The Qualified Business Income (QBI) deduction under Section 199A lets LLC owners deduct up to 20% of their business income from federal taxable income. This tax break, introduced in 2017, was made permanent through 2034 by the One Big Beautiful Bill Act in 2025. It’s a major tax-saving tool for pass-through entities like LLCs.

Here’s what you need to know:

- Who qualifies: LLCs taxed as sole proprietorships, partnerships, or S corporations. C corporations are excluded from this specific deduction.

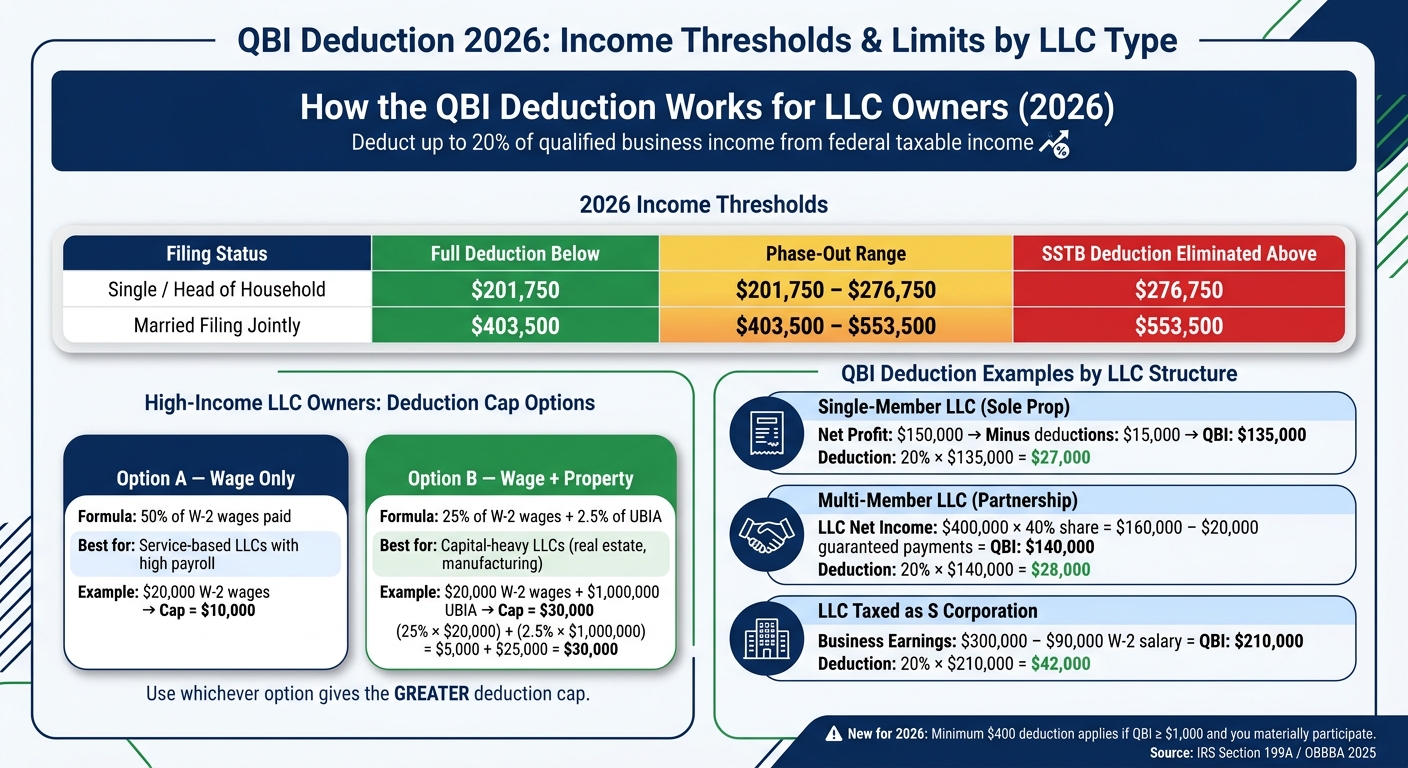

- Income thresholds (2026): Full deduction applies below $201,750 (single) or $403,500 (married filing jointly). Phase-outs apply above these limits.

- Specified Service Trades or Businesses (SSTBs): Professions like law and accounting face stricter limits.

