Forming an LLC is only the first step. If I want to run a construction company the right way, I still need to handle state licensing, local registration, tax accounts, insurance, bonds, contracts, and clean bookkeeping.

Here’s the short version:

- set up the LLC by choosing a name, filing Articles of Organization, naming a registered agent, getting an EIN, and opening a business bank account.

- I still need a contractor license before taking paid jobs in most states.

- I may also need local licenses, building permits, sales tax registration, payroll tax accounts, and surety bonds.

- The LLC can help protect my personal assets, but that protection gets weak if I mix personal and business money, sign in my own name, or skip filings.

- Insurance does a different job than the LLC. The LLC separates me from the business. Insurance helps pay claims.

- Construction owners can still face personal risk for personal guarantees, unpaid payroll taxes, bond claims, and their own negligence.

A few numbers stand out:

- State LLC filing fees often run from $50 to $500

- Permit costs may be around 0.5% to 2% of project value

- Federal performance and payment bonds are often required on jobs over $150,000

- California LLC contractors may need a $25,000 license bond plus a $100,000 employee/worker bond

If I had to boil it down to one point, it’s this: an LLC helps, but it does not replace licenses, insurance, or clean records.

That’s the core of this article.

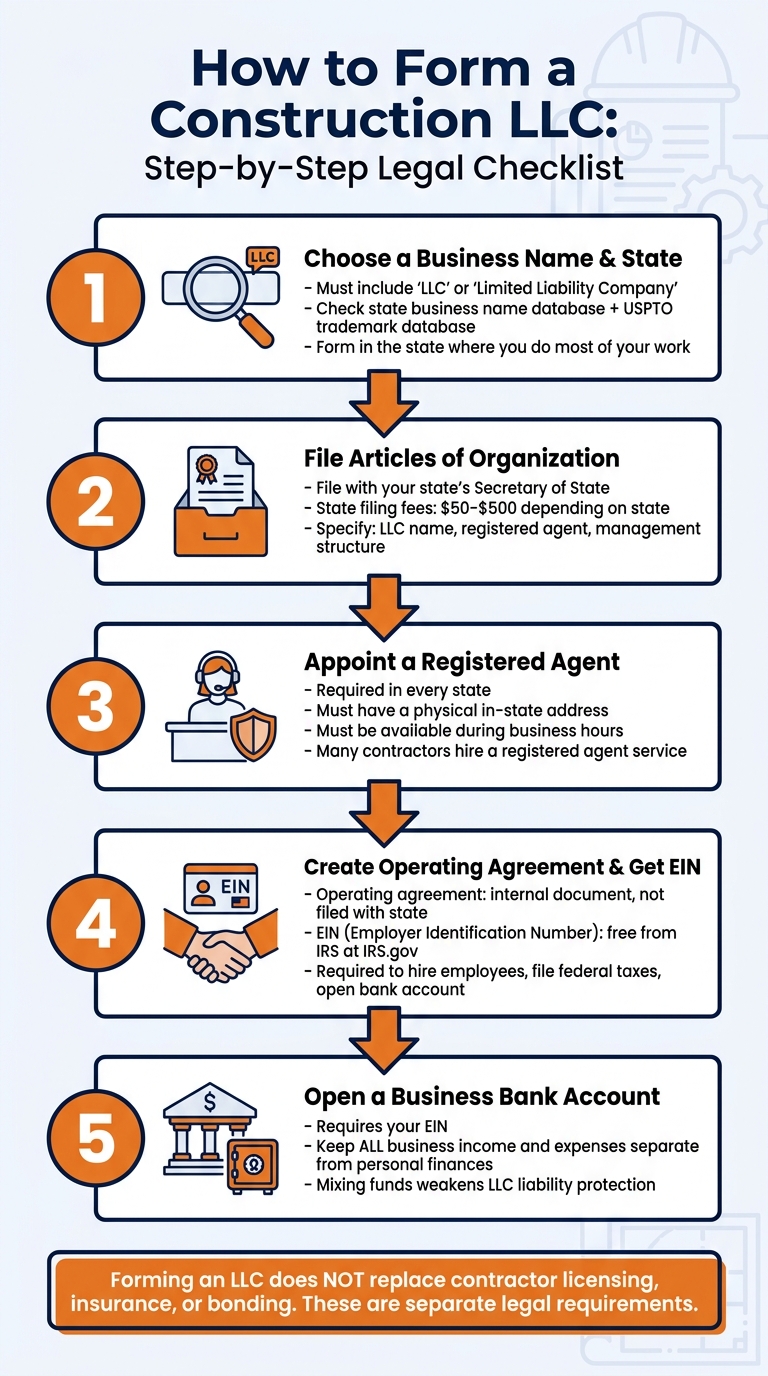

1. Forming a Construction LLC Step by Step

Choose a business name and state of formation

Pick a name that no one else in your state is using, and make sure it includes "LLC" or "Limited Liability Company." Before you settle on it, run it through your state’s business name search tool. Then do one more check in the USPTO trademark database. That second step matters. A name can pass the state search and still run into a federal trademark problem.

You should usually form the LLC in the state where you do most of your work. If you set it up in one state but do business in another, you’ll need to register there as a foreign LLC.

File Articles of Organization and appoint a registered agent

Your LLC officially starts when you file the Articles of Organization with your state’s Secretary of State office. The form usually asks for:

- Your LLC name

- Your registered agent’s name and address

- Whether the LLC is member-managed or manager-managed

State filing fees usually fall between $50 and $500, depending on the state.

You’ll also need a registered agent. Every state requires one. This person or service must have a physical in-state address and be available during business hours to accept lawsuits and government mail. A lot of contractors hire a registered agent service for a simple reason: they’re often out on job sites and don’t want to miss an important notice.

Create an operating agreement, get an EIN, and open a business bank account

