If your business trades swaps, files certain SEC forms, manages private funds, or sends cross-border payments, you may need an LEI. An LEI is a 20-character code used to identify a legal entity in the global financial system. As of 2026, more than 3.2 million LEIs have been issued, and over 300 rules around the world require or encourage them.

Here’s the short version:

- An LEI is not the same as an EIN.

- EIN: U.S. tax ID from the IRS

- LEI: global entity ID used in finance, reporting, and bank checks

- You usually need an LEI only when a trigger exists, such as:

- Each legal entity needs its own LEI. A parent company’s code does not cover subsidiaries, SPVs, or separate funds.

- LEIs must be renewed every year. If the record lapses, trades, filings, onboarding, or payments can stall.

A simple way to think about it: an EIN tells the IRS who your business is in the U.S. An LEI helps banks, regulators, and counterparties confirm your entity across borders and inside regulated markets.

If I were checking whether I need one, I’d ask just four questions:

- Do I trade regulated financial products?

- Do I file with the SEC or manage private funds?

- Do my banks or brokers ask for one?

- Do I send cross-border business payments?

If the answer to any of those is yes, I’d check the Global LEI Index before the next transaction or filing.

| Question | If “Yes” |

|---|---|

| Do I trade swaps or OTC derivatives? | You likely need an LEI |

| Do I file Form PF, N-CEN, or similar forms? | You may need an LEI |

| Do I manage private funds over $150 million? | You likely need an LEI before 10/1/2026 |

| Did a bank, broker, or custodian ask for one? | You likely need an LEI |

| Do I only run a small domestic business with no regulated finance activity? | You usually do not need one now |

That’s the core point: most small U.S. businesses do not need an LEI by default, but once they enter regulated finance or some international payment flows, the LEI can shift from optional to required fast.

What a Legal Entity Identifier (LEI) Is

An LEI is a 20-character code that identifies a legal entity in financial transactions. The code does not change if the entity moves to a different LEI issuer. Each LEI also connects to a public record in the Global LEI Index, which is managed by GLEIF. That’s what gives the LEI weight: it points to a record people can look up, not just a string of characters.

How LEI Data Identifies an Entity and Its Ownership

Every LEI record has two layers of data. Level 1 data – often described as "who is who" – includes the entity’s legal name, registered address, headquarters address, country and jurisdiction of formation, and its registration authority file number, such as a Secretary of State filing number. Level 2 data – "who owns whom" – shows the entity’s direct parent and ultimate parent.

Banks and regulators use that ownership data when they check counterparties. Put simply, they don’t just want to know who an entity is. They also want to know who sits behind it.

