Choosing between an LLC and a C Corporation (C-Corp) is a critical decision for startups. Here’s the key takeaway: If you’re planning to attract venture capital, issue equity, or aim for an IPO, a Delaware C-Corp is your best bet. On the other hand, if you’re running a small, profitable business without plans for institutional funding, an LLC may be a better fit due to its simplicity and tax advantages.

Key Differences:

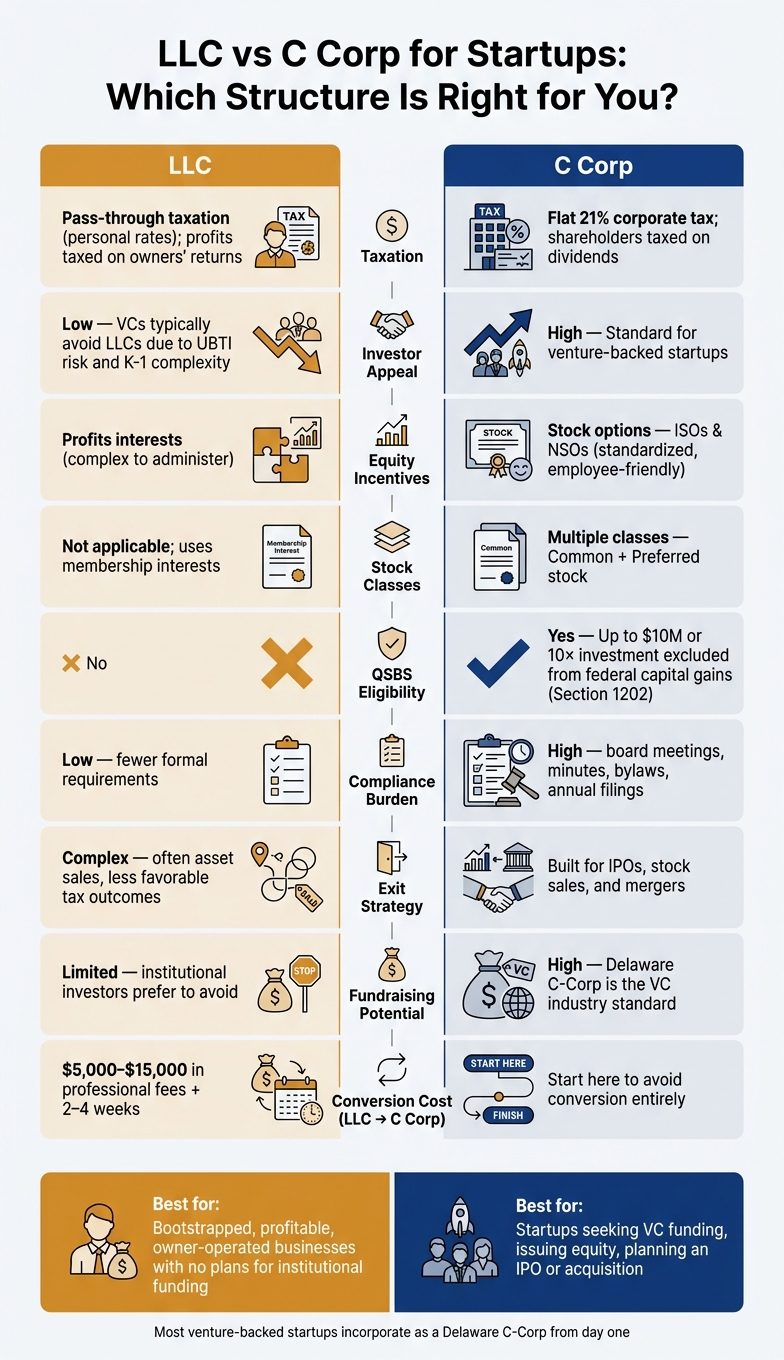

- Taxation: LLCs offer pass-through taxation, while C-Corps face double taxation but benefit from a flat corporate rate (21%) and potential tax perks like QSBS.

- Investor Appeal: C-Corps are the standard for venture-backed companies, while LLCs can create tax complications for investors.

- Equity: C-Corps provide stock options (ISOs, NSOs), while LLCs use profits interests, which are more complex.

- Compliance: LLCs have fewer formal requirements, but C-Corps offer a structure that supports scaling and investor trust.

