If you’re running a business, choosing between an LLC and an S Corp can significantly affect your taxes in 2026. Here’s the key takeaway:

- LLC: Simpler setup with all profits subject to a 15.3% self-employment tax. Best for businesses earning less than $60,000 annually.

- S Corp: Lets you split income into a salary (taxed at 15.3%) and distributions (not subject to self-employment tax), saving thousands for businesses with profits over $80,000. However, it comes with higher compliance costs (higher compliance costs ($1,500–$4,500 annually).,500–$4,500 annually).

Quick Comparison

| Feature | LLC (Default) | S Corp Election |

|---|---|---|

| Self-Employment Tax | 15.3% on all profit | 15.3% on salary only |

| QBI Deduction | Full net profit | Distributions only |

| Compliance Costs | $0–$1,500/year | $1,500–$4,500/year |

| Best for | Profits under $60,000 | Profits over $80,000 |

The break-even point for switching to an S Corp is typically $40,000–$80,000 in annual profits. Below this, the added costs outweigh the savings. Above $80,000, S Corp status can save $5,000–$15,000 annually by reducing self-employment tax. To secure these savings, you must file IRS Form 2553 to elect S Corp status.

For 2026, changes like the increased Social Security wage base ($184,500) and adjustments to the Qualified Business Income (QBI) deduction further impact your choice. S Corps often offer better tax benefits, but only if you’re prepared to handle the administrative complexity.

How S Corps and LLCs Are Taxed

LLC Taxation: Pass-Through Income and Self-Employment Taxes

If you operate a single-member LLC, your net business income flows directly to your personal tax return. This means 100% of your net profit is subject to self-employment tax, which is currently set at 15.3%.

Here’s how that tax rate breaks down: 12.4% goes toward Social Security (up to the first $184,500 of earnings in 2026), while the remaining 2.9% is allocated to Medicare, which applies to all earnings without a cap. Additionally, if you’re earning more than $200,000 as an individual filer – or $250,000 if filing jointly – you’ll owe an extra 0.9% Medicare surtax.

One of the perks of an LLC is its simplicity. There’s no need to run payroll, and you can withdraw funds as needed through owner draws. Tax filing is also straightforward: single-member LLCs use Schedule C, while multi-member LLCs file Form 1065. On top of that, your entire net profit qualifies for the 20% Qualified Business Income (QBI) deduction, which became a permanent benefit under the One Big Beautiful Bill Act signed on July 4, 2025.

S Corp Taxation: Splitting Income Between Salary and Distributions

If you elect S Corp status by filing Form 2553, your income is divided into two parts: a W-2 salary (subject to payroll taxes) and distributions, which are exempt from self-employment tax. This setup can result in substantial tax savings. However, the IRS requires you to pay yourself a “reasonable salary” based on what someone in your position and industry would typically earn.

"The IRS expects owner-employees to pay themselves a fair salary for the work they perform. That salary is subject to payroll taxes. Distributions are not. That’s the lever." – Chris Landqvist, Managing Partner, Weston Tax Associates

S Corp owners do face a tradeoff when it comes to the QBI deduction. While LLC owners can apply the 20% deduction to their full net profit, S Corp owners can only claim it on the distribution portion of their income – not their salary. Despite this limitation, the savings on self-employment taxes often outweigh the reduced deduction, especially if your profit exceeds $40,000 to $60,000.

LLC vs S Corp Tax Comparison

Here’s a quick look at how taxation differs between LLCs and S Corps:

| Feature | LLC (Default) | S Corp Election |

|---|---|---|

| Self-Employment Tax | 15.3% on ALL net profit | 15.3% on salary ONLY |

| Compensation Type | Owner draws (no payroll) | W-2 Salary + Distributions |

| Payroll Requirement | No | Yes (Mandatory for owners) |

| Tax Return Form | Schedule C or Form 1065 | Form 1120-S |

| QBI Deduction | Based on full net profit | Based on distributions only |

| Administrative Effort | Low | High (Quarterly filings, W-2s) |

The breakeven point for choosing an S Corp often falls between $40,000 and $80,000 in annual net profit. Below this range, the extra administrative costs – typically $1,500 to $4,500 per year – can cancel out any tax savings. Once you’re above this threshold, the self-employment tax savings generally justify the added complexity.

sbb-itb-ba0a4be

2026 Tax Law Changes That Affect Your Choice

2026 Social Security Wage Base Increase to $184,500

The Social Security wage base is climbing from $176,100 in 2025 to $184,500 in 2026. This bump directly impacts payroll tax obligations for business owners.