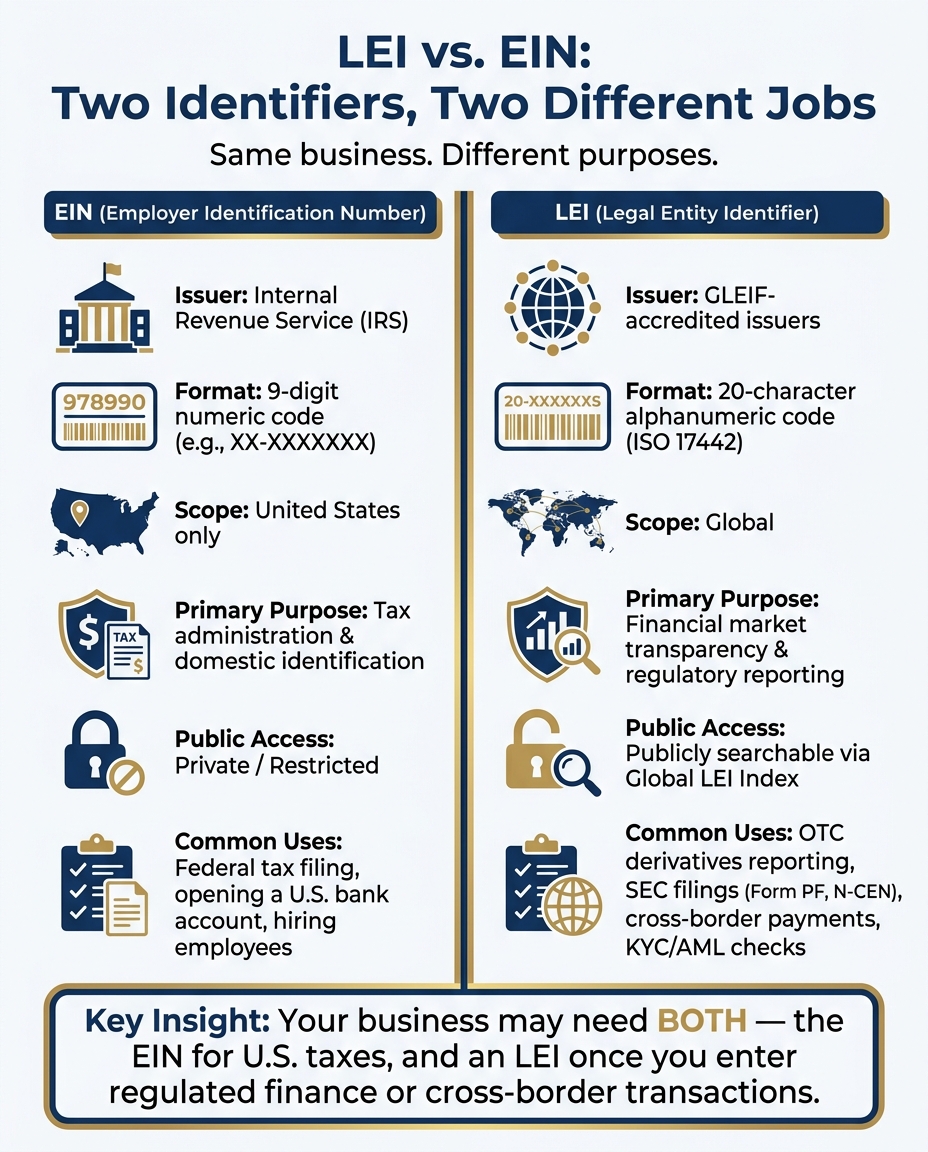

LEI vs. EIN: Two Different Identifiers for Two Different Purposes

An LEI is often mixed up with an Employer Identification Number (EIN), but they do different jobs.

An EIN is a nine-digit number issued by the IRS for U.S. tax administration and domestic identification. For example, it’s used for federal tax filing, opening a U.S. bank account, and hiring employees. An LEI, by contrast, is a 20-character global identifier used to identify legal entities across borders for financial market transparency and regulatory reporting under more than 300 regulations worldwide.

| Feature | EIN | LEI |

|---|---|---|

| Issuer | Internal Revenue Service (IRS) | GLEIF-accredited issuers |

| Format | 9-digit numeric code | 20-character alphanumeric code |

| Scope | United States only | Global (ISO 17442 standard) |

| Primary Purpose | Tax administration | Financial market transparency and regulation |

| Public Access | Private/Restricted | Publicly searchable via Global LEI Index |

This matters because banks, regulators, and trading platforms need the correct identifier for reporting and compliance. In plain English: an EIN helps identify a business for U.S. tax purposes, while an LEI helps identify a legal entity in the global financial system.

sbb-itb-ba0a4be

How LEIs Are Used in Financial and Regulatory Transactions

That registry data turns into day-to-day process work the moment a bank, regulator, or payment network needs to confirm who an entity is.

Trading, Reporting, and Compliance

LEIs show up most often in regulated financial markets. They matter when firms need to report activity, confirm a party’s identity, or screen a legal entity before moving ahead with a transaction. The CFTC requires LEIs for swap data reporting and recordkeeping, and the SEC’s Regulation SBSR applies the same rule to security-based swaps. If a firm operates in these markets, it needs an active LEI to satisfy reporting and recordkeeping rules.

The SEC applies the same kind of check in other filings too. SEC-registered investment advisers that manage private funds with more than $150 million in assets must use LEIs for both the adviser and its funds on Form PF, and the amended compliance deadline is October 1, 2026. The SEC also checks LEIs in EDGAR. Filers such as Form N-CEN submitters must enter a valid 20-character LEI or mark "N/A".