Quick Comparison:

| Feature | LLC | C Corporation |

|---|---|---|

| Taxation | Pass-through (personal rates) | Corporate tax (21%) + dividends |

| Investor Appeal | Limited | High |

| Equity Options | Profits interests | Stock options (ISOs, NSOs) |

| Compliance | Low | High |

| QSBS Eligibility | No | Yes |

Bottom Line: Start with the end in mind. If your goal is rapid growth and attracting investors, incorporate as a Delaware C-Corp early to avoid costly conversions later. For small businesses focused on profitability, an LLC might be the right choice.

Key Differences Between LLCs and C Corporations

LLCs are often chosen for their simplicity and tax advantages, while C Corporations (C-Corps) provide a more formal structure designed to support scaling, attract external investors, and facilitate long-term growth. Let’s dive into how these differences affect taxation and investor appeal.

When it comes to taxation, the structures vary significantly. LLCs utilize pass-through taxation, meaning profits and losses are reported directly on the owners’ personal tax returns. While this setup can be appealing, it can create challenges for institutional investors. For instance, tax-exempt entities like university endowments or pension funds, which often invest in venture funds, may face Unrelated Business Taxable Income (UBTI) from LLC profits. This could jeopardize their tax-exempt status and make LLCs less attractive for these types of investors.

C-Corps, on the other hand, are taxed at a flat corporate rate of 21%. Shareholders are only taxed when they receive dividends or sell their shares. If profits are reinvested into the business, double taxation is minimized, making C-Corps appealing for growth-focused companies.

Ownership structures also differ. LLCs allow flexibility with members and customized operating agreements, while C-Corps require formal governance, including board meetings, annual filings, and clearly defined stock classes. This structure fosters trust among investors.

"Venture and institutional investors don’t want to be part of an entity that passes through profits and losses. If you’re looking to be a high-growth company that raises multiple rounds from VCs, it will be a prerequisite to incorporate as, or convert to, a C corp before accepting that capital." – Anthony Millin, Founder and Co-chair of NEXT powered by Shulman Rogers

Comparison Table: LLC vs. C Corporation

The table below highlights the key distinctions between these two structures: Feature LLC C Corporation

These differences play a critical role in aligning your business structure with your growth goals. If your startup plans to pursue venture funding, an IPO, or a strategic acquisition, a C-Corp is often the best choice. On the other hand, LLCs are ideal for businesses focused on bootstrapping or generating profits without seeking institutional funding. However, the limitations of the LLC structure can become a hurdle when external investors are involved.

sbb-itb-ba0a4be

LLCs for Startups: Pros and Cons

LLCs are a popular choice for bootstrapped startups or those with a small group of owners. They’re quicker and cheaper to establish than C-Corps and come with fewer ongoing compliance requirements. However, as a business grows or seeks outside funding, LLCs can pose challenges.

Taxation and Ownership Flexibility

One of the biggest perks of an LLC is pass-through taxation, which avoids the double taxation seen with C-Corps. On the flip side, all profits are subject to self-employment taxes. To mitigate this, some LLCs opt for S-Corp election, allowing owners to take a reasonable salary and treat additional earnings as distributions. This can save $15,000–$30,000 annually in self-employment taxes. However, S-Corp status comes with its own restrictions: it limits the entity to 100 shareholders (all of whom must be U.S. individuals) and allows only one class of stock. These restrictions can clash with venture capital requirements.

Ownership in an LLC is based on membership interests rather than traditional shares. This setup is flexible and can be tailored to the business’s needs. However, it doesn’t align well with the preferred stock model that most investors expect. For employee equity, LLCs often use profits interests, which can be more tax-efficient but require more complex tax reporting.

"The LLC structure isn’t a temporary waiting room – many successful businesses operate indefinitely as LLCs." – Adam Braverman

These points explain why startups often transition from an LLC to a C-Corp as they scale.

Fundraising Limits and Scaling Challenges

While LLCs are straightforward for daily operations, they can complicate fundraising. Many venture capitalists steer clear of LLCs due to administrative burdens. For instance, multi-member LLCs issue Schedule K-1s to each member, which can require investors to file personal tax returns in multiple states – a headache most prefer to avoid.

