Choosing the right business structure matters. Here’s the breakdown:

- Sole Proprietorship: The simplest option. No paperwork, but your personal assets are at risk if the business incurs debts. Taxes pass through to your personal return.

- DBA (Doing Business As): Not a legal structure. It lets you operate under a trade name but offers no liability protection.

- LLC (Limited Liability Company): A separate legal entity that protects personal assets. More formal LLC formation process with state filings and fees. Offers flexible tax election options.

Key takeaway: Sole proprietorships are great for low-risk, solo ventures. A DBA is just a name change. LLCs are best for liability protection and growth.

Quick Comparison

| Feature | Sole Proprietorship | DBA (Doing Business As) | LLC (Limited Liability Co.) |

|---|---|---|---|

| Legal Entity | No | No | Yes |

| Liability Protection | None | None | Yes |

| Tax Treatment | Pass-through | Follows entity | Flexible |

| Setup Cost | $0 | $25–$100 | $35–$500 |

| Compliance | Minimal | Periodic renewal | Annual filings |

Whether you’re starting small or planning big, your choice impacts liability, taxes, and effort. Keep reading for details on each option.

What is a Sole Proprietorship?

A sole proprietorship is the most straightforward business structure you can choose. In fact, the moment you start selling goods or services on your own, you’re automatically operating as a sole proprietor. Legally, there’s no distinction between you and your business – you’re considered one and the same.

This structure is incredibly common, making up about 73.1% of all businesses in the United States. Its popularity stems from its simplicity – there’s no startup cost or complex paperwork involved. However, the trade-off is unlimited personal liability. This means your personal assets, like your home or savings, could be at risk if your business faces debts or legal issues.

How a Sole Proprietorship Works

A sole proprietorship gives you complete control over every aspect of your business – pricing, operations, and even expansion decisions. There’s no need to file Articles of Organization or follow corporate formalities like holding board meetings.

From a tax perspective, sole proprietorships use pass-through taxation. This means all business income is reported directly on your personal tax return using Form 1040, Schedule C. Along with income tax, you’ll also pay a 15.3% self-employment tax and may need to make quarterly estimated payments if you owe $1,000 or more annually. Depending on your industry, you might also need local business licenses, zoning permits, or a seller’s permit. Additionally, if you want to operate under a name other than your legal name, you’ll need to register a DBA (Doing Business As) with your county or state.

One key limitation of this structure is its dependency on the owner. A sole proprietorship ends if the owner dies or becomes incapacitated, with all assets and liabilities transferring to the owner’s estate. This is different from corporations or LLCs, which exist independently of their owners.

Pros and Cons of a Sole Proprietorship

The biggest draws of a sole proprietorship are its simplicity and low cost. You don’t need to pay state filing fees to form one, and you have full control over the business without needing to consult partners or shareholders. Tax filing is also straightforward since everything is included in your personal tax return.

"Sole proprietorships are the most common type of business – and generally also the simplest and most affordable."

- Brad Tyler, Business Strategy and Intelligence Manager, Bank of America

But there are downsides. The most serious is that your personal assets are fully tied to your business liabilities. This makes liability insurance a must-have. Additionally, raising funds can be tough – you can’t sell stock or equity, and banks may see sole proprietorships as a higher lending risk. Some larger companies may also hesitate to sign contracts with sole proprietors, preferring the perceived stability of an LLC or corporation.

Take Sam Walton, for example. In 1962, he started Walmart as a sole proprietorship in Arkansas, running independent retail stores. Eventually, he transitioned to incorporating and going public.

The U.S. Small Business Administration highlights one of the key benefits:

"Sole proprietorships can be a good choice for low-risk businesses and owners who want to test their business idea before forming a more formal business."

While a sole proprietorship is perfect for testing the waters or running a low-risk business, it may not be the best long-term option as your business grows or faces increased liability. At that point, transitioning to a structure like an LLC could provide more protection by setting up an LLC.

sbb-itb-ba0a4be

What is a DBA (Doing Business As)?

A DBA, or "Doing Business As", is a registered trade name that lets you run your business under a name different from your legal one. It’s also referred to as a fictitious name, assumed name, or trade name. However, it’s important to note that a DBA doesn’t create a separate legal entity – it simply allows you to operate under a different name.

For example, if you’re a sole proprietor named John Smith but want to run your business as "Smith’s Landscaping", you’d register that name as a DBA. Similarly, if your LLC is called "Happy Tails LLC" and you decide to expand into landscaping under the name "Happy Lawns", you’d register a DBA instead of forming a new company.