Once the state approves your LLC, put together an operating agreement. You don’t file this with the state. It’s an internal document that spells out ownership and how decisions get made. If your construction LLC has more than one owner, this can save a lot of trouble later by setting the ground rules early.

Next, get an EIN – your Employer Identification Number – from the IRS. It’s free. You’ll need it to hire employees, file federal taxes, and open a business bank account. The IRS lets you apply online at IRS.gov.

Then open a business bank account as soon as you have that EIN. This is a big one. If you mix personal and business money, you can weaken the LLC’s liability shield and give creditors a path to your personal assets. Keep all income and all business spending inside the company account.

Once the LLC is set up and your finances are separate, the next move is licensing, permits, and bond registration.

2. Licenses, Permits, Tax Registration, and Bonds

Forming an LLC and getting licensed as a contractor are two separate things. Setting up the LLC does not give you permission to start taking paid jobs. Before you begin work, you need the right licenses, permits, and tax registrations in place.

State contractor licenses and specialty trade licenses

Most states require a contractor license once a job goes over a state-set dollar limit, often $500 to $1,000. A General Contractor (GC) license lets you run full projects and hire subcontractors across several trades. A specialty trade license – like electrical, plumbing, or HVAC – limits your work to that trade.

In many states, getting licensed also means showing 2 to 4 years of field or supervisory experience and passing a trade exam.

There’s another detail that can catch people off guard: many states require one qualified person to hold the license for the LLC. If that person leaves the company, the license can be suspended until someone else qualifies.

Local business licenses, building permits, and tax accounts

A state contractor license usually doesn’t cover local rules. Cities and counties often want their own business tax receipt or occupational license, and those are often renewed each year, even if you already have a state license.

Building permits work differently. They’re tied to each project, not your company as a whole. You need to get a permit from the local building department before work starts on jobs that involve structural, electrical, plumbing, or HVAC work. Permit costs often fall around 0.5% to 2% of the total project value.

Your construction LLC will often need state tax registrations too. For example:

- If you buy materials, your state may require a sales and use tax account

- If you hire employees, you’ll need a payroll tax account with your state’s Department of Revenue

Sales tax for construction can get messy fast because the rules change a lot from state to state. That’s why it’s smart to check with a CPA before you start sending invoices.

