If you’re a non-US resident owning a US LLC, whether you owe US taxes depends on:

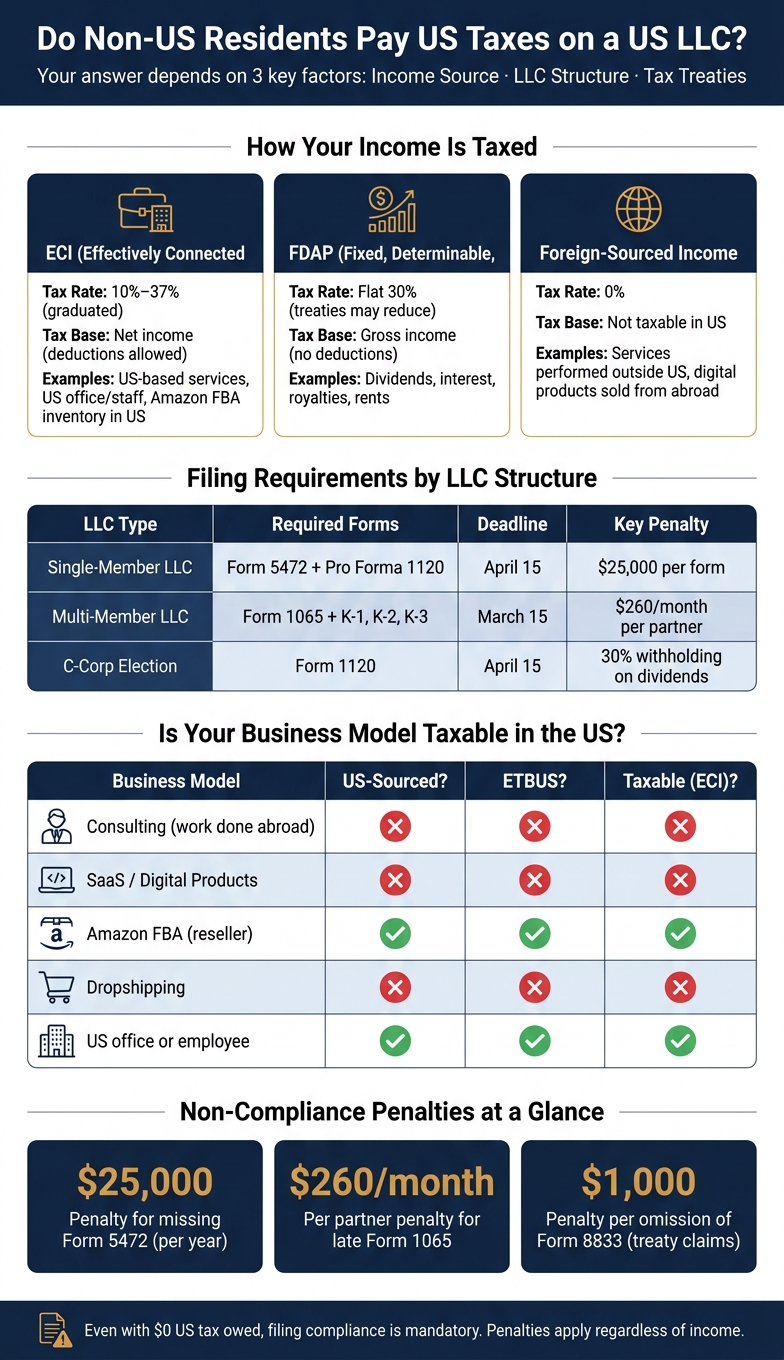

- Income Source: Only US-sourced income or effectively connected income (ECI) is taxable. Services performed outside the US or foreign-sourced income are not taxed in the US.

- LLC Structure: Single-member LLCs must file Form 5472 even if no tax is due, while multi-member LLCs file Form 1065. C-Corp elections involve corporate-level taxes and dividend withholding.

- Filing Obligations: Filing is mandatory even with $0 tax liability. Missing forms like Form 5472 can result in penalties up to $25,000.

- Tax Treaties: Treaties can reduce withholding rates on passive income (like dividends) and prevent double taxation.

Key takeaway: Even if you owe no US taxes, compliance is required. Understand your LLC’s structure, income source, and filing deadlines to avoid penalties.

How the US Tax System Treats Non-US Residents

The US tax system focuses on specific types of income when it comes to non-residents. Understanding what qualifies as taxable income is crucial.