"A DBA is not a business structure at all. It is a name registration that lets an existing entity operate under a different name."

- LegalClarity Team

DBAs are useful for branding and transparency – they connect a business name to its owner, which builds trust and credibility. However, they don’t offer liability protection, meaning your personal assets could still be at risk if your business faces debts or lawsuits. Additionally, a DBA doesn’t secure trademark rights, so someone else could register the same name unless you obtain a federal trademark. Unlike LLCs or corporations, a DBA doesn’t separate personal and business liabilities – it’s essentially a rebranding tool.

How a DBA Works

The process for filing a DBA is relatively simple, though it varies depending on your location. In some states, you file with the Secretary of State, while in others, you might need to go through the County Clerk or another local agency. Before filing, it’s essential to check the relevant government database to ensure the name you want is available.

The cost of registering a DBA typically ranges from $10 to $100, and some states may also require you to publish your new name in a local newspaper, which adds to the expense. A DBA certificate is often required to open a business bank account or accept checks under your business name rather than your personal name. Keep in mind that DBAs aren’t permanent – many states require renewal every five to ten years, and failing to renew could cause complications, such as losing the name or issues with your bank account. Additionally, changes in your business address or ownership may require updating your registration.

While the filing process is straightforward, it’s worth considering both the benefits and limitations of using a DBA.

Pros and Cons of a DBA

One major benefit of a DBA is the flexibility it provides for branding, and it does so at a relatively low cost. Instead of operating under your personal name – like "Jane Smith" – you can use a more professional and memorable name, such as "Jane’s Web Design." If you already have an LLC, DBAs allow you to manage multiple product lines or services under one legal entity, simplifying operations while expanding your market reach.

A DBA can also help maintain some privacy by keeping your personal name off business materials like signage and business cards. However, your identity is still part of public records.

The biggest downside is that a DBA doesn’t offer any liability protection. If your business faces debts or lawsuits, your personal assets are at risk.

"A DBA is simply a registration, not a legal business structure – and it offers no liability protection."

- Elyse Dillard, Content Specialist, LegalShield

Another drawback is the lack of strong name protection. While your DBA is registered in your jurisdiction, it doesn’t stop others in different counties or states from using the same name. For exclusive, nationwide protection, you’d need to apply for a federal trademark, which costs between $250 and $350 per class. Lastly, sole proprietors and partnerships cannot include terms like "Corporation", "Inc.", or "LLC" in their DBA, as these imply a formal corporate structure, which could limit how "established" your business appears.

What is an LLC (Limited Liability Company)?

An LLC, or Limited Liability Company, is a business structure authorized at the state level, designed to create a legal entity separate from its owners. This setup allows the LLC to own property, enter into contracts, and take on debts under its own name. Unlike Sole Proprietorships or DBAs, an LLC’s structure provides ongoing liability protection, even if the owner steps away from the business.

The standout feature of an LLC is its liability shield. This means your personal assets – like your home, car, or savings – are generally safe from business-related debts or lawsuits. The only financial risk you face is limited to the amount you’ve invested in the business.

"LLCs can be a good choice for medium- or higher-risk businesses, owners with significant personal assets they want protected, and owners who want to pay a lower tax rate than they would with a corporation."

- U.S. Small Business Administration

Beyond protecting your assets, forming an LLC adds a layer of credibility. It shows banks, investors, and vendors that your business is legitimate and not just a casual operation. Additionally, unlike sole proprietorships, which dissolve upon the owner’s death, an LLC can continue operating indefinitely if a succession plan is outlined in its operating agreement.

How an LLC Works

To establish an LLC, you’ll need to file Articles of Organization with your state. Filing fees vary, ranging from $35 to $500. You’ll also need to designate a registered agent, who must have a physical address in the state where the LLC is formed.

Once your LLC is set up, it’s important to obtain an EIN (Employer Identification Number). This helps protect your Social Security number and allows you to open a business bank account. Keeping personal and business finances separate is crucial to maintaining your liability protection.

LLCs are flexible when it comes to management. You can choose a member-managed structure, where the owners handle daily operations, or a manager-managed structure, where specific individuals are appointed to run the business. Even if you’re the only owner, drafting an operating agreement is essential. This document formalizes the separation between your personal and business affairs and outlines how the business will operate, including plans for unexpected events like incapacity or death.

