If I had to give the short answer: LLC often works best at low profit, S-Corp often wins once profit is steady and higher, and C-Corp can work best when profits stay in the business or when investors are part of the plan.

Here’s the simple version:

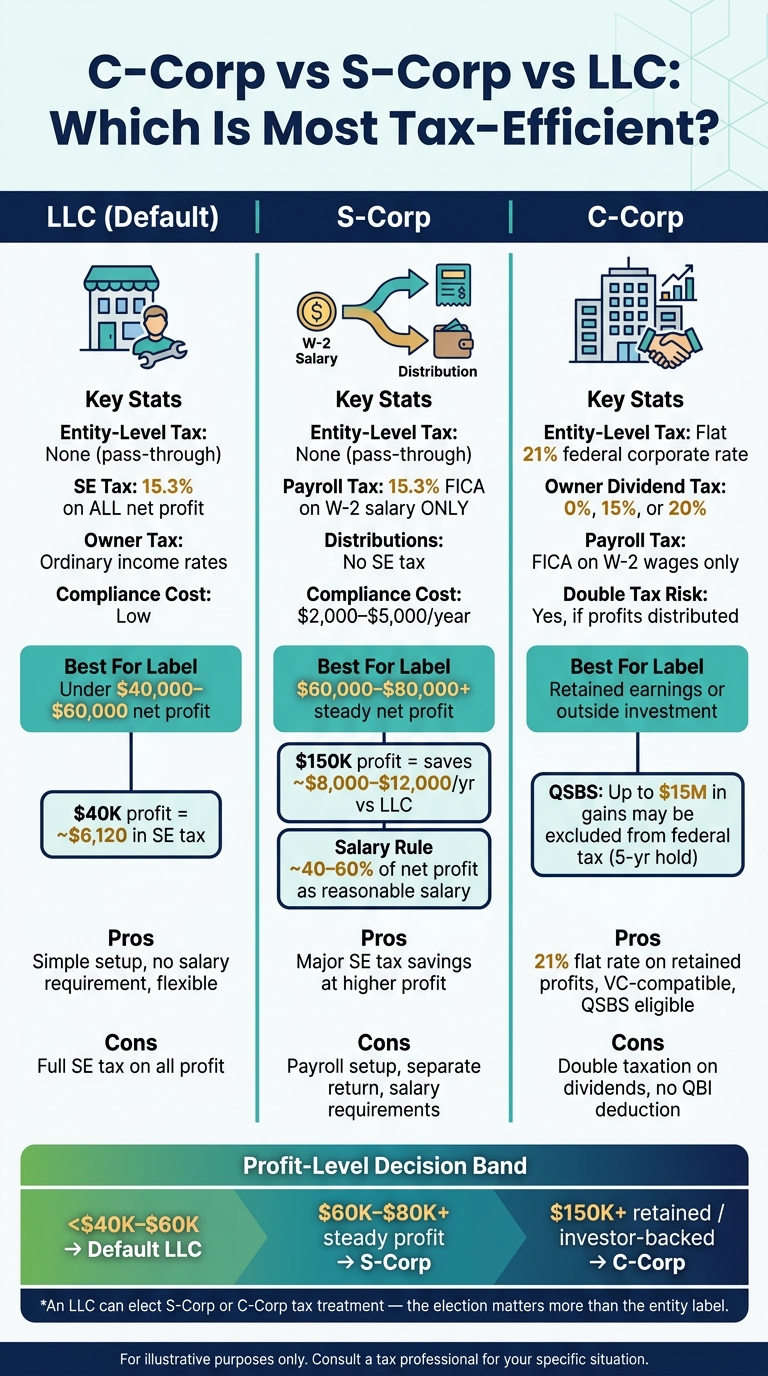

- Default LLC: easy setup, but active owners usually pay 15.3% self-employment tax on most profit

- S-Corp: can cut payroll-related tax by splitting owner pay into salary + distributions

- C-Corp: pays a flat 21% federal corporate tax, but profits paid out later can face a second tax

That means the “best” choice depends on a few things:

- how much profit you make

- how much you pay yourself

- whether you take profits out or leave them in the company

- whether you want pass-through treatment and the 20% QBI deduction

- whether you may want outside investors or QSBS treatment later

One point matters a lot: an LLC is a legal entity, not a tax status. I’d compare the S-Corp vs LLC tax benefits, not just the label. An LLC can be taxed as a sole proprietorship, partnership, S-Corp, or C-Corp.