License bonds, performance bonds, and payment bonds

On bigger jobs, bonding starts to matter. And no – bonding is not the same as insurance.

Insurance pays claims on your behalf. A bond works more like a three-party guarantee that protects the client or the state. If the surety pays a claim, you pay it back.

| Bond Type | Who Requires It | When It Applies | Main Purpose |

|---|---|---|---|

| License Bond | State Licensing Board | Condition of getting or keeping a license | Protects the public against licensing law violations |

| Bid Bond | Project Owner | Submitted with a project bid | Guarantees you’ll sign the contract if you win |

| Performance Bond | Project Owner / Lender | After contract award, before work starts | Guarantees the project is completed per contract specs |

| Payment Bond | Project Owner | Required alongside performance bonds | Guarantees subcontractors and suppliers get paid |

| LLC Employee/Worker Bond | State (for example, California) | Specific to LLC-structured contractors | Guarantees payment of employee wages |

A license bond is often a standing requirement. You need it to get licensed, and you need it to keep that license active.

California stands out here. LLC contractors in the state must carry both a standard $25,000 license bond and a separate $100,000 Employee/Worker Bond that guarantees wages. That extra bond does not apply to sole proprietors.

Performance bonds and payment bonds usually show up on public works projects and larger private jobs. Under the Miller Act, federal law requires both on federal construction contracts over $150,000. Many states also have their own Little Miller Acts, and those can kick in at much lower amounts – sometimes as low as $1,000 to $25,000. In practice, performance and payment bonds are often packaged together.

Once your licenses, permits, tax accounts, and bonds are set up, the next piece is how LLC liability protection works in construction.

3. How LLC Liability Protection Works in Construction

What the LLC protects and why separation matters

An LLC usually protects your personal assets from business claims, including contract disputes, jobsite injuries, bond claims, and tax issues, if the company is kept separate and maintained the right way. That separation is a big deal. Courts look at the basics: separate contracts, separate records, and separate tax filings.

Put simply, the LLC needs to act like its own business. If it does, the liability shield is much more likely to hold.

When owners can still face personal liability

In construction, personal risk often comes from guarantees, taxes, and safety violations – not only from the work on the jobsite. Here’s where owners can still get pulled in personally: Scenario Business Liability Personal Liability Risk Reason

The pattern here is pretty simple: when the LLC is the one doing business, the LLC usually takes the hit. But when the owner signs a personal promise, fails to handle payroll taxes, or directly causes harm, that shield can crack fast.

How owners accidentally weaken the liability shield

A lot of owners weaken the shield without meaning to. Commingling funds – like paying personal bills from the business account or depositing client checks into a personal account – can give courts a reason to pierce the LLC veil. That’s one of the easiest ways to blur the line between you and the company.

Other mistakes can hurt too. An underfunded business may look like a shell, and signing contracts in your own name instead of the LLC’s name can pull you into the deal personally. Keeping licenses current also matters. If the paperwork is sloppy, the protection can get shaky.

The LLC protects the business entity. Insurance, contracts, and annual filings help cover the weak spots.

sbb-itb-ba0a4be

4. Insurance, Contracts, and Ongoing Compliance

Core insurance policies construction LLCs typically need

An LLC helps protect your personal assets. Insurance is what pays the claim. Put simply, the LLC is the legal shell, and insurance is what gives that shell muscle.

| Coverage | What It Protects | Commonly Required | Typical Use Case |

|---|---|---|---|

| General Liability (CGL) | Bodily injury, property damage, and completed operations | State licensing boards and most clients | A visitor trips on a job site or a pipe bursts after a remodel is finished |

| Workers’ Compensation | Employee medical costs and lost wages for work-related injuries | State law – mandatory once you hire one employee | A crew member falls from a ladder or suffers a repetitive motion injury |

| Commercial Auto | Business vehicles and trailers; liability and physical damage | State law and insurance carriers | A work van is in an accident while hauling tools between job sites |

| Builder’s Risk | The structure under construction against fire, theft, and weather | Lenders and project owners | A house under construction is damaged by a fire before the final inspection |

| Umbrella / Excess Liability | Claims exceeding primary policy limits | Commercial and government contracts | A catastrophic accident exceeds the $1 million limit of a standard GL policy |

| Professional Liability (E&O) | Design errors and professional negligence | Only for design-build or design-adjacent work | A contractor provides structural specs that later fail due to a calculation error |