To keep the liability shield intact, you must stay compliant with state requirements. This includes filing annual or biennial reports and paying state fees, which can range from less than $10 to several hundred dollars. Some states also impose flat franchise taxes, which can be as high as $800 annually, regardless of the LLC’s profit. Missing these filings could result in administrative dissolution, which would strip away your liability protection.

Pros and Cons of an LLC

One of the biggest advantages of an LLC is the protection it offers for personal assets, shielding them from business-related debts or lawsuits. Additionally, LLCs provide tax flexibility. Most LLCs use pass-through taxation, but they can also elect to be taxed as S or C corporations, depending on what works best for their financial situation. Under the Tax Cuts and Jobs Act, pass-through LLCs may even qualify for a 20% deduction on qualified business income.

For instance, starting in 2026, the Social Security portion of self-employment tax will apply only to the first $184,500 of income. High earners, however, will face an additional 0.9% Medicare surtax on income above $200,000 for individuals or $250,000 for joint filers. Electing S-corp status could help reduce self-employment taxes if your net profit significantly exceeds a reasonable salary.

However, LLCs do come with some downsides. They are generally more expensive and complex to maintain than sole proprietorships. Formation fees, ongoing filing requirements, and franchise taxes add to the cost. Additionally, maintaining the separation between personal and business finances requires careful recordkeeping. While LLCs protect against business debts, they don’t shield you from personal professional malpractice or personal loan guarantees. For those, liability insurance is a smart choice.

If your LLC operates under a name different from its registered one, you’ll need to file a DBA to ensure consistent liability protection.

This breakdown of LLCs highlights their benefits and challenges, setting the stage for a comparison with Sole Proprietorships and DBAs.