For default LLCs, the 12.4% Social Security tax applies to every dollar of net profit up to $184,500. So, if your business nets the full $184,500, your Social Security tax bill will hit $22,878. On the other hand, S Corp owners are taxed differently. The 12.4% rate only applies to their W-2 salary, not to distributions, offering a potential tax advantage as the wage base rises.

Take this example: A consulting business with $120,000 in net income for 2026 would pay $18,378 in self-employment tax as a standard LLC. Switching to S Corp status with a reasonable $60,000 salary reduces the employment tax to $9,180, saving $9,198 annually. If your net income ranges between $80,000 and $100,000, the increased wage base might make it worth reconsidering S Corp status for potential savings.

These changes pave the way for additional updates in 2026, including adjustments to the Qualified Business Income (QBI) deduction.

Qualified Business Income Deduction Updates for 2026

The One Big Beautiful Bill Act (OBBBA), signed on July 4, 2025, made the 20% Qualified Business Income (QBI) deduction permanent. However, new provisions in 2026 introduce changes that impact LLCs and S Corps differently.

First, there’s a new $400 minimum deduction for businesses with at least $1,000 in qualified income and material participation. Even if the standard 20% calculation results in a lower amount, you’re guaranteed at least $400. Second, the phase-out ranges have expanded: single filers now phase out over a $75,000 range, while joint filers phase out over $150,000. This gives more high-income taxpayers a shot at claiming at least part of the deduction.

For higher earners, the QBI deduction is further restricted by W-2 wages once taxable income surpasses $203,000 for single filers or $406,000 for married couples filing jointly. Here’s where S Corps have an edge. S Corp owners who pay themselves a W-2 salary establish a wage base that qualifies for the deduction, while solo LLC owners without employees often have a $0 wage base, which can mean a $0 QBI deduction at higher income levels.

To maximize the QBI deduction, high-income S Corp owners should aim for a salary that’s roughly 35–40% of net income. This ensures enough W-2 wages to qualify for the deduction without overpaying payroll taxes. Additionally, for those near the income thresholds, contributing to a retirement account like a SEP-IRA or Solo 401(k) can help lower taxable income and keep you within the phase-out range.