Quick Comparison

| Type | Federal tax setup | Payroll / SE tax | Often a fit when |

|---|---|---|---|

| LLC (default) | Pass-through | 15.3% SE tax on owner profit | Profit is lower and simplicity matters |

| S-Corp | Pass-through | FICA on salary only | Profit is steady, often $60,000+ |

| C-Corp | 21% corporate tax | FICA on wages only | Profits stay in the business or investors are expected |

A few rough rules from the article:

- Under about $40,000 to $60,000 in net profit, a default LLC often comes out ahead after admin costs

- Around $60,000 to $80,000+, an S-Corp may start to save money

- At $150,000 in profit, S-Corp tax savings can land around $8,000 to $12,000 per year in many owner-operator cases

- A C-Corp can make more sense at higher profit when earnings are kept in the company, not paid out

In other words: don’t ask which entity is best in general. Ask which one leaves you with more after tax based on your profit, pay mix, and plans for the cash.

How C-Corps, S-Corps, and LLCs Are Each Taxed

With those tax rules in mind, here’s the side-by-side view:

| Entity Type | Entity-Level Tax | Owner-Level Tax | SE / Payroll Tax | Common Use Case |

|---|---|---|---|---|

| LLC (Default) | None (pass-through) | Ordinary income tax on all profits | 15.3% SE tax on net profit | Side hustles, early-stage businesses |

| S-Corp | None (pass-through) | Ordinary income tax on all profits | 15.3% FICA on W-2 salary only | Profitable owner-run businesses |

| C-Corp | 21% flat federal rate | Dividend tax (0%, 15%, or 20%) | Payroll tax on W-2 wages only | VC-backed or reinvestment-heavy startups |

C-Corp Taxation: The 21% Corporate Rate and Double Taxation Risk

A C-Corp is its own taxpayer. That means the company pays a flat 21% federal corporate tax on net profit before the owner gets paid anything.

If the owner later takes those after-tax profits as dividends, that same income gets taxed again on the shareholder’s return. That’s the double-tax issue people talk about. Dividend tax rates can be 0%, 15%, or 20%, depending on the situation.

C-Corp owner-employees also pay standard FICA payroll taxes on W-2 wages. So the big tax tradeoff is pretty simple: C-Corps tend to make more sense when profits stay inside the business, not when most of the cash gets paid out to the owner. This often matters a lot for companies that plan to retain earnings or bring in outside investors.

S-Corp Taxation: Pass-Through Income with Payroll Tax Planning

An S-Corp does not pay federal income tax at the entity level. Instead, profit passes through to the owner’s personal return and gets taxed at individual rates.

The main tax angle comes from how the owner is paid. The owner takes a reasonable W-2 salary, and any extra profit can come out as distributions. Those distributions are still taxed on the owner’s return as ordinary income, but they aren’t subject to self-employment tax. In plain English: the salary amount becomes the key tax lever.

There are also a few rules you can’t ignore. S-Corp status requires:

- U.S. shareholders only

- A single class of stock

- No more than 100 shareholders

LLC Taxation: Default Rules and Tax Election Options

By default, a single-member LLC is treated as a disregarded entity, while a multi-member LLC is taxed as a partnership. In both setups, active owners usually pay 15.3% self-employment tax on net profit, on top of ordinary income tax.

Here’s the part that trips people up: an LLC can choose to be taxed as an S-Corp or a C-Corp. So the LLC label by itself doesn’t decide the federal tax result. The tax election does.