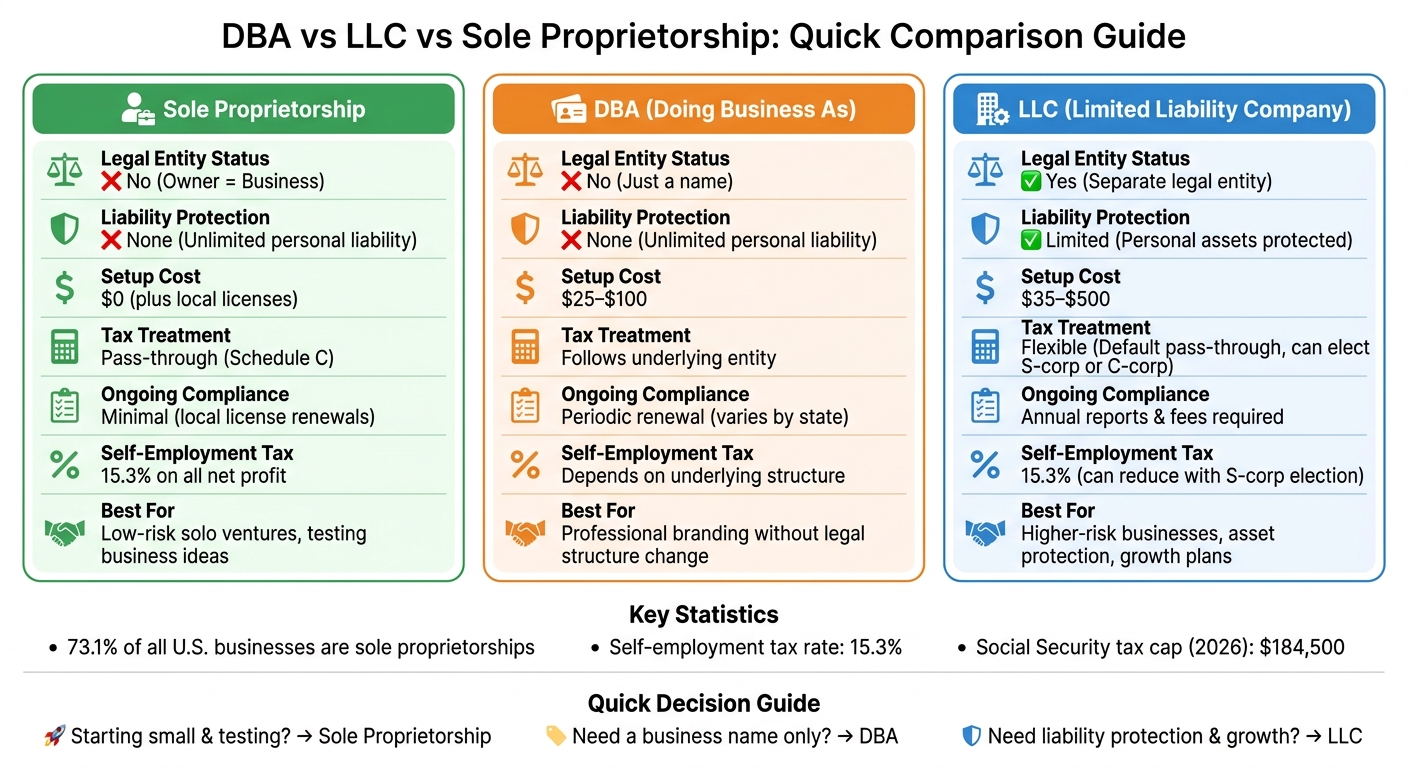

Sole Proprietorship vs DBA vs LLC: Side-by-Side Comparison

Here’s a detailed comparison of sole proprietorships, DBAs, and LLCs to help you better understand their differences. The table below outlines how these structures stack up across critical factors.

Comparison Table: Sole Proprietorship vs DBA vs LLC

| Feature | Sole Proprietorship | DBA (Doing Business As) | LLC (Limited Liability Co.) |

|---|---|---|---|

| Legal Entity | No (Owner = Business) | No (It is just a name) | Yes (Separate legal entity) |

| Liability Protection | None (Unlimited) | None (Unlimited) | Limited (Shields personal assets) |

| Tax Treatment | Pass-through (Schedule C) | Follows underlying entity | Flexible (Default pass-through) |

| Setup Cost | $0 (plus local licenses) | $25 – $100 | $35 – $500 |

| Ongoing Compliance | None | Periodic renewal (varies) | Annual reports & fees |

| EIN Required | Optional (unless employees) | Optional | Usually required |

| Management | Owner has total control | Owner has total control | Members or Managers |

This table highlights the key distinctions, helping you evaluate which structure might suit your business needs.

Liability Protection and Legal Entity Status

One of the most important factors to consider is liability protection. Sole proprietorships and DBAs don’t separate the owner from the business, meaning personal assets – like your home or savings – are at risk if the business incurs debts or faces lawsuits. An LLC, on the other hand, operates as a separate legal entity, offering a layer of protection for personal assets. However, this protection is only effective if you maintain clear boundaries between personal and business finances and sign contracts in the LLC’s name.

Another difference is how these structures handle business continuity. A sole proprietorship ceases to exist upon the owner’s death, which could complicate the transfer of assets. By contrast, an LLC can include succession plans in its operating agreement, ensuring the business can continue smoothly.

Tax Treatment and Compliance Requirements

The tax obligations for these structures vary significantly, as reflected in the table above.

- Sole Proprietorships: All business income is reported on Schedule C of the owner’s personal tax return. Self-employment tax is 15.3% of net profit, with the Social Security portion capped at $184,500 of income for 2026.

- DBAs: A DBA doesn’t alter the tax responsibilities of the underlying entity. For example, a sole proprietor using a DBA still files a Schedule C, while an LLC with a DBA follows LLC tax rules.

- LLCs: These offer flexibility in taxation. By default, they use pass-through taxation like a sole proprietorship. However, you can choose to be taxed as an S-corp or C-corp. In some cases, S-corp taxation can reduce self-employment taxes once your net profit exceeds a reasonable salary.

When it comes to compliance, sole proprietorships are the simplest, usually requiring only the renewal of local business licenses. DBAs often need periodic renewals, which can cost anywhere from $10 to $100. LLCs, however, have more involved requirements, including annual filings and fees.

Which Business Structure Should You Choose?

The best business structure for you depends on three key factors: your exposure to liability, how much administrative work you’re willing to take on, and whether you plan to grow beyond a solo operation. Here’s a breakdown to help you choose based on your goals.

When to Choose a Sole Proprietorship or DBA

If you’re testing a low-risk business idea, a sole proprietorship could be the simplest option. Freelance writers, graphic designers, and consultants often start this way because there’s no state filing fee, and tax reporting is straightforward – you just include a Schedule C with your personal tax return. As the U.S. Small Business Administration explains, "Sole proprietorships can be a good choice for low-risk businesses and owners who want to test their business idea before forming a more formal business".

For those who want a professional brand name without the complexity of forming an LLC, a DBA (Doing Business As) can be a good alternative. For example, if you’re "Jane Doe" but want to operate as "Bright Path Consulting", a DBA lets you use this business name for contracts or opening a business bank account. However, keep in mind that a DBA only registers the trade name – it doesn’t offer liability protection.

