State tax nexus is a critical issue for remote businesses, especially as remote work becomes more common. Nexus is the legal connection between a business and a state, which requires tax registration, collection, and filing. Here’s what you need to know:

- Nexus Triggers: Hiring even one remote employee in a state, storing inventory, or meeting economic thresholds (e.g., meeting economic thresholds (e.g., $100,000 in sales or 200 transactions)00,000 in sales or 200 transactions) can establish nexus.

- Compliance Risks: Ignoring nexus obligations can lead to penalties, back taxes, and interest. Some states, like Nevada, can pursue up to eight years of back taxes.

- Steps to Manage Nexus:

- Map employee locations and business activities.

- Register and file taxes in applicable states, and manage multi-state annual report filings to maintain compliance.

- Update policies to track relocations and avoid accidental nexus.

Failing to comply with nexus rules can result in serious financial consequences. Proactively managing compliance ensures your business avoids penalties and stays on the right side of state tax laws.

Why Remote Work Increases State Tax Nexus Risk

What State Tax Nexus Means

State tax nexus refers to the legal connection between a business and a state, which requires the business to register, collect taxes, and file returns. This often requires appointing a registered agent service to handle official state correspondence. This connection can be established through either a physical or economic presence. For businesses operating remotely, the distinction lies in how each type of nexus is triggered. Economic nexus typically kicks in when a business reaches $100,000 in annual sales or completes 200 separate transactions in a state. On the other hand, physical presence has no minimum threshold – any level of presence can establish nexus.

How Remote Employees Create Nexus

Hiring remote employees can lead to new tax obligations in states where those employees work. Even a single employee working from home in a different state is enough to establish physical nexus. This is true regardless of their job function, whether it’s sales, coding, or administrative work.

"A single employee working in a state can be enough to create nexus for both sales tax and income or franchise tax purposes." – Cherry Bekaert

A key example of this is the Telebright Corp. v. Director, New Jersey Division of Taxation case. In this situation, a Maryland-based company employed one remote worker in New Jersey who wrote software code from home. The New Jersey court ruled that this single employee’s presence constituted "doing business" in the state, making the company liable for New Jersey’s Corporation Business Tax. This case highlights how just one remote hire can trigger a host of tax obligations.

Once nexus is established, the tax responsibilities can multiply. A remote employee can trigger requirements for corporate income tax, franchise tax, sales and use tax, payroll withholding, state unemployment insurance, and workers’ compensation – all at the same time. This creates a complex web of compliance issues for businesses to navigate.

Compliance Risks Across Multiple States

Managing tax compliance becomes even more challenging for businesses with distributed teams. Each state has unique thresholds, regulations, and filing deadlines, adding layers of complexity for companies operating across multiple states.

One major issue is that nexus creates a filing obligation even if no taxes are owed. Many states charge minimum franchise taxes or capital-based fees simply for doing business there. For example, startups often find themselves required to file corporate returns after reaching $50,000 in payroll within a state. Failing to meet these obligations can result in penalties, back taxes, and other financial liabilities, making compliance a critical concern for businesses with remote employees.

Business Activities That Trigger State Tax Nexus

Employees, Contractors, and Sales as Nexus Triggers

Remote businesses can establish tax nexus in several ways, with people, property, and sales activities being the most common triggers. Importantly, each of these operates independently.

A W-2 employee working remotely creates physical nexus immediately, regardless of their role. Mey Morales from The Sales Tax People emphasizes this point:

"A developer writing code in their basement creates the same tax obligation as a sales rep closing deals."

Independent contractors are just as impactful. For example, a contractor performing on-site tasks like installations or providing technical support can trigger nexus.

Another key trigger is inventory storage, which businesses often overlook. Whether goods are stored in a third-party facility or through FBA, nexus is established in every state where inventory is held. A notable case is the Arizona Court of Appeals’ 2024 ruling against RockAuto, LLC, an online auto-parts retailer. Despite having no offices or employees in Arizona, the company’s use of six in-state independent suppliers to store and fulfill orders led to nexus. The court found these activities were "significantly associated" with the company’s ability to maintain a market in the state, resulting in an $8 million tax assessment for the period between April 2013 and April 2019.

Even short-term activities like attending trade shows, conducting on-site training, or making repair visits can trigger nexus. Some states, however, offer limited grace periods for these temporary activities.

Physical Presence Nexus vs. Economic Nexus

To understand the obligations of remote businesses, it’s essential to differentiate between the two main types of nexus: physical presence nexus and economic nexus. A business can trigger one type without the other, but often, both are triggered simultaneously.