- Calculation basics: Deduct 20% of QBI, but limits apply based on W-2 wages and property owned by the business.

- Key updates for 2026: A $400 minimum deduction now applies if you earn at least $1,000 in QBI and materially participate.

The deduction can be complex, especially for high earners or SSTBs. Proper planning, accurate records, and understanding limits are crucial to maximizing your tax savings.

Who Qualifies for the QBI Deduction

Whether your LLC qualifies for the QBI deduction depends on its tax structure, your taxable income, and the type of business you operate.

LLC Structures That Qualify

The QBI deduction is designed for pass-through entities, where profits flow directly to the owner’s personal tax return.

"Entity form does not determine eligibility. What matters is whether the taxpayer has qualified business income from a qualified trade or business." – Steven Cashiola, CPA

Here’s how different LLC tax structures qualify:

- Single-member LLCs (taxed as sole proprietorships): Most net profits qualify as QBI after accounting for self-employment tax.

- Multi-member LLCs (taxed as partnerships): Each member’s share of the profits qualifies as QBI on their personal tax returns.

- LLCs taxed as S corporations: Only the pass-through distributions qualify as QBI. Any W-2 salary paid to the owner is excluded.

C corporations are not eligible for the QBI deduction since their income is taxed at the corporate level. Additionally, the LLC must operate as a domestic trade or business. Income earned from activities conducted outside the U.S. does not qualify.

Next, let’s look at how income thresholds and phase-outs affect your eligibility.

Income Thresholds and Phase-Outs

Your taxable income plays a major role in determining how much of the QBI deduction you can claim. If your income falls below the threshold, you can take the full 23% deduction on your QBI without any restrictions. However, exceeding the threshold triggers limitations.

| 2026 Filing Status | Full Deduction Below | Phase-out Range | SSTB Deduction Eliminated Above |

|---|---|---|---|

| Single / Head of Household | $201,750 | $201,750 – $276,750 | $276,750 |

| Married Filing Jointly | $403,500 | $403,500 – $553,500 | $553,500 |

Source: OBBBA statutory changes, 2026 projections [11]

For non-SSTB LLCs above the income threshold, the deduction is limited by the W-2 wages paid and the qualified property owned by the business. For SSTBs, the deduction decreases gradually within the phase-out range and is completely eliminated once the upper limit is reached.

It’s important to note that taxable income for QBI purposes is calculated before applying the deduction. Also, starting in 2026, taxpayers with at least $1,000 in QBI who materially participate must meet a $400 minimum deduction requirement.

Specified Service Trades or Businesses (SSTBs)

SSTBs include businesses in IRS-defined service fields such as health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, and brokerage services. If a business primarily relies on the owner’s personal reputation or skill – like income from endorsements or licensing their image – it is also classified as an SSTB.

"Professional service businesses – lawyers, doctors, accountants, consultants, financial advisors – face the full SSTB phaseout above the threshold and lose the deduction entirely above the phaseout completion." – Reed Corporation CPA Firm

Certain industries, such as engineering and architecture, are specifically excluded from the SSTB category. Similarly, real estate agents, insurance agents, and health club operators generally fall outside this classification.

For businesses that earn income from both service and non-service activities, the de minimis rule applies. If a business with gross receipts of $25 million or less earns less than 10% of its revenue from specified service fields, it can avoid being classified as an SSTB. This allows mixed-revenue businesses to retain part of the QBI deduction.

How to Calculate the QBI Deduction for LLCs

The Basic Calculation Formula

Once you’ve confirmed eligibility, calculating your Qualified Business Income (QBI) deduction is relatively straightforward. The formula starts with deducting 20% of your QBI, plus 20% of any qualified REIT dividends and Publicly Traded Partnership (PTP) income.

However, there’s an important cap. Your total deduction is limited to the lesser of:

- The sum of the QBI component and the REIT/PTP component, or

- 20% of your taxable income minus net capital gains

"20% of your qualified business income, deducted on your personal return. It stacks on top of every other deduction." – Reese Tax & Wealth

It’s also worth noting that QBI excludes several types of income: W-2 wages, guaranteed payments, dividends, interest, and capital gains. Only active business profits are included.

W-2 Wage and Qualified Property Limits

If your income exceeds the 2026 thresholds ($201,750 for single filers; $403,500 for married filers), additional limits apply. In this case, the deduction is capped by either 50% of W-2 wages or a combination of 25% of W-2 wages plus 2.5% of UBIA (unadjusted basis immediately after acquisition) of qualified property.