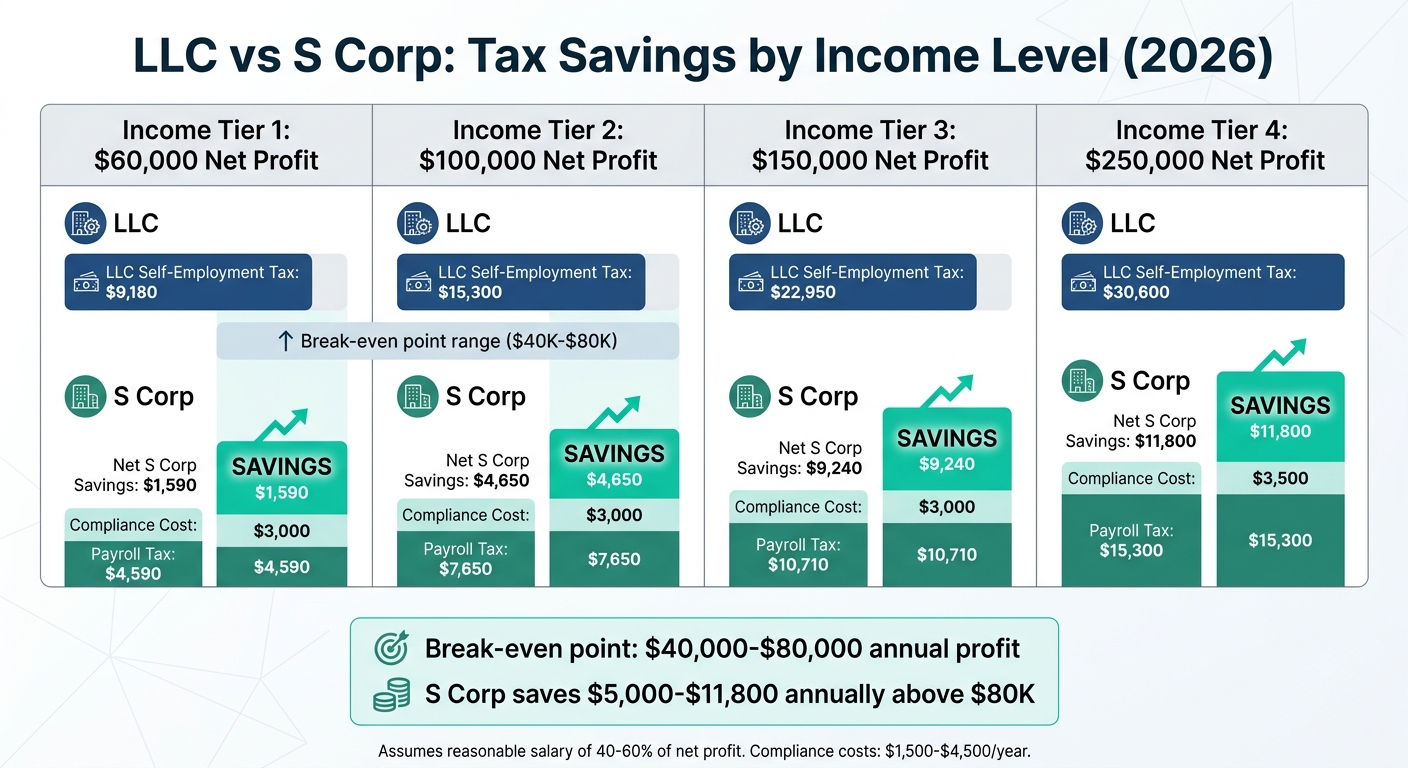

Tax Savings Examples by Income Level

Tax Comparison at $60K, $100K, $150K, and $250K Profit

Let’s dive into how an S Corp election can impact taxes at different profit levels in 2026. These examples highlight the potential savings compared to staying as an LLC.

At $60,000 in net profit, an LLC owner pays about $9,180 in self-employment tax (15.3% applied to the full profit). In contrast, an S Corp owner who sets a reasonable salary of $30,000 pays approximately $4,590 in payroll taxes. That’s a savings of about $1,590.

With a profit of $100,000, the LLC owner’s self-employment tax rises to around $15,300. However, an S Corp owner who takes a $50,000 salary pays roughly $7,650 in payroll taxes. Savings: ~$4,650.

At $150,000 in net profit, the LLC owner faces self-employment taxes of about $22,950. An S Corp owner, assigning a $70,000 salary, pays around $10,710 in payroll taxes, resulting in savings of ~$9,240.

Finally, with $250,000 in profit, the LLC’s self-employment tax caps at ~$30,600 due to the Social Security wage base limit. Meanwhile, an S Corp owner taking a $100,000 salary pays about $15,300 in payroll taxes. Savings: ~$11,800.

| Net Profit | LLC Self-Employment Tax | S Corp Payroll Tax | Compliance Cost | Net S Corp Savings |

|---|---|---|---|---|

| $60,000 | ~$9,180 | ~$4,590 | $3,000 | ~$1,590 |

| $100,000 | ~$15,300 | ~$7,650 | $3,000 | ~$4,650 |

| $150,000 | ~$22,950 | ~$10,710 | $3,000 | ~$9,240 |

| $250,000 | ~$30,600 | ~$15,300 | $3,500 | ~$11,800 |

These figures show how profits can translate into significant savings with the right structure.