That’s why, for tax purposes, the election often matters more than the entity name. And those gaps tend to show up more clearly at different profit levels, which the examples below walk through.

sbb-itb-ba0a4be

When Each Entity Type Usually Saves the Most Tax

The best business structure usually comes down to two things: profit and how much money you leave in the business. If you want the short version, the table below gives you the fastest read.

| Scenario | Most Tax-Efficient Entity | Reason | Payroll / SE Tax Impact | Key Tradeoff |

|---|---|---|---|---|

| Solo owner, <$40k net profit | Default LLC | Lower admin cost usually beats tax savings | SE tax still applies | No SE tax relief |

| Service business, $100k+ net profit | S-Corp | SE tax savings on owner pay | 15.3% only on W-2 salary | Higher payroll and filing costs |

| Startup retaining profits | C-Corp | Retained earnings taxed at 21% | FICA on W-2 wages only | Double taxation on future dividends |

| Startup planning outside investment or exit | C-Corp | VC investors require C-Corp; QSBS exit benefit | FICA on W-2 wages only | Must meet strict asset and active business tests |

Below is what those breakpoints usually mean in plain English.

When a Default LLC Is the Better Tax Choice

A default LLC tends to make sense when profit is low and the business is still simple to run. If annual net profit stays under about $40,000 to $60,000, the self-employment tax savings from an S-Corp often get eaten up by payroll, a separate tax return, and extra bookkeeping. Those added compliance costs often land around $2,000 to $5,000 per year.

This is why a default LLC often works well for early-stage businesses and side hustles. You don’t have to lock yourself into a set owner salary when cash flow jumps around, and that can take some pressure off when revenue is uneven.

Once profit gets past that range, it’s worth taking a harder look at the S-Corp election.

When an S-Corp Usually Saves the Most Tax

When net profit gets into the $60,000 to $80,000 per year range on a steady basis, the S-Corp election often starts to make more sense. The main tax win comes from moving part of the owner’s income out of self-employment tax.

At $150,000 in net profit, an S-Corp election can save about $8,000 to $12,000 per year. That’s the part that gets people’s attention.

The catch is reasonable salary. For service businesses, many tax pros use a range of about 40% to 60% of net profit. That number can’t be picked out of thin air. It needs support from industry wage data, so if the IRS looks at it, you have a solid case.

If the plan is to keep profits in the company or bring in outside investors, the math can shift again.

When a C-Corp Can Be More Tax-Efficient Despite Double Taxation

A C-Corp usually works best when the business keeps its profits instead of distributing most of them each year. A company that’s reinvesting for growth can build capital at the 21% corporate tax rate instead of passing income through to an owner who may face a higher individual rate.

Two other situations can also push a business toward a C-Corp.

- Venture capital investors often want a C-Corp structure. Things like preferred stock, more than one class of shares, and foreign or institutional shareholders don’t fit with S-Corp rules.

- IRC §1202 QSBS can create a major exit-planning tax break for stock that qualifies and is held for at least five years.

If most of the profit is paid out every year, though, the C-Corp usually loses that tax edge.

The next examples show what those breakpoints can look like in practice.

Side-by-Side Tax Examples for Common Owner Scenarios

These three examples show how the tax result shifts as profit changes and the owner takes money out in different ways.

| Scenario | Assumed Profit | Owner Compensation Method | Main Tax Driver | Likely Winner |

|---|---|---|---|---|

| Solo owner, modest profit | $40,000 | Owner takes profit distributions (LLC) | 15.3% self-employment tax on all profit | Default LLC (simplicity, low overhead) |

| Solo/small team, strong recurring profit | $150,000 | $70,000 salary + $80,000 distribution (S-Corp) | Payroll tax on salary only | S-Corp (saves about $10,000 to $12,000 per year) |

| Startup reinvesting or raising capital | $500,000 | Salary + retained earnings (C-Corp) | 21% corporate tax; double tax on dividends | C-Corp (lower rate on retained growth capital) |

Example 1: Solo Owner with Modest Annual Profit

Picture a freelance graphic designer earning $40,000 in net profit for the year. As a default single-member LLC, the full $40,000 gets hit with the 15.3% self-employment tax. That comes out to about $6,120.