The limit is calculated as the greater of:

- Option A: 50% of W-2 wages paid by the business

- Option B: 25% of W-2 wages + 2.5% of UBIA of qualified property

UBIA reflects the original purchase price of tangible, depreciable assets like buildings or equipment. Even if an asset is fully depreciated, it still counts toward UBIA as long as it remains within its depreciable period (the later of 10 years from the service date or the end of its MACRS recovery period).

| Limitation Option | Formula | Best For |

|---|---|---|

| Option A (Wage-Only) | 50% of W-2 wages | Service-based LLCs with high payroll |

| Option B (Wage + Property) | 25% of W-2 wages + 2.5% of UBIA | Capital-heavy LLCs (real estate, manufacturing) |

For instance, real estate LLCs often favor Option B due to their high property basis but relatively low W-2 wages. A rental LLC with $1,000,000 in UBIA and $20,000 in W-2 wages would calculate its limit under Option B as follows:

(25% × $20,000) + (2.5% × $1,000,000) = $5,000 + $25,000 = $30,000, compared to just $10,000 under Option A.

Calculation Examples by LLC Tax Classification

The calculation process varies depending on how your LLC is taxed.

Single-member LLC (sole proprietorship): Start with your net profit from Schedule C. Subtract deductible expenses like the self-employment tax, health insurance premiums, and retirement contributions. For example, if your net profit is $150,000 and these deductions total $15,000, your QBI is $135,000. The deduction would then be 20% × $135,000 = $27,000, provided your taxable income is below the threshold.

Multi-member LLC (partnership): Use your share of income from Schedule K-1 as the QBI base, excluding guaranteed payments for services. If you own 40% of an LLC with $400,000 in net income and received $20,000 in guaranteed payments, your QBI would be:

($400,000 × 40%) − $20,000 = $140,000.

LLC taxed as an S corporation: Only the pass-through distribution on your Schedule K-1 qualifies as QBI. Your W-2 salary from the S corp is excluded. For example, if the business earns $300,000 and you pay yourself a $90,000 salary, your QBI is $300,000 − $90,000 = $210,000. The deduction would be 20% × $210,000 = $42,000. If you’re above the income threshold, the 50% W-2 wage limit would apply:

50% × $90,000 = $45,000, which is higher than the $42,000 deduction, so the full deduction remains valid.

Looking ahead to 2026, there’s a minimum deduction rule. If your aggregate QBI is at least $1,000 and you materially participate in the business, you qualify for a minimum deduction of $400, even if other limits would otherwise reduce it.

Tax Planning Strategies to Maximize the QBI Deduction

Aggregating Multiple Businesses

If you own multiple LLCs, you might be able to combine their Qualified Business Income (QBI), W-2 wages, and Unadjusted Basis Immediately After Acquisition (UBIA) to make the most of the QBI deduction. This strategy works especially well when one business has strong profits but low wage expenses, while another has higher payroll costs relative to its income.

To qualify for aggregation, you must own at least 50% of each business for most of the tax year and meet two of the following three criteria: shared products or services, centralized business functions, or operational interdependence. However, Specified Service Trades or Businesses (SSTBs) cannot be part of an aggregated group.

"The aggregation rules… allow taxpayers to aggregate multiple businesses for purposes of the W-2 wage and UBIA tests if certain common ownership and operational criteria are met." – Reed Corporation CPA Firm

Once you choose to aggregate, the decision must be applied consistently every year unless there’s a significant change in circumstances. To stay compliant, you’ll need to report aggregated businesses annually on Schedule B of Form 8995-A. Failing to do so could result in the IRS disallowing your aggregation.

If aggregation isn’t an option, you might consider adjusting owner compensation to optimize your deduction.

Reasonable Compensation for S Corporation Owners

For LLCs taxed as S corporations, finding the right balance between W-2 wages and profit distributions is key to maximizing the QBI deduction. Since wages don’t count as QBI, keeping your salary lower can increase the portion of income eligible for the deduction. However, if your income exceeds the 2026 thresholds ($201,750 for single filers and $403,500 for married couples filing jointly), the deduction becomes subject to the W-2 wage test. In this case, paying yourself too little could actually hurt you because the deduction is capped at 50% of W-2 wages paid.