When S Corps Deliver Greater Tax Savings

The examples above make it clear: as profits grow, the benefits of the S Corp structure become more pronounced. Typically, the break-even point for choosing S Corp status is between $40,000 and $80,000 in annual net profit. Below $60,000, the additional compliance costs often outweigh the savings, making default LLC treatment a better choice than a corporation. Randy Martin, CPA at IRSProb.com, explains that profits under $60,000 favor the LLC structure, while profits above $80,000 almost always justify an S Corp election.

For those earning more than $80,000, S Corp status can lead to yearly tax savings ranging from $5,000 to $11,000. The key is setting a reasonable salary – usually 40% to 60% of net profit – to balance tax-free distributions with IRS compliance.

"Setting your salary too low is the number one S-Corp audit trigger – the IRS has won every major court case on this issue." – Tom Woolley, MBA, Today CFO

S Corps work best for businesses that distribute most of their profits rather than reinvesting in inventory or equipment. If your business requires significant reinvestment, sticking with the simpler LLC structure may make more sense, even as income rises.

Compliance Requirements and Costs

Annual Costs for LLCs vs. S Corps

If you opt for a default LLC, the process is relatively straightforward. Single-member LLCs report their income on Schedule C of the owner’s personal Form 1040, while multi-member LLCs file Form 1065 instead. There’s no requirement to run payroll, make quarterly tax deposits, or issue W-2 forms. Because of this simplicity, annual compliance costs tend to fall between $0 and $1,500.

However, S Corps come with more administrative responsibilities. Filing Form 1120-S, issuing Schedule K-1 forms to shareholders, and running formal W-2 payroll for owner-employees are all mandatory. Payroll involves withholding taxes and filing quarterly Form 941 payroll returns. These additional requirements push annual compliance costs up to $1,500–$4,500.

Here’s a breakdown of those costs for S Corps:

- Payroll processing: $500–$2,000 per year

- Form 1120-S preparation: $500–$2,000

- Additional bookkeeping: $200–$500

- State-specific fees: For example, California imposes a 1.5% franchise tax on S Corp net income, with a minimum annual payment of $800.

Failing to meet payroll tax deposit deadlines can also lead to IRS penalties, which start at 2% and can rise to 15%.

"The S Corp election is one of the most powerful tax-saving tools available to profitable small businesses, but it’s not free. There’s a real cost in complexity, compliance, and professional fees."

- Slava Akulov, Founder, Jupid

On top of these costs, S Corps face additional operational compliance requirements. They must maintain bylaws and meeting minutes, even if there’s only one owner. Their corporate tax return is due on March 15 – earlier than the April 15 deadline for LLCs. Another challenge? The IRS closely monitors "reasonable salary" determinations for S Corps, which increases the likelihood of audits compared to default LLCs.

How to Convert Your LLC to an S Corp

Despite the extra administrative work, many business owners choose to convert their LLCs to S Corps to take advantage of potential tax benefits.

Converting your LLC to an S Corp is simpler than it sounds. The process doesn’t change your legal structure at the state level – it only affects how the IRS taxes your business income. To make the switch, you’ll need to file IRS Form 2553 (Election by a Small Business Corporation).

For the 2026 tax year, calendar-year businesses must file Form 2553 by March 16, 2026 (since March 15 is a Sunday). If you’re starting a new business, you have 2 months and 15 days from your formation date to file. Missed the deadline? You can request retroactive relief under Rev. Proc. 2013-30 for up to 3 years and 75 days.

Before filing, ensure your LLC meets these eligibility criteria:

- Must be a domestic entity.

- Can have no more than 100 shareholders, all of whom must be U.S. citizens or residents.

- May only issue one class of stock.

Additionally, some states – like California, New York, and New Jersey – require a separate S Corp election at the state level.