US-Source Income and Effectively Connected Income (ECI)

Non-residents are taxed only on income that is either sourced in the US or effectively connected to a US trade or business.

Effectively Connected Income (ECI) refers to income tied to a US trade or business. This type of income is taxed at federal rates ranging from 10% to 37%, calculated on net income after allowable business deductions. To determine if your LLC’s income qualifies as ECI, the IRS examines your business activities in the US. These activities must be substantial, continuous, and regular – examples include having a physical office, employing US-based staff, or using a dependent agent with authority to sign contracts.

"ECI is the line between paying US taxes as foreign-owned LLC and not paying them." – Vincenzo Villamena, CPA and CEO, Entity Inc.

The location of the work or transaction determines whether income is US-sourced. For instance, services are taxable based on where they are performed, while physical goods are taxed where the title is transferred. A freelance developer in Germany working for US clients, without a US office or staff, would generally generate foreign-sourced income and avoid ECI taxation. This is a common scenario for digital nomads with US LLCs who operate entirely from abroad.

Next, let’s look at passive income, which falls under FDAP rules.

Fixed, Determinable, Annual, or Periodical (FDAP) Income

FDAP income covers passive income like dividends, interest, royalties, and rents. Unlike ECI, FDAP income is taxed at a flat 30% rate on the gross amount, and no deductions are allowed. This tax is typically withheld at the source.

Here’s a breakdown of how different income types are categorized and taxed:

| Income Type | Tax Category | Tax Rate | Tax Base |

|---|---|---|---|

| Business services (US-based) | ECI | 10%–37% | Net income |

| Physical goods (title transfers in US) | ECI | 10%–37% | Net income |

| Dividends, interest, royalties | FDAP | Flat 30% | Gross income |

| Services performed outside the US | Foreign-source | 0% | Not taxable |

| Digital products (seller operates abroad) | Foreign-source | 0% | Not taxable |

Tax treaties between the US and your home country may lower the 30% FDAP withholding rate.

What Non-Residency Means for Your US Tax Obligations

Forming a US LLC does not automatically mean you owe US taxes. Even if your income isn’t subject to US tax, you might still need to meet Form 5472 filing requirements and other informational returns with the IRS. It’s essential to understand the difference between owing taxes and meeting filing requirements – failing to file could lead to penalties, even if no tax is due.

sbb-itb-ba0a4be

When Non-US Residents Owe US Taxes on LLC Income

Understanding how US tax laws apply to non-US residents with LLCs boils down to two key factors: where your income originates and what your LLC does within the United States. Let’s break this down.

Income from Non-US Clients and Work Done Outside the US

If you’re performing services outside the US, that income is treated as foreign-sourced. This holds true even if your clients are based in the US or payments are deposited into a US bank account. For example, imagine a web developer in Portugal running a Wyoming LLC. If they build websites for New York clients from their home in Portugal, they wouldn’t owe US federal income tax on that income because no business activity is happening on US soil.

However, the rules change when your business has a physical presence in the US.

Income from US Customers or US-Based Operations

If your LLC operates within the United States – like hiring US-based employees, opening an office, or storing inventory in a US warehouse – you could be classified as Engaged in a Trade or Business in the United States (ETBUS). This classification makes your income "effectively connected" (ECI) and subject to federal taxes, which range from 10% to 37%.

For those selling physical goods, the location where ownership (or title) transfers determines whether income is US-sourced.

"Income from selling physical goods is sourced based on where title (ownership) transfers to the buyer. Not where the seller is located, not where the goods were manufactured." – Vincenzo Villamena, CPA, CEO at Entity Inc.

Take Amazon FBA sellers, for example. If you store inventory in US fulfillment centers, your income is considered US-sourced because ownership transfers on US soil, making it taxable. On the other hand, dropshipping – where you never take ownership of the goods – typically avoids this exposure.

Here’s a quick comparison of how different business models are treated:

| Business Model | US-Sourced Income? | ETBUS? | Taxable in US (ECI)? |

|---|---|---|---|

| Consulting (work done abroad) | No | No | No |

| SaaS / Digital Products | No | No | No |

| Amazon FBA (reseller) | Yes | Yes | Yes |

| Dropshipping | No | No | No |

| US-based office or employee | Yes | Yes | Yes |

Before worrying about state taxes, you must first understand the process of how non-US citizens can start a US LLC to ensure proper legal standing.