"Venture capital funds, tax-exempt investors and non-U.S. investors prefer investing in C-Corporations because a C-Corporation’s income is taxed at the entity level and does not flow up to the investors." – Sahir Surmeli & Ryan Urban

When institutional funding becomes a goal, converting to a Delaware C-Corp is often the only viable path. In Delaware, this statutory conversion process is relatively quick – it can typically be done in a matter of days for under $500 in state fees. However, equity restructuring and tax cleanup can add $5,000–$15,000 in professional fees and take 2–4 weeks to complete. Waiting until a term sheet is in hand can lead to delays and increased costs. Early conversion to a Delaware C-Corp not only smooths the fundraising process but also starts the clock on the QSBS holding period, which can offer significant tax benefits during an eventual exit.

C Corporations for Startups: Benefits and Trade-offs

Many founders, after grappling with the limitations of LLC structures, often find C-Corps to be a better fit for scaling and attracting investors.

For startups aiming to raise institutional capital, Delaware C-Corps are the go-to structure. They dominate the landscape, with over half of all publicly traded U.S. companies and most venture-backed startups incorporated in Delaware. Why Delaware? Its legal system is highly predictable, its corporate laws are well-established, and venture capital firms already have legal templates tailored to it. These factors make Delaware C-Corps particularly appealing for addressing fundraising and growth challenges.

"If you plan to raise venture capital, issue equity broadly, or ever want a clean acquisition process, you will usually end up as a Delaware C-Corp – either immediately or after an expensive ‘we should’ve done this earlier’ conversion." – Ryan Roberts, Startup Lawyer

Taxation and Qualified Small Business Stock (QSBS)

C-Corps are subject to a flat 21% federal corporate income tax on profits, and shareholders pay taxes again on dividends – this is the well-known "double taxation." However, most early-stage startups avoid this issue as they reinvest their revenue into R&D and operations rather than distributing dividends.

One standout tax benefit for C-Corp founders is Qualified Small Business Stock (QSBS) under Section 1202. By holding C-Corp shares for at least five years, founders may exclude up to $10 million (or 10× their initial investment) in federal capital gains. Thanks to the One Big Beautiful Bill Act, stock issued after July 4, 2025, benefits from an increased gross-assets limit for QSBS eligibility – from $50 million to $75 million. The exclusion is phased: 50% after three years, 75% after four years, and 100% after five years. This tax advantage is exclusive to C-Corps.

One critical step for founders: if you receive restricted stock, file an 83(b) election with the IRS within 30 days of issuance to secure your tax basis at the current, lower valuation.

Equity Tools and Fundraising Advantages

C-Corps offer equity mechanisms that are investor- and employee-friendly, making them a popular choice for startups.

They can issue multiple classes of stock, such as preferred stock with features like liquidation preferences and anti-dilution protection – key elements institutional investors expect. For employees, C-Corps provide Incentive Stock Options (ISOs) and Non-Qualified Stock Options (NSOs), which are more familiar and flexible compared to the profits interests often used by LLCs.

On the flip side, C-Corps require formal governance, including board meetings, recorded minutes, bylaws, and annual filings. They also can’t pass operating losses through to founders’ personal tax returns. Additionally, Delaware’s annual franchise tax starts at $175–$400, depending on the calculation method. Most early-stage startups can expect to pay around $400–$500 using the Assumed Par Value Capital Method. These governance and tax costs should be factored into your startup’s budget from the outset.

"While avoiding double taxation by filing as an LLC is attractive, it’s important to recognize that the corporate tax rate was cut from 35% to 21% in 2018, making the double tax hit not as significant as it previously was." – Anthony Millin, Founder and Co-chair, NEXT powered by Shulman Rogers

How to Choose: LLC or C Corporation for Your Startup

The choice between an LLC and a C Corporation depends on your startup’s goals and growth plans. If you’re aiming for venture capital funding, a high-value acquisition, or an IPO, a Delaware C-Corp is often the go-to structure. On the other hand, if you’re running a profitable, owner-operated business focused on distributing cash rather than pursuing a high-valuation exit, an LLC might offer better tax benefits. Let’s break down the key factors and real-world examples to help you decide.

Key Factors to Consider

There are four main factors that typically influence this decision:

- Funding goals: If you’re planning to raise venture capital, a C-Corp is usually the better choice. Venture capitalists and institutional investors prefer C-Corps because the pass-through taxation of an LLC can complicate tax reporting for their funds and limited partners. Starting with a Delaware C-Corp avoids the hassle and costs of converting later.

- Equity and talent: C-Corps provide standard stock options like ISOs and NSOs, which are easier to manage and more appealing to employees. In contrast, LLCs use profits interests, which are more complex.