That’s why many firms follow a strict no-LEI, no-trade rule. If an LEI is missing or has lapsed, a trade or filing can stop cold. And this isn’t just box-checking. The CFTC has previously imposed six-figure fines on financial institutions for failing to keep counterparty LEI data current.

Outside securities reporting, the same identifier also appears in cross-border payments and onboarding.

Cross-Border Payments, KYC, and AML Checks

Most nonfinancial companies run into LEI requests during international wires or when opening accounts. Under FATF Recommendation 16, banks and payment service providers must include verified originator and beneficiary details in cross-border payment messages. When the parties are legal entities, banks often use the LEI to identify the sender or recipient in those messages.

LEIs also help during KYC and AML review. Because LEI records include ownership data, banks can use them to check who sits behind a company, not just the company name on the form. Level 2 data shows direct and ultimate parents, and that information is publicly searchable in the Global LEI Index.

Which Businesses Commonly Need an LEI

Not every business needs an LEI. But the group that does is bigger than many owners think.

The simplest way to judge it is this: look at the trigger, not the business label. An LLC, corporation, fund, or finance firm may need an LEI once it steps into regulated reporting, trading, custody, or cross-border payment flows.

| Entity Type | Usually needs one? | Common trigger | Who asks for it |

|---|---|---|---|

| Basic U.S. Holding LLC | Usually no | Needed only if the LLC is part of a regulated structure or a bank requests it | Banks |

| Operating LLC | Often | Brokerage, custody, or derivatives accounts; some cross-border transactions | Broker-dealers, custodians, banks |

| Publicly Listed Corporation | Often | SEC-related reporting and market compliance | SEC, institutional investors, exchanges |

| Investment Fund (Hedge/PE) | Yes | Form PF reporting; derivatives trading | SEC, CFTC, prime brokers |

| Regulated Financial Institution | Yes | Swap data reporting; other regulated market activity | Regulators, clearinghouses, global banks |

In practice, the most common LEI holders are regulated firms, funds, and entities that trade or report through financial systems.

Entity Types That Often Need an LEI: LLCs, Corporations, Funds, and Financial Firms

Banks, broker-dealers, insurers, and other regulated firms usually need an LEI for market activity and reporting. Funds, listed companies, and entities trading swaps or OTC derivatives also need one for filing and compliance.

Hedge funds, private equity funds, pension funds, and their managers need active LEIs for derivatives trading and regulatory filings like Form PF. Publicly listed corporations need LEIs for SEC-related reporting and market compliance. Non-financial companies that trade OTC derivatives or swaps must have an LEI to comply with CFTC and SEC reporting rules.

Special-purpose entities used in capital markets and structured finance also commonly require one. And one point trips people up all the time: a parent company’s LEI does not cover subsidiaries or branches.

When a Small Business or Real Estate LLC May Be Asked for an LEI

Small businesses usually run into LEI requests only when they move into regulated or cross-border finance channels.

For example, if an operating LLC wants to open a brokerage or custody account to trade stocks, bonds, or derivatives, the broker-dealer on the account will often ask for an LEI. The same thing can come up during foreign-investment onboarding. Cross-border B2B payments are another common trigger, since banks use the LEI as the main entity identifier in cross-border payment messages.

One more thing: LEIs are for legal entities, not individuals.

Next, use those triggers to test whether your business needs an LEI.

How to Decide Whether Your Business Needs an LEI

The easiest way to figure this out is to look at what your business does. An LEI isn’t something every company needs. But in certain cases, it’s not optional.

The table below covers the triggers that come up most often.

| Business Activity | Usually needed? | Who asks for it? | Typical impact without one |

|---|---|---|---|

| Trading OTC derivatives or swaps | Yes | CFTC (Dodd-Frank Act, 17 CFR Part 45) | High – trades may be rejected immediately |

| SEC filings (Form PF, 13F, N-CEN) | Yes | SEC | High – filings may be flagged or rejected in EDGAR |

| Managing a private fund with $150 million or more in assets | Yes | SEC / CFTC (Form PF, October 1, 2026 deadline) | High – non-compliance risk |

| Cross-border payments | Increasingly | Banks / FATF (Travel Rule) | Moderate – payments held during AML screening |

| Real estate syndications and loan closings | Often | Lenders / financial institutions | Moderate – delays in closing |

Use that table as a quick filter. Then check your business against the four triggers below.