State Tax Obligations for US LLCs

Federal taxes are just one piece of the puzzle. States have their own rules, and some impose fees or taxes even if you owe nothing to the IRS.

For example, forming an LLC in Wyoming or Delaware doesn’t automatically shield you from state-level costs. If your LLC operates in California – whether by storing goods in a warehouse or working with a contractor – the state considers this "doing business" and imposes a minimum $800 annual franchise tax, regardless of income.

"There isn’t a magic US state that deletes federal tax. Structure + presence decide exposure, not a pretty registered-agent address." – James Baker, CPA

Some states, like Wyoming (with a $60 annual fee) or New Mexico (no annual report fee), are more affordable for non-residents without a physical US presence. But if your business activities create a nexus – like hiring employees, storing inventory, or surpassing certain sales thresholds – that state may require additional filings, registrations, and tax payments.

How LLC Structure Affects Tax and Reporting Obligations

The tax classification of an LLC determines your tax and reporting responsibilities. Mistakes in this area can lead to hefty penalties, so understanding the rules is critical.

Single-Member LLCs as Disregarded Entities

For non-US residents, a single-member LLC (SMLLC) is considered a disregarded entity by default.

"The IRS ‘ignores’ the LLC as an entity for income-tax purposes. The owner of the LLC must report all income on their individual tax return." – Vincenzo Villamena, CEO, Entity Inc.

Here’s the catch: even if your LLC generates no taxable income, you’re still required to file Form 5472 (along with a pro forma Form 1120) to disclose all transactions between you and the LLC. This includes capital contributions, distributions, and other financial exchanges.

"Formation alone – the act of paying to register the LLC... creates reportable transactions on Form 5472 for year one." – David Stancel

For example, in 2026, Maria, a Spanish UX designer, formed a Wyoming SMLLC and deposited $3,000 to set it up. She invoiced $92,000 to global clients while working from Spain and owed $0 in US federal taxes. However, she still had to file Form 5472 to report her $3,000 contribution and $65,000 in distributions. Her compliance costs totaled about $1,009. If she had skipped filing, she would have faced a $25,000 penalty – equal to 27% of her annual revenue.

Failure to file Form 5472 comes with a $25,000 penalty per year. Additionally, if the LLC generates Effectively Connected Income (ECI), you must also file Form 1040-NR as your personal US tax return.

Multi-Member LLCs as Partnerships

When a US LLC has two or more owners, it’s automatically taxed as a partnership. The LLC must file Form 1065 annually, and each partner receives a Schedule K-1 outlining their share of the LLC’s income, deductions, and losses. Foreign partners report their share on Form 1040-NR if ECI applies.

Since 2021, multi-member LLCs with foreign partners must also file Schedules K-2 and K-3 to report international tax-related items. Missing the March 15 filing deadline for Form 1065 results in a penalty of $260 per month, per partner. Many new LLC owners mistakenly assume the filing deadline matches the April 15 deadline for single-member LLCs, which can lead to costly errors.

For those exploring other tax options, electing corporate taxation offers an alternative.

LLCs That Elect Corporate Taxation

Any LLC can choose to be taxed as a C-corporation by submitting Form 8832 to the IRS. Under this setup, the LLC pays taxes at the corporate level and files Form 1120. Profits are not directly passed through to the owners.

For non-US shareholders, this structure introduces a key trade-off: dividends are treated as FDAP income and are subject to a 30% withholding tax, unless a tax treaty reduces this rate. This approach might appeal to founders with substantial US-sourced income who want to avoid filing a personal Form 1040-NR, but the withholding tax on dividends needs careful consideration.

Here’s a quick comparison of the filing requirements for each structure:

| LLC Structure | Federal Filing | Filing Deadline | Key Penalty |

|---|---|---|---|

| Single-Member (Disregarded) | Form 5472 + Pro Forma 1120 | April 15 | $25,000 per form |

| Multi-Member (Partnership) | Form 1065 + Schedules K-1, K-2, K-3 | March 15 | $260/month per partner |

| C-Corp Election | Form 1120 | April 15 | 30% withholding on dividends |

"A non-resident-owned LLC with zero US-source income may owe $0 in federal tax but still face mandatory information reporting requirements with five-figure penalties for non-compliance." – David Stancel

How Tax Treaties Can Reduce Double Taxation

If your home country has a tax treaty with the US, it could significantly lower your tax bill.