For budgeting, small crews often pay $2,000–$8,000 per year for general liability and $5,000–$20,000+ per $100,000 in payroll for workers’ comp. Commercial auto usually costs $1,500–$5,000 per vehicle each year. Those policies matter, but they aren’t enough on their own. The paperwork tied to each job needs to be just as solid.

Contracts, documentation, and annual state maintenance

That’s why written contracts and clean subcontractor records matter so much. In construction, handshake deals can turn into expensive fights. Every project should have a written contract. Every change in scope should have a written change order.

Before a subcontractor starts work, check their license status and collect a Certificate of Insurance (COI) that lists your LLC as an additional insured. If a subcontractor has no coverage and causes a loss, your policy may end up taking the hit.

Then there’s the back-office side of staying in good standing. Most states require annual or biennial reports filed with the Secretary of State, and fees usually range from $50 to $500, depending on the state. Contractor licenses renew on a set timeline, often every one to two years. Many states also require continuing education tied to safety, ethics, or building code updates. Let a license lapse, and you could get hit with a stop-work order right in the middle of a project.

Federal filings matter too. Most construction LLCs must handle Beneficial Ownership Information (BOI) reporting through FinCEN. If your LLC has employees, payroll tax filings are a recurring federal duty. And unpaid payroll taxes can create direct personal liability for the owner. The simplest move is to track license, insurance, bond, and annual report deadlines in one calendar.

Using BusinessAnywhere to manage formation and compliance remotely

BusinessAnywhere can keep formation documents, registered agent service, EIN filing, annual reports, and mail handling in one dashboard.

Conclusion: The Minimum Legal Foundation for a Construction LLC

Once the LLC is in place, the rest of the launch comes down to a few legal basics: licensing, tax registration, insurance, and clean recordkeeping. That usually means state contractor licensing, local business registrations, any trade-specific credentials, plus the bond and insurance coverage your work requires.

An LLC can protect personal assets only if the business stays separate and compliant. That’s where the LLC earns its keep. Keep business and personal finances separate, sign contracts in the LLC’s name, maintain active licenses, and file required reports on time. Those simple habits are the minimum legal foundation for running the business properly and keeping the liability shield in place.

Form the LLC, secure the licenses, keep records clean, and maintain coverage.

FAQs

Can I start a construction business with just an LLC?

Yes, you can start a construction business as an LLC. That setup can help protect your personal assets if the business takes on debt or faces legal claims.

That said, forming an LLC alone doesn’t mean you’re ready to operate. In most cases, you’ll also need contractor licenses, permits, insurance, and sometimes bonding, depending on your state and local rules.

What licenses does a construction LLC usually need?

A construction LLC usually needs more than one license. There isn’t a single federal contractor license that covers everything.

In most states, you’ll need a state contractor’s license. That license often depends on a qualifying individual’s work history, exam results, and a background check.

You may also need:

- a general contractor or specialty trade license

- a local business license or contractor registration

- a surety bond, often $10,000 to $25,000

When am I still personally liable?

An LLC can help shield your personal assets, but that shield has limits. It’s not a free pass.

For example, you can still end up personally liable if you mix personal and business funds. When that happens, a court may decide to pierce the corporate veil.

Personal liability can also come into play in a few other cases:

- You mismanage customer deposits or retainage under state trust-fund laws

- You fail to keep required professional licenses in place

- You don’t handle warranty obligations the right way after the LLC is dissolved

That’s the part many owners miss: the LLC helps, but only if you treat the business like a separate business.