A Practical Checklist for U.S. Business Owners

If even one of these applies, you likely need an LEI.

- You trade financial instruments. If your LLC or corporation trades swaps, OTC derivatives, or other regulated instruments, an LEI is required under CFTC rules. Without one, the transaction can be blocked.

- You are a regulated financial entity or fund. SEC-registered advisers managing private funds with $150 million or more in assets must have active LEIs for their firm and all advised funds before the October 1, 2026, Form PF compliance deadline.

- A provider requires one for cross-border transactions. Under the FATF Travel Rule, banks often use LEIs to identify legal entities in international wire transfers. If your business sends or receives large international payments, ask your bank whether an LEI is part of its onboarding requirements before you initiate the transfer.

- A bank, broker, custodian, or regulator has asked for one. This is the clearest signal.

If none of those fit your situation – for example, you run a domestic freelance LLC, hold a rental property, or operate a small business with no regulated financial activity – you usually do not need one right now.

How to Get and Maintain an LEI

If you need an LEI, getting one is pretty simple. You submit your entity’s legal name, state of formation, and registration number to an LEI issuer. The issuer then checks that information against official state business registries, such as your Secretary of State records, before issuing the 20-character code. If your records are clean and match exactly, most LEIs are issued within one business day, and often within minutes.

There’s one part that trips people up: the LEI belongs to the legal entity, not the owner. So if you manage several entities – like multiple real estate LLCs, a fund structure, or a holding company with subsidiaries – each one needs its own LEI.

After issuance, renew the LEI every year to keep its status Active. You should also update the record any time your business changes its legal name, registered address, or ownership structure. A lapsed LEI can block trades, delay payments, and stop onboarding.

Conclusion: When Your Business Needs an LEI and What to Do Next

If your business matched any of the triggers above, the next step is simple: check whether you already have an active LEI. If your company trades derivatives, files with the SEC, manages a private fund, or handles cross-border payments, an LEI may be required. That’s worth checking before onboarding starts or a transaction moves ahead.

Take a look at your onboarding documents early, not when the deal is already in motion. Banks and broker-dealers often bring up the LEI requirement during onboarding or right at execution. A quick check up front can save time and prevent avoidable delays.

One point trips people up: each legal entity needs its own LEI. A parent company’s code does not cover subsidiaries, SPVs, or individual funds.

If your business activity means you need one, the process is pretty simple. Register with a GLEIF-accredited issuer, make sure your legal name and ownership details stay up to date, and renew the LEI each year. Registration is usually low-cost, and annual renewal keeps the code active. Before you do anything else, check the Global LEI Index so you don’t create a duplicate record. If no active code exists, register, keep the record current, and renew yearly.

FAQs

How do I check if my business already has an LEI?

Search the Global LEI Index, the public database maintained by GLEIF. It lists all issued LEIs and gets updated daily.

Search using your company’s legal name to check whether your business appears in the database and whether the LEI status is active or lapsed.

Why does that matter? A lapsed LEI can affect financial reporting compliance.

What happens if your LEI expires before a filing or transaction?

If your Legal Entity Identifier (LEI) expires, many firms may treat it as if you don’t have one at all. Banks, trading platforms, and regulators usually need an active LEI to complete compliance checks. If it has lapsed, new transactions can get blocked.

That can also slow down filings, cause cross-border payments to fail, and expose your business to fines or other regulatory action. The fix is straightforward: renew it through the standard process with your issuer.

Can a sole proprietor or individual get an LEI?

No. An LEI is only issued to organizations and legal entities that can enter into legal contracts on their own. That includes entities like corporations, funds, and trusts.

Individuals and sole proprietors can’t get an LEI in their own name.

That said, a person acting on behalf of an eligible legal entity may be able to get a vLEI credential to verify their role.