At this level, an S-Corp often doesn’t do much for the owner after you factor in payroll, filings, and other admin costs. In plain English, the tax savings usually aren’t big enough to justify the extra work. So the default LLC comes out ahead here because the lower overhead matters more than the tax angle. As profit moves past this range, the S-Corp starts to look better.

Example 2: Solo Owner or Small Team with Strong Recurring Profit

Now take a similar service business earning $150,000 in net profit. This is the range where an S-Corp often starts to shine.

With an S-Corp election, the owner might pay themselves a W-2 salary of about $70,000 and take the other $80,000 as a distribution. Payroll taxes apply only to the salary. That means the distribution portion avoids self-employment tax, which can save about $10,000 to $12,000 per year compared with a default LLC.

That’s a big enough gap to clear the annual compliance cost by a wide margin. For many solo owners and small teams, this is the point where the math changes in a noticeable way. But the picture shifts again when the owner isn’t trying to pull most of the profit out of the business.

Example 3: Startup Reinvesting Profits or Planning Outside Investment

Things look different when the company plans to keep earnings inside the business. Say a SaaS startup brings in $500,000 in annual profit and the founders want to put most of it back into growth. In that setup, a C-Corp can keep those profits at the flat 21% corporate tax rate, which leaves more cash in the company for reinvestment.

The second tax layer becomes an issue only if the company later pays dividends. If the plan is to keep building, hiring, or funding product work, that timing matters. There’s also another piece founders often care about: QSBS. A C-Corp can make QSBS treatment possible, which may exclude up to $15 million in gains from federal tax if the stock is held for at least five years.

Conclusion: Which Entity Is Most Tax-Efficient for Your Business

The examples lead to a simple rule: lower profit often fits a default LLC, steady higher profit often fits an S-Corp, and retained earnings or outside investment can tilt the math toward a C-Corp.

Federal tax is the place to start. But it’s not the whole story. Operating in multiple states can change the answer, and in some cases, state taxes can outweigh the federal result.

From there, the next big factor is what the business does with its profit. Will it distribute the money, or put it back into the company? That matters a lot. LLCs and S-Corps may qualify for the 20% QBI deduction, while C-Corps do not.

Once you’ve sorted out the tax side, the filing choice usually gets much easier. If you’re weighing your options, look closely at your profit, salary, and state tax exposure before you file.

FAQs

How do I know if my salary is reasonable in an S-Corp?

The IRS bases reasonable compensation on what you’d pay someone else to do the same job.

That means they look at factors like:

- Industry pay norms

- Your location

- Hours worked

- Day-to-day duties

- How much your role affects revenue

For many service-based business owners, a reasonable salary often lands around 40% to 60% of net profit.

Set it too low just to cut payroll taxes, and you could run into an audit, back taxes, interest, and penalties.

How do state taxes affect whether an LLC, S-Corp, or C-Corp saves more?

State taxes can change which entity saves you the most money.

In high-tax states like California, New York, and New Jersey, PTET can help S-Corps and partnerships blunt the impact of the federal SALT deduction cap.

States can also add franchise taxes or entity-level fees. For example, California charges LLCs an $800 minimum franchise tax. That extra cost can eat into some of the federal tax savings.

Can an LLC switch to S-Corp or C-Corp taxation later?

Yes. An LLC can change its tax classification as the business changes.

To choose S-Corp taxation, file Form 2553 with the IRS. If you file within the first 75 days of the tax year, the election can apply to that entire year.

To choose C-Corp taxation, file Form 8832 or convert the LLC to a corporation under state law.

Because the tax impact can last for years, it’s smart to talk with a tax professional first.