- Tax preferences: LLCs allow profits and losses to flow directly to your personal tax return, which can be helpful during the early stages of your business when losses are common. Meanwhile, C-Corps keep taxes at the entity level, which is beneficial if you’re reinvesting profits into growth rather than distributing them as dividends.

- Exit strategy: If your goal is an IPO or a stock-based acquisition, a C-Corp is the standard choice. These transactions are generally cleaner and more straightforward. LLCs, on the other hand, often exit through asset sales, which may lead to less favorable tax outcomes.

- Ownership considerations for international founders: For non-U.S. residents, a C-Corp is often the cleaner option. Non-residents cannot hold shares in an S-Corp, and owning an LLC may require them to file personal U.S. tax returns – an added layer of complexity.

Common Startup Scenarios and Recommendations

Real-world examples can help clarify these considerations. Here are a few scenarios shared by Carta in February 2022:

- Sarah’s construction company: Sarah launched her business with friends-and-family funding and no plans to seek venture capital. She chose an LLC, which allowed her to use early losses to offset personal income – a smart choice for a closely held business focused on cash distributions.

- Sydney and Alex’s agtech startup: Aiming for a pre-seed VC round, they incorporated as a C-Corp from the start. This decision immediately started their QSBS (Qualified Small Business Stock) clock and kept their cap table clean, making them more attractive to investors.

- John and Nancy’s bootstrapped fintech: Although they began with personal savings, they opted for a C-Corp from the beginning. This move avoided the challenges of converting from an LLC later, which would have reset their QSBS holding period – a key factor when pitching to seed-stage investors.

Each scenario highlights how the right structure depends on your startup’s unique goals and circumstances. Understanding these factors can help you make an informed decision that aligns with your vision for growth.

Conclusion: Choosing the Right Structure for Your Startup

The business structure you choose plays a critical role in how your company raises funds, compensates employees, and plans for an eventual exit. For startups aiming for venture capital or an IPO, a Delaware C-Corp is often the go-to choice. On the other hand, if you’re running a profitable, owner-operated business without plans for institutional investment, a Delaware LLC – with its simplicity and pass-through taxation – might be a better fit. The structure you select affects taxation, investor interest, and future growth opportunities, as discussed earlier.

"Changing structures later is possible, but it is expensive, time-consuming, and sometimes tax-triggering. Smart founders decide with the end in mind."

Making changes later can reset your QSBS clock, potentially delaying significant tax advantages. Additionally, missing the 83(b) election filing deadline within 30 days can lock in higher taxes – mistakes that can be costly for growing startups.

Choosing the right structure from the outset avoids these pitfalls. Platforms like Business Anywhere simplify the process, offering a comprehensive solution that covers everything from entity formation to compliance management. They handle EIN applications, corporate bylaws, operating agreements, annual filings, and compliance alerts – all accessible from a single online dashboard. Check out their internal guides for tips on staying compliant and fine-tuning your structure as your business scales.

FAQs

When should I choose an LLC over a C-Corp for my startup?

LLCs are a great choice if you’re looking for flexibility in operations, simpler compliance requirements, and the benefit of pass-through taxation. They offer limited liability protection while allowing for customizable profit distribution among members, which can be a big plus for many small businesses.

That said, LLCs might not be the best option for startups aiming to attract venture capital or issue stock options. If your business plan includes scaling quickly, securing outside funding, or eventually selling the company or going public, a C-Corp could be the better route.

What are the biggest VC deal-breakers with LLCs?

When it comes to venture capital, LLCs face two major hurdles: tax complications and investor preferences.

First, LLCs are taxed as partnerships by default. This means members must report the company’s income on their personal tax returns – even if those profits stay within the business. This setup can create unnecessary headaches for investors who prefer simpler tax structures.

Second, LLCs don’t qualify for Qualified Small Business Stock (QSBS) benefits. These benefits are a major draw for investors, as they offer significant tax advantages when selling shares of a qualifying business.

In contrast, C-Corps are much more VC-friendly. They streamline stock issuance, make fundraising easier, and offer smoother exit options. For these reasons, C-Corps are often the go-to structure for startups seeking venture capital.

How does converting an LLC to a Delaware C-Corp affect QSBS and taxes?

Converting an LLC to a Delaware C-Corp can open the door to QSBS (Qualified Small Business Stock) benefits. This means shareholders might exclude up to 100% of their gains from federal taxes when selling stock they’ve held for more than five years. However, this change also alters the tax structure. Instead of pass-through taxation, the company will face corporate-level taxation, which could result in double taxation on profits and dividends.