Physical presence nexus depends on tangible factors like employees, property, or inventory located in a state. There’s no minimum threshold for this type of nexus.

Economic nexus, on the other hand, is based solely on revenue or transaction volume, regardless of physical location. Most states set the threshold at $100,000 in annual sales or 200 separate transactions within a 12-month period.

| Feature | Physical Presence Nexus | Economic Nexus |

|---|---|---|

| Primary Trigger | Employees, contractors, offices, or inventory | Revenue volume or number of transactions |

| Common Threshold | Often a single employee or any physical property | Typically $100,000 in sales or 200 transactions |

| Tax Types Affected | Sales, Income, Payroll, and Franchise taxes | Primarily Sales and Income taxes |

| Timing | Starts immediately upon presence | Starts once the threshold is exceeded |

| Remote Work Impact | High – one remote hire can trigger obligations | Based on customer location, not worker location |

As Rob Galloway, Editor at Checkpoint Catalyst, explains:

"Physical presence remains a fully independent basis for taxpayers to establish sales and use tax nexus in a state due to their physical footprint."

Even after the Wayfair decision introduced economic nexus nationwide, physical presence rules remain in effect and are actively enforced.

How Nexus Rules Differ by State

State-specific rules add another layer of complexity to compliance. Each state has its own thresholds, rules, and tax types, making it a challenge for remote businesses to navigate.

For state income and franchise taxes, many states apply "factor presence" standards. For instance, thresholds like $50,000 in in-state payroll or property or $150,000 in in-state sales can establish income tax nexus. These thresholds are separate from sales tax rules and apply even if a business lacks a physical office in the state.

Federal protections under Public Law 86-272 offer limited relief. This law shields businesses from state income tax if their activities are restricted to soliciting orders for tangible goods. However, it doesn’t protect service providers, SaaS companies, or businesses with active online interactions, such as chat tools or cookies. Increasingly, states are targeting these digital activities as triggers for nexus.

Lastly, using a Professional Employer Organization (PEO) for payroll doesn’t eliminate nexus exposure. As Kruze Consulting explains:

"PEOs are fantastic for benefits and HR compliance, but they do not change which states can tax your corporation’s income."

States focus on where the work is performed, not who processes the payroll.

What Happens When You Ignore Nexus Obligations

Unexpected Filing Obligations for Remote Businesses

Ignoring nexus obligations can lead to a cascade of unexpected filing requirements, especially for remote businesses. Many companies don’t realize they’ve triggered nexus until it’s too late. For example, hiring a single remote employee in a new state can immediately create filing obligations – there’s no grace period, no minimum revenue threshold, and no exemptions for small businesses. This one hire can result in multiple tax obligations, including sales tax, corporate income tax, franchise tax, and payroll tax, even in states where the company has never filed before. With multi-state nexus and compliance, the complexity grows quickly, as each state has its own rules, deadlines, and filing schedules. These unanticipated responsibilities can lead to serious financial consequences.

Penalties, Back Taxes, and Backdated Liabilities

As The Sales Tax People explain:

"The obligation [to collect sales tax] doesn’t go away just because you didn’t know about it."

Once nexus is triggered, back taxes start accumulating from that date, along with interest on unpaid amounts. States also impose penalties for failing to file or pay, regardless of whether the business was aware of its obligations. In states like New York, businesses may face minimum franchise or capital-based taxes even if they’re operating at a loss. This means that simply "doing business" in a state can result in significant costs.

Audits raise the stakes even higher. If a state discovers non-compliance during an audit, it may impose maximum penalties and review all unregistered activity. On the other hand, voluntary disclosure programs can reduce the look-back period and may waive penalties in some cases. Nexus issues can also complicate funding rounds and acquisitions. During due diligence, unresolved tax liabilities can lead to purchase price adjustments, escrow demands, or transaction delays.

"A single remote employee… can quickly generate thousands of dollars in unrecognized tax liability, plus penalties and interest." – Mey Morales, Staff Researcher, The Sales Tax People

This highlights why businesses need to go beyond basic payroll solutions to manage their tax obligations.

Why Payroll or HR Outsourcing Is Not Enough

Relying on payroll services or Professional Employer Organizations (PEOs) isn’t enough to cover all state tax requirements. While these services handle employee-level compliance – such as withholding, unemployment insurance, and benefits – they don’t manage broader business obligations like registering your company or filing corporate income and franchise tax returns.