As your business grows or takes on more risk, transitioning to an LLC may be the next logical step.

When to Choose an LLC

An LLC (Limited Liability Company) makes sense if your business involves higher risks, such as physical safety concerns, handling sensitive data, or working in regulated industries like construction, healthcare, or finance. The main advantage? An LLC provides a liability shield that protects your personal assets from business debts or lawsuits.

LLCs also make it easier to expand. You can add members, attract investors, and build business credit – key steps for growing your reach, hiring employees, or securing funding. According to the U.S. Small Business Administration, LLCs are ideal for "medium- or higher-risk businesses, owners with significant personal assets they want protected, and owners who want to pay a lower tax rate than they would with a corporation". Additionally, once your profits exceed what you’d consider a reasonable salary, understanding S Corp vs LLC tax benefits can help you lower self-employment taxes by electing S-Corp status.

Business Examples for Each Structure

Sole Proprietorship: This structure is ideal for independent contractors or consultants with low overhead and minimal liability risk. For instance, a freelance photographer or virtual assistant could start as a sole proprietor to keep things simple while building their client base.

DBA: A DBA is a good fit for small businesses seeking better brand recognition without the added complexity of an LLC. For example, a sole proprietor running a local bakery might file a DBA to operate as "Sweet Street Bakery" instead of under their personal name, making it easier to market and manage the business professionally.

LLC: LLCs are often the go-to for businesses with higher risk or growth potential. Think of a software development firm managing client data or a contractor overseeing construction projects – both would benefit from the liability protection and flexibility an LLC offers.

Conclusion

This guide breaks down each option to help you decide on the best structure for your business.

When choosing between a sole proprietorship, DBA, or LLC, consider three key factors: liability protection, tax flexibility, and how much administrative work you’re ready to handle. A sole proprietorship is ideal for testing low-risk ideas with minimal hassle, while a DBA simply gives your business a professional name without changing its legal structure. On the other hand, an LLC creates a separate legal entity, which is crucial if you’re managing high-value contracts, hiring employees, or operating in higher-risk industries.

As your business grows, tax considerations become more important. Both sole proprietorships and single-member LLCs use pass-through taxation, but only an LLC can opt for S-Corp status when profits exceed a reasonable salary. With the self-employment tax rate at 15.3%, this option can lead to notable savings once your net income surpasses that threshold.

To maintain the liability protection of an LLC, keep personal and business finances separate. Open a dedicated business bank account, sign contracts under your LLC’s name, and create an operating agreement – even if you’re the sole member. These steps help reinforce the legal distinction between you and your business, safeguarding your long-term goals.

If your business has multiple members, is growing rapidly, or faces complex tax issues, seek advice from a tax professional or attorney. The upfront cost of expert guidance is a small price to pay compared to the potential risks of choosing the wrong structure or losing liability protection due to poor upkeep.

Evaluate your current risk level and revenue, and choose a structure that aligns with your future ambitions.

FAQs

Do I need a DBA if I already have an LLC?

If you have an LLC, you typically don’t need a DBA unless you plan to operate under a name different from your LLC’s registered name. A DBA lets your LLC use an alternate name for branding or marketing purposes. However, it doesn’t establish a separate legal entity or offer any additional liability protection. If your LLC’s registered name works for your needs, a DBA isn’t required.

When should I switch from a sole proprietorship to an LLC?

When your business starts to expand and protecting your personal assets becomes crucial, it might be time to consider forming an LLC. Unlike a sole proprietorship, an LLC creates a legal distinction between your personal assets and the liabilities of your business. This means your personal finances are shielded from business debts or legal claims.

If your business is generating more revenue, hiring employees, or signing contracts that could involve legal risks, transitioning to an LLC offers an added layer of security. Plus, it provides a more structured foundation, which can enhance your business’s credibility and support future growth.

How do I keep LLC liability protection from being lost?

To protect the liability shield of your LLC, it’s crucial to separate personal and business finances. This means maintaining distinct bank accounts and keeping detailed, accurate financial records. Stay on top of compliance obligations, like filing annual reports and paying required fees promptly.

Avoid mixing personal and business funds or offering personal guarantees for business debts. If these boundaries are blurred, courts could "pierce the LLC veil", exposing your personal assets to liability. Also, keep in mind that liability protection won’t cover fraudulent or illegal actions, so always operate your business responsibly.