If you’re looking for help, services like BusinessAnywhere’s S Corp Tax Election can handle the process for just $97. They’ll file Form 2553 and ensure you meet all deadlines. Once your S Corp election is approved, you’ll need to set up payroll. Tools like Gusto or ADP can simplify this by automating quarterly Form 941 filings and year-end W-2 processing, helping you avoid manual errors.

After converting, your tax obligations change immediately. You’ll stop filing Schedule C and start filing Form 1120-S, along with Schedule K-1s for each owner. You’ll also need to establish a "reasonable salary" for yourself – typically 40% to 60% of your net profit – and process it through W-2 payroll. To defend against potential IRS scrutiny, it’s a good idea to document your salary methodology using data from the Bureau of Labor Statistics or industry salary surveys.

This straightforward conversion process allows business owners to take advantage of tax benefits while balancing the added compliance requirements. Preparing ahead ensures you’re ready to make the most of these opportunities in 2026.

Which Structure Saves More on Taxes?

S Corp tax savings become evident when your net profit exceeds $80,000 annually. For profits below $60,000, the additional administrative work often makes sticking with an LLC the better choice. For instance, if your business nets $150,000, switching to an S Corp could save you about $7,484 per year. At $250,000, those savings grow to around $12,936 – even after factoring in compliance costs.

The difference boils down to how self-employment taxes are handled. With an S Corp, only the W-2 salary is subject to the 15.3% self-employment tax, while distributions are not. This contrasts with an LLC, where the entire profit is taxed at that rate. This distinction plays a big role in shaping your 2026 tax planning decisions.

"If your business nets more than $80,000/year, an S-Corp election could save you $5,000–$15,000 annually in self-employment taxes."

2026 Tax Planning Decisions

When planning for 2026, consider three main factors: income level, income stability, and administrative capacity. If your net profit is below $60,000, your income is highly variable, or you prefer a simpler filing process, sticking with an LLC may be the smarter route. On the other hand, if your net profit consistently exceeds $80,000 and you’re okay with managing payroll, electing S Corp status could be a savvy move.

State-specific costs also matter. For example, California imposes a 1.5% franchise tax on S Corp net income, with a minimum annual fee of $800. These expenses can chip away at – or even cancel out – your federal tax savings, so include them in your calculations.

If you decide to make the switch, file Form 2553 by March 17, 2026 (since March 15 falls on a Sunday) to ensure the election applies to the 2026 tax year. To avoid IRS scrutiny, document your salary methodology using data from the Bureau of Labor Statistics or industry surveys. Keep in mind, setting your salary too low is a major audit trigger, and the IRS has consistently won court cases on this issue.

FAQs

What counts as a “reasonable salary” for an S Corp owner in 2026?

A "reasonable salary" for an S Corp owner in 2026 is essentially what someone with a comparable role in the same industry would earn. Factors like your experience, the profits of the business, and typical industry standards play a key role in determining this amount. The salary should also meet IRS requirements while striking a balance to avoid unnecessarily high payroll taxes. Staying within these benchmarks helps ensure compliance and keeps your business on the right track.

How do state taxes and fees affect S Corp vs LLC savings?

State taxes and fees can play a big role in shaping the tax benefits of S Corps and LLCs in 2026. While federal strategies often aim to cut down on self-employment taxes, state-specific charges – like franchise taxes or annual fees – can eat into the savings for LLCs. On the flip side, some states have minimal or even no fees for LLCs, which might make them a more affordable option. To figure out which structure works best for your wallet, it’s crucial to dig into your state’s tax rules and compare the costs.

Can I switch from an LLC to an S Corp mid-year and still get 2026 tax savings?

Yes, it’s possible to switch from an LLC to an S Corporation mid-year in 2026. To make this change, you’ll need to file Form 2553 within the IRS’s required timeframe. If you miss the deadline, the IRS might accept a late filing, but you’ll need to provide a valid reason and gain their approval. Acting quickly ensures you can start leveraging S-Corp tax benefits and potentially reduce your 2026 tax liability.