Payroll data processed through a PEO isn’t hidden from state tax authorities. In fact, states often use this data to determine whether a business has nexus and should be filing additional returns.

"Payroll processed by a PEO is still visible to the state, and they use that data to infer income/franchise nexus. That surprise often shows up later as unexpected startup tax notices and penalties." – Kimberly Quisenberry, Director of Income Tax, Kruze Consulting

Here’s a breakdown of what PEOs handle versus what your business must manage:

| Obligation | Handled by PEO | Business Must Handle |

|---|---|---|

| Employee withholding & W-2s | ✓ | |

| Unemployment insurance | ✓ | |

| Business registration | ✓ | |

| Corporate income tax returns | ✓ | |

| sales tax registration & filing | ✓ | |

| Franchise tax returns | ✓ |

The hiring process and tax compliance process must work together. Hiring a remote employee in a new state isn’t just an HR decision – it’s a major tax event for your company. Proper management of nexus requires registering your business and filing the necessary returns in each applicable state, a process that will be explored further in the next section.

sbb-itb-ba0a4be

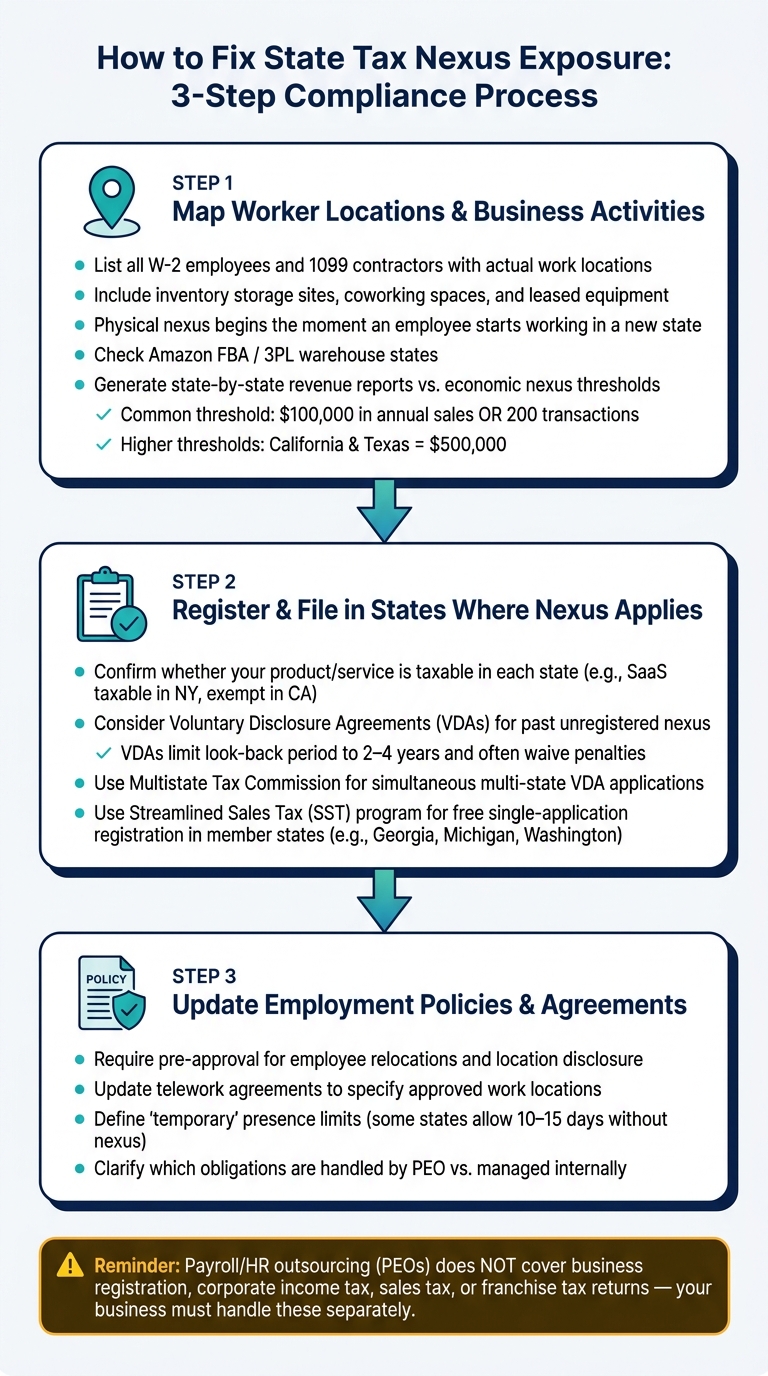

How to Fix Nexus Exposure Step by Step

Managing nexus exposure effectively starts with understanding where your business activities and employees create obligations. From there, it’s about ensuring proper state registrations and updating internal policies to avoid future issues. Here’s a breakdown of the process:

Step 1: Map Worker Locations and Business Activities

Start by listing all your W-2 employees and 1099 contractors, along with their actual work locations. This includes not just office spaces but also inventory storage sites, coworking spaces, and leased equipment. Remember, physical nexus begins the moment an employee starts working in a new state – even if that employee was hired remotely months ago.

If you rely on Amazon FBA or third-party logistics (3PL) providers, your products might be stored in warehouses across multiple states, sometimes without you realizing it. To identify potential nexus, generate state-by-state revenue reports and compare them to economic nexus thresholds. These thresholds often sit at $100,000 in annual sales or 200 transactions, though states like California and Texas set their thresholds higher at $500,000.

This mapping exercise is critical because it pinpoints every state where your business has a physical or economic presence. Each of these locations could trigger tax obligations.

Step 2: Register and File in States Where Nexus Applies

Before registering in a state, confirm whether your product or service is taxable there. For instance, SaaS products are taxable in New York but are generally exempt in California. Registering in a state unnecessarily can create extra filing burdens, so it’s important to verify this upfront.

If your business has had unregistered nexus in the past, consider applying for a Voluntary Disclosure Agreement (VDA). VDAs typically limit the look-back period to 2–4 years and often waive penalties. The Multistate Tax Commission offers a program for simultaneous applications across multiple states, while the Streamlined Sales Tax (SST) program allows businesses to register in member states – like Georgia, Michigan, and Washington – through a single, free application.

"Coming forward under a VDA almost always costs less than being discovered through an audit, and it eliminates the open-ended statute of limitations problem that unregistered businesses face." – Donnie L. Davis, CPA, DMG Worldwide Inc

Once your registrations are complete, shift focus to updating your internal policies to prevent similar issues in the future.

Step 3: Update Employment Policies and Agreements

Revising internal policies is key to addressing current exposure and avoiding future non-compliance. Introduce a policy requiring employees to get pre-approval for relocations and to disclose their locations. This allows your finance team to assess potential tax implications – like income, franchise, or sales tax – before a move inadvertently triggers nexus.

Update telework agreements to specify approved work locations and include clauses that prohibit unapproved remote work. Define what "temporary" presence means for your business. Some states allow employees to work in-state for 10–15 days without triggering nexus, but many states don’t offer such exceptions. Without a formal policy, you risk both compliance issues and a lack of documentation to support your stance.

| Policy Change | What It Prevents |

|---|---|

| Relocation pre-approval and location disclosure | Accidental nexus from unreviewed moves and untracked presence |

| Temporary presence limits | Unintentional crossing of state-specific thresholds |

| PEO limitation disclosure | Misunderstandings about payroll providers’ roles |

Lastly, clarify which registrations are handled by your Professional Employer Organization (PEO) and which are managed internally. Payroll compliance and corporate tax compliance are separate responsibilities, and documenting this distinction helps ensure everyone is on the same page.

How to Stay Compliant Across Multiple States

Once you’ve registered in the appropriate states and updated your policies, the real challenge begins: maintaining compliance as your business grows and your team becomes more mobile. This isn’t a one-and-done task – it’s a continuous process that requires regular monitoring and scheduled reviews.

Tracking Employee Locations and Business Activities

Physical nexus can be triggered the moment an employee starts working in a new state. Even a temporary relocation by a single team member can create new obligations overnight.

To stay ahead, require employees to report any changes in their work location immediately – whether it’s a permanent move, a temporary stay, or an extended visit to another state. Combine this with a monthly review of your trailing 12-month sales and transaction counts against each state’s economic nexus thresholds. Many states set these thresholds at $100,000 in sales or 200 transactions, though some, like New York, have higher thresholds – typically $500,000 in sales and 100 transactions.

Don’t overlook third-party inventory locations. Recent legal decisions highlight the risks of ignoring where your inventory is stored. For example, using in-state distributors for fulfillment can establish a physical nexus, even if you don’t have employees or offices in that state.

These tracking practices naturally lead to the next critical step: conducting regular nexus reviews.