The goal is to hit the "sweet spot" – a salary that meets the IRS’s reasonable compensation standards while leaving enough profit to maximize your deduction.

"Reasonable compensation paid by an S-corp to a shareholder-employee is wages, not QBI." – Reed Corporation CPA Firm

For higher earners, W-2 wages should typically fall between 40%–46% of QBI to avoid running into the wage-based limitation. Reviewing your payroll before the end of the year allows you to tweak compensation if needed to optimize the deduction.

Now, let’s take a look at how rental real estate can factor into your QBI planning.

Rental Real Estate and QBI Eligibility

Rental income can qualify as QBI, but only if the rental activity meets the IRS’s criteria for a trade or business under Section 162. One straightforward way for landlords to qualify is by meeting the IRS safe harbor outlined in Rev. Proc. 2019-38, which requires at least 250 hours of rental services annually. These services can include advertising vacancies, tenant screening, collecting rent, and performing repairs. Keeping detailed and contemporaneous records – such as logs of dates, activities, and hours – is crucial for meeting this requirement.

There’s an easier path for self-rental situations. If you rent property to a business in which you own at least a 50% stake, the rental activity is automatically treated as a qualified trade or business without the 250-hour requirement. This arrangement is common when an LLC owns real estate and leases it to an operating S corporation owned by the same individual. However, triple-net leases generally don’t qualify under the safe harbor and may face closer scrutiny.

Additionally, increasing retirement contributions through plans like SEP-IRAs, 401(k)s, or defined benefit plans can help reduce taxable income, making it easier to claim the full QBI deduction.

sbb-itb-ba0a4be

Steps to Claim the QBI Deduction as an LLC Owner

Keeping your documentation accurate and filing on time is key to making the most of the deductions outlined above. Once you’ve calculated your Qualified Business Income (QBI) deduction, the next step is ensuring everything is properly documented and filed.

Tax Documents You Need to Gather

The documents you need will depend on how your LLC is taxed. One of the most important forms is the K-1, which must include the Section 199A Statement. This statement provides the QBI, W-2 wages, and UBIA (Unadjusted Basis Immediately After Acquisition) figures essential for calculating your deduction.

In addition to the K-1, here’s what else you’ll need:

- W-2 payroll records: Necessary if your income exceeds the phase-out threshold.

- Depreciation schedule: This shows the original cost of your tangible business assets (UBIA).

- Prior-year tax returns: Check for any qualified business loss carryforwards that could impact your current QBI.

- Contemporaneous time logs and certification statement: Required for rental LLCs that qualify under the 250-hour safe harbor rule.

Here’s a quick overview of the key documents and their purposes:

| Document | Why You Need It |

|---|---|

| Schedule C or Schedule E | Reports your LLC’s net business income |

| Schedule K-1 + Section 199A Statement | Provides QBI, W-2 wage, and UBIA figures for pass-through entities |

| Form W-2 / Payroll Records | Used to calculate the wage limit for high-income taxpayers |

| Depreciation Schedule (UBIA) | Supports the property limit calculation on Form 8995-A |

| Prior-Year Tax Returns | Identifies qualified business loss carryforwards |

| Time Logs (Rental LLCs) | Documents 250+ hours of rental services for safe harbor qualification |

Once you’ve gathered these documents, you’ll be ready to complete the required IRS form for your QBI deduction. Understanding how to file taxes as an LLC ensures you don’t miss other valuable write-offs.

Filing IRS Form 8995 or 8995-A

The form you use depends on your taxable income:

- Form 8995: If your taxable income is below the 2026 thresholds ($200,000 for single filers and $400,000 for married couples), this is the simpler option. Multiply your net QBI by 20%, then compare it to 20% of your taxable income minus net capital gains. The smaller amount is your deduction.

- Form 8995-A: Use this if your income exceeds the thresholds, if you need to aggregate multiple businesses, or if you operate a Specified Service Trade or Business (SSTB) subject to phase-outs. This form includes additional schedules, such as Schedule B for aggregation and Schedule D for SSTB phase-outs.

"The QBI deduction is claimed using Form 8995 for straightforward cases or Form 8995-A when limitations apply." – Carry

For 2026, there’s a minimum $400 deduction if your QBI is at least $1,000 and you materially participate in the business – even if the standard 20% calculation gives you a smaller number. Report your final deduction amount on Line 13 of Form 1040. This applies whether you take the standard deduction or itemize.

