your formation documents, EIN notice, and application.

- Missing or wrong ownership details. If ownership percentages are off, or the control person isn’t listed, the application can get stuck.

- Bad address or expired ID. Using a P.O. box or registered agent address as your main business address, or submitting an expired government ID, can delay review.

- Missing authority documents. Banks use the operating agreement to verify who has legal authority to open and manage the account. If you apply without one – even for a single-member LLC – the bank may pause approval.

If your LLC has had banking issues before, check your ChexSystems report before you apply. It’s a small step, but it can save you a headache. And if your LLC does business in a state other than the one where it was formed, you may need proof of foreign qualification or a Certificate of Good Standing.

Before you submit, go through this final check:

| Checklist Item | Purpose |

|---|---|

| Articles of Organization / Certificate of Formation | Proves the LLC legally exists |

| EIN Confirmation (CP 575 or Letter 147C) | Links the account to your federal tax ID |

| Signed Operating Agreement | Confirms who can open and manage the account |

| Unexpired government-issued photo ID | Satisfies identity verification |

| Proof of physical address (lease or utility bill) | Supports identity and compliance checks |

| Beneficial owner details (names, SSNs, ownership %) | Required for individuals with 25%+ equity |

| DBA/Fictitious Name Certificate (if using a trade name) | Connects your trade name to the registered LLC |

| Business License (if your industry requires one) | Required for regulated industries |

| Certificate of Good Standing (if your LLC is over one year old) | Confirms the entity is current with state filings |

Use this checklist to make sure your application is complete before you send it in. If everything lines up, submit the application.

FAQs

Can I open an LLC bank account before my EIN arrives?

Usually, no. Most banks require a valid EIN to open an LLC business bank account. They use it to confirm that your business exists and matches IRS records. If you apply without one, you’ll likely face a rejection or a delay.

There’s another catch: a new EIN can take up to two weeks to show up in IRS verification systems. So don’t rush the application. Wait until the EIN is fully processed, and keep your CP 575 or 147C confirmation letter on hand.

Do all LLC members need to be present to open the account?

Not always. Bank rules vary, so one bank may ask for more than another.

In many cases, banks want all authorized signers to complete identity verification. But that doesn’t always mean every member has to show up in person.

Your operating agreement matters too. If it says all members must approve financial decisions, the bank may ask for signed resolutions.

Banks also usually collect ID for:

- Owners with 25% or more equity

- Any designated control person

What if my LLC uses a home address or virtual mailbox?

Using a home address or virtual mailbox for your LLC is common. But it can lead to compliance or identity checks if the bank spots mismatched addresses.

If your LLC uses more than one address, the bank may pause your application and ask for more detail. In that case, have a few documents ready, such as:

- a recent utility bill

- a lease agreement

- state-filed business documents that show your official address

That way, if the bank asks for proof, you can respond without delays.