Periodic Nexus Reviews and Record-Keeping

Regularly reviewing your nexus status is key to staying ahead of state audits. Plan to conduct these reviews annually or whenever you hire new employees, expand into new markets, or introduce new products. During these reviews, cross-check your employee roster, inventory locations, contractor agreements, and sales data against the latest state-specific thresholds.

Maintain detailed, state-specific records for sales, payroll, and property. These records are essential for accurate income apportionment and can be a lifesaver if you’re audited or need to defend a Net Operating Loss claim. Also, once you’re registered in a state, don’t forget to file tax returns – even if there’s no taxable activity. Skipping a return, even a zero-dollar one, could lead to automated penalty notices.

To stay on top of deadlines, create a centralized filing calendar. This calendar should track registration renewals, return due dates, and threshold review schedules for every state where you operate, often with the help of a registered agent for multistate tax compliance. Without such a system, you risk missing deadlines, which could expose your business to back-tax assessments going back 5, 7, or even 10 years.

To streamline these processes, consider using an integrated platform.

Using BusinessAnywhere to Manage Multi-State Compliance

After setting up your registration and review systems, a unified compliance dashboard can help ensure nothing slips through the cracks. BusinessAnywhere centralizes services like registered agent management, compliance alerts, annual report filings, and ongoing company maintenance into one online platform. This ensures that all legal and tax correspondence is handled promptly across every state where you operate.

For businesses managing nexus in multiple states, this approach reduces the risk of missed deadlines and keeps you on track with state obligations. With additional support services like bookkeeping, accounting, and S-Corp tax filings, BusinessAnywhere can help lighten the administrative load, allowing you to focus on growing your business without unnecessary stress.

Conclusion: Managing State Tax Nexus for Long-Term Remote Business Success

State tax nexus can create serious challenges for remote businesses. Even one remote employee in a different state can trigger immediate tax obligations in that state – sometimes starting from day one. Ignoring these responsibilities only increases penalties and interest over time.

Donnie L. Davis, CPA, puts it plainly:

"The cost of getting this right is a fraction of the cost of getting caught." – Donnie L. Davis, CPA, DMG Worldwide Inc

Consider this example: A business that remains unregistered for two years while owing $30,000 annually in sales tax could face liabilities exceeding $60,000 once penalties and interest are added. Beyond monetary consequences, unresolved nexus issues can also jeopardize funding opportunities or acquisitions. Investors routinely examine unpaid state taxes, and unresolved liabilities can lead to reduced purchase prices or altered funding agreements.

Taking a proactive approach is far easier than dealing with the fallout of non-compliance. Steps like tracking employee locations, monitoring economic nexus thresholds, and filing returns during loss years to lock in Net Operating Losses (NOLs) can safeguard your business over time. If historical exposure is already an issue, a Voluntary Disclosure Agreement (VDA) can limit your lookback period to 2–4 years and waive penalties – but only if you act before the state reaches out to you. These steps not only minimize risk but also simplify ongoing compliance.

Platforms like BusinessAnywhere offer a centralized solution, combining registered agent services, compliance alerts, annual report filings, bookkeeping, and S-Corp tax support. For remote businesses juggling multi-state obligations, having everything in one dashboard ensures deadlines and requirements don’t slip through the cracks.

FAQs

Does one remote employee create nexus?

Yes, in several states, having just one remote employee working from home in a different state can create a tax nexus. This means the employer may need to address state compliance requirements, including filing income or franchise taxes, managing payroll obligations, and often registering for sales tax.

What taxes can nexus trigger besides sales tax?

In the U.S., having a nexus in a state doesn’t just mean dealing with sales tax – it can also bring about responsibilities like state income or franchise taxes, which are typically tied to physical presence or economic activity. Beyond that, businesses might face obligations such as payroll taxes for remote employees, gross receipts or excise taxes, and ensuring compliance with unclaimed property reporting. BusinessAnywhere simplifies managing these intricate, state-specific requirements, helping entrepreneurs stay on top of their obligations.

How can I resolve past nexus issues without triggering an audit?

To tackle past nexus issues head-on, take a close look at your business activities. Check for factors like remote employees, inventory stored in third-party warehouses, or sales surpassing state-specific thresholds. It’s smart to work with a tax advisor to evaluate your potential exposure before states step in. For businesses operating remotely, services like BusinessAnywhere can assist with compliance management to keep things on track. Acting early is crucial, as states can impose penalties without giving prior notice.