Once you determine which form applies to your situation, follow the instructions carefully to ensure a smooth filing process.

How BusinessAnywhere Can Help

Accurate QBI claims rely on solid record-keeping throughout the year – not just during tax season. BusinessAnywhere’s virtual mailbox service makes it easy to stay on top of your paperwork by scanning and storing essential documents, such as IRS notices and K-1s, as soon as they arrive.

For LLC owners needing additional services, BusinessAnywhere offers:

- S-Corp tax election filing: $97

- Annual compliance maintenance: $147 per year

- Tax and residency consultation: $535 for a one-hour personalized session

If you’re a foreign-owned LLC or need an EIN to file Form 8995, BusinessAnywhere’s EIN application service, priced at $97, takes care of the process for you. They also offer bookkeeping services, which are particularly useful for rental LLCs working to meet the 250-hour safe harbor requirement.

Key Takeaways for LLC Owners

The Qualified Business Income (QBI) deduction is now a permanent part of the U.S. tax code, thanks to the One Big Beautiful Bill Act (OBBBA) signed into law on July 4, 2025. As Steven J. Cashiola, CPA, explains:

"Section 199A is a structural feature of passthrough taxation rather than a temporary benefit."

This permanence gives LLC owners the ability to develop long-term tax strategies with greater confidence.

Your eligibility for the deduction depends on several factors: taxable income relative to the 2026 thresholds, whether your business qualifies as a Specified Service Trade or Business (SSTB), and the amount of W-2 wages or qualified property your business holds. If your income exceeds the thresholds, strategic planning becomes critical to ensure you can secure and maximize the deduction.

Interestingly, about 42% of eligible taxpayers fail to claim the full QBI deduction. This often happens due to inadequate documentation, missed opportunities to optimize wages in an S-corp structure, or failing to meet the record-keeping requirements for rental real estate safe harbor qualification. Even small oversights in planning or documentation can lead to a higher tax bill.

To make the most of the QBI deduction, focus on these key steps:

- Regularly monitor your taxable income and maintain detailed business records throughout the year.

- Adjust your S-corp salary to strike the right balance for deduction optimization.

These strategies align with the broader planning techniques covered in this guide, including aggregation, compensation structuring, and rental safe harbor compliance. For example, if you’re in a 24% tax bracket, proper planning could save you approximately 4.8% in taxes on your business income – a savings well worth the effort.

FAQs

What income counts as QBI for my LLC?

Qualified Business Income (QBI) refers to the net total of qualified income, gains, deductions, and losses generated by your LLC’s trade or business activities. What counts as QBI depends on how your LLC is taxed – whether it’s treated as a sole proprietorship, partnership, or S corporation.

However, some items are specifically excluded from QBI, including:

- Wages or reasonable compensation paid to S corporation shareholders.

- Guaranteed payments made to partners.

- Investment-related income such as capital gains and dividends.

- Foreign income and certain types of interest.

Understanding what qualifies as QBI is essential for determining eligibility for deductions and tax benefits.

How do W-2 wages and UBIA limit my deduction?

If your taxable income falls below the 2026 thresholds – $201,750 for single filers or $403,500 for married filing jointly – the W-2 wage and UBIA (Unadjusted Basis Immediately After Acquisition) limitations won’t apply to you. However, if your income exceeds these thresholds, the deduction is capped at the greater of:

- 50% of W-2 wages, or

- 25% of W-2 wages plus 2.5% of the UBIA of qualified property.

These limitations don’t kick in all at once; instead, they phase in gradually until they fully apply.

Does my rental LLC qualify for the QBI deduction?

Yes, your rental LLC might qualify for the Qualified Business Income (QBI) deduction, but there are specific requirements to meet. Your rental activity must either:

- Operate as a Section 162 trade or business, which means it demonstrates a profit motive, operates with continuity, and performs activities on a regular basis.

- Or, meet the IRS safe harbor rules. To satisfy these, you’ll need to:

- Maintain separate books and records for the rental activity.

- Perform 250+ hours of qualifying rental services each year.

- Keep contemporaneous records to document hours, services performed, and who completed them.

Additionally, rentals to commonly controlled businesses may also qualify under certain conditions.