How Treaties Lower Withholding Tax Rates

Under standard US rules, the withholding tax rate on FDAP income – like dividends, interest, and royalties – is 30%. However, tax treaties can reduce this rate to 15% or even 0%, depending on the type of income and the specific terms of the treaty.

Beyond lowering withholding rates, these treaties also include Permanent Establishment (PE) rules, which limit the US’s ability to tax your business profits unless you have a fixed presence in the country. This is especially helpful for remote business owners who operate entirely outside the US.

That said, not every country has an active treaty with the US. For example, as of 2024, the treaty with Hungary was terminated, and those with Russia and Belarus are partially suspended. If you’re from one of these countries, the full 30% withholding rate applies without any reductions.

To take advantage of treaty benefits, you need to file Form W-8BEN (for individuals) or Form W-8BEN-E (for entities) with the US withholding agent. You’ll also need a US Taxpayer Identification Number (TIN), such as an ITIN. Additionally, if you’re claiming a treaty position that overrides standard US tax law, you must file Form 8833 with your US tax return. Missing this step could result in a $1,000 penalty for each omission.

These treaty provisions work alongside foreign tax credits to help reduce the burden of double taxation.

Foreign Tax Credits and Coordinating with Your Home Country

If a tax treaty doesn’t fully lower your US tax liability, foreign tax credits (FTC) provide another way to avoid being taxed twice. Many countries allow residents to claim an FTC for taxes paid to the US, ensuring the same income isn’t taxed twice.

"The foreign tax credit is intended to relieve you of a double tax burden when your foreign source income is taxed by both the United States and the foreign country." – IRS Publication 514

To claim the FTC on your US tax return, you’ll need to file Form 1116. If you can’t use all your credits in the current year, they can be carried back one year or forward up to 10 years.

"If you are entitled to a reduced rate of foreign tax based on an income tax treaty between two countries, only the lower rate qualifies for the credit." – Internal Revenue Service

For example, if a treaty limits withholding to 15% but 30% is withheld, you can only claim a credit for the 15% rate. You’ll need to reclaim the excess separately. Ensuring your US filings and home country tax returns are aligned is critical to avoid leaving money on the table.

Leveraging these treaty benefits and foreign tax credits can make a big difference in managing your US tax obligations effectively.

Compliance Checklist for Non-US Residents Who Own US LLCs

This checklist is designed to help non-US residents with US LLCs stay on top of their tax obligations and avoid hefty penalties from the IRS. It’s not just about understanding your tax responsibilities – it’s about filing the right forms on time.

Federal Tax Forms and Filing Requirements

The forms you need to file depend on how your LLC is structured. Here’s a quick rundown:

| Form | Who Files It | Due Date | Purpose |

|---|---|---|---|

| Form 5472 + Pro Forma 1120 | Single-Member LLC (foreign-owned) | April 15 | Reports transactions between the LLC and its foreign owner |

| Form 1065 | Multi-Member LLC | March 15 | Partnership income return |

| Form 1040-NR | Individual owner with ECI | April 15 | Personal return for US-source income |

| Form 7004 | All LLCs | By original due date | Automatic 6-month extension |

| FinCEN 114 (FBAR) | LLCs with foreign accounts over $10,000 | April 15 | Report of foreign bank accounts |

Important Notes:

- Form 5472 must be filed for any reportable transaction, even if no US tax is owed. Missing the deadline can result in penalties exceeding $25,000 per year.

- Foreign-owned single-member LLCs cannot e-file Form 5472 or the pro forma Form 1120. These must be mailed or faxed to the IRS in Ogden, Utah. Always keep proof of submission.

"The US LLC is not a loophole. It’s a legitimate structure with legitimate compliance requirements that most foreign founders don’t discover until they’re staring at a penalty notice." – David Stancel, Tax Consultant

State-Level Reporting and Annual Filings

In addition to federal filings, each state has its own requirements. Most states require annual filings to maintain an LLC’s good standing, and some impose taxes regardless of your business activity.

| State | Annual Requirement | Typical Due Date |

|---|---|---|

| Wyoming | Annual Report | 1st day of anniversary month |

| Delaware | Franchise Tax | June 1 |

| Florida | Annual Report | May 1 (late fee: $400 after this date) |

| California | Minimum Franchise Tax | 15th day of the 4th month |

State-specific rules can vary, so it’s critical to meet deadlines to avoid penalties. Additionally, if your LLC sells physical goods in the US and exceeds $100,000 in sales or 200 transactions in a state, you may need to register for and collect sales tax under economic nexus laws.

Other Compliance Requirements to Keep in Mind

Beyond federal and state filings, there are a few more compliance points to remember:

- Beneficial Ownership Information (BOI): Under the Corporate Transparency Act, most LLCs must file BOI reports with FinCEN. These reports disclose details about individuals who own or control the company.

- Registered Agent: Every LLC must have a registered agent with a physical address in the state of formation. This ensures you receive time-sensitive legal notices. For example, BusinessAnywhere offers registered agent services starting at $147 per year.

- Recordkeeping: Keep all financial records for at least seven years. Document every transaction, including capital contributions, distributions, or loans. Even personal transactions, like paying for LLC formation from your personal account, can trigger Form 5472 filing requirements.

BusinessAnywhere provides a US LLC Tax Filing service that handles Form 5472 and the pro forma Form 1120 for $700, with an optional EIN add-on available for $97.

"Filing Form 5472 correctly can help you avoid costly penalties and keep your LLC in good standing… even if your LLC is dormant or only holds a bank account, you’re likely still required to file." – Rick Mak, Global Entrepreneur and Business Strategist, BusinessAnywhere

Key Takeaways on US Taxation for Non-US Residents

If you’re a non-US resident, your tax obligations in the US depend on where your income originates. Generally, income sourced outside the US is not taxed by the US. However, if your LLC earns income through US-based activities or receives passive US-sourced payments, US tax rules will apply.

Active business income earned in the US, known as Effectively Connected Income (ECI), is taxed at graduated rates ranging from 10% to 37%. On the other hand, passive income like interest or dividends, referred to as Fixed, Determinable, Annual, or Periodical (FDAP) income, is taxed at a flat 30% rate. But here’s the good news: if your home country has a tax treaty with the US, these rates can be reduced. To take advantage of treaty benefits, you’ll need to file Form W-8BEN before receiving payments and Form 8833 with your tax return.

It’s crucial to understand that owing no US tax does not mean you’re exempt from filing requirements.

"The founders who get hurt are the ones who treat ‘no US tax owed’ as ‘no US compliance required.’ Those are different sentences." – David Stancel, Founder

Failing to meet filing obligations can be costly. For instance, multi-member LLCs face penalties of $260 per partner, per month for not filing Form 1065. Even if your LLC is inactive and earns no income, you must file Form 5472 to avoid a $25,000 penalty. Compliance isn’t optional; it’s a mandatory cost of doing business, no matter where you reside or where your income originates.

For non-US LLC owners, understanding the source of your income, your business structure, and any treaty benefits is essential to staying compliant and avoiding hefty penalties. These key points should guide you as you navigate your US tax responsibilities.

FAQs

Do I need to file US taxes if my LLC has $0 income?

Even if your LLC hasn’t generated any income, you’re still required to file specific forms. For foreign-owned single-member LLCs, this includes:

- Form 5472: Used to report transactions between the LLC and its foreign owner.

- Pro forma Form 1120: Filed alongside Form 5472.

These forms must be submitted annually, regardless of whether the LLC had any business activity or revenue. Ignoring this requirement can lead to hefty penalties – starting at $25,000 per year. Staying compliant is crucial to avoid these fines.

What makes my LLC income “effectively connected” to the US?

Your LLC income qualifies as effectively connected income (ECI) if it meets two key criteria:

- The income is sourced from the United States.

- Your business is actively involved in a trade or business within the United States (ETBUS).

To meet the ETBUS standard, your business generally needs to have ongoing, meaningful activities in the U.S. – like employing U.S.-based staff, operating a physical office, or using dependent agents. Just having U.S. customers alone does not qualify your income as effectively connected.

Which IRS forms do foreign-owned LLCs usually file?

The IRS filing requirements for your LLC depend on its ownership structure:

- Single-Member LLC (Disregarded Entity): You’ll need to file Form 5472 along with a pro forma Form 1120. This applies even if your LLC has no U.S. income tax liability.

- Multi-Member LLC (Treated as a Partnership): In this case, the required filings include Form 1065 and a Schedule K-1 for each partner. If your LLC has international activities, you’ll likely need to include Schedules K-2 and K-3 as well.

These forms are mandatory regardless of whether your LLC owes any U.S. income tax.