If you’re running a business and want to protect your personal assets, forming an LLC (Limited Liability Company) is a smart move. Here’s when you should consider it:

- You’re earning consistent revenue: If your business income is steady or exceeds $100,000 annually, forming an LLC can reduce risks and offer potential tax advantages.

- You face legal risks: High-risk industries like real estate, professional services, or product sales make your personal assets vulnerable. An LLC creates a legal shield.

- You’re adding partners: An LLC ensures clear ownership rules and liability protections in multi-owner businesses.

- You’re serious about growth: If you’re scaling operations, signing contracts, or managing customer data, an LLC boosts credibility and safeguards your finances.

Before filing, ensure you have a unique business name, a registered agent, an operating agreement, and an EIN (Employer Identification Number). Filing fees vary by state, typically ranging from $35 to $500. For remote businesses, states like Wyoming or New Mexico may offer cost-effective options.

Key takeaway: Form your LLC before risks or liabilities arise. It’s a low-cost step that protects your personal assets and positions your business for growth.

What Changes When You Open an LLC

Forming an LLC brings about shifts in how your business operates, how taxes are handled, and what compliance requirements you’ll need to meet. Each of these changes plays a role in deciding when it’s the right time to move from being a sole proprietor to establishing an LLC.

Legal Protections and Liability

As a sole proprietor, there’s no distinction between you and your business. This means your personal assets – like your home, savings, or car – could be at risk if your business faces lawsuits or debt. An LLC creates a legal barrier that separates your personal and business assets, offering protection as long as you maintain compliance with regulations.

"An LLC fixes that [legal exposure]. It creates a legal wall between your business and your personal life." – Marcus Williams, Business Writer

However, this protection isn’t automatic. If you mix personal and business finances or fail to meet compliance requirements, courts can "pierce the corporate veil", holding you personally liable for business obligations.

While asset protection is a key benefit, forming an LLC also changes how your business is taxed.

Tax Implications

By default, an LLC is treated as a pass-through entity for tax purposes. For single-member LLCs, this means profits are reported on your personal tax return using Schedule C, similar to a sole proprietorship. Multi-member LLCs are taxed like partnerships, with profits and losses passed through to your personal tax return, avoiding double taxation.

If your LLC’s net profits exceed $40,000–$50,000 annually, you might consider electing S-Corp status over a standard LLC. This allows you to divide income between a salary and distributions, potentially reducing the 15.3% self-employment tax. However, it’s important to note that forming an LLC doesn’t automatically reduce your taxes. Instead, it gives you more options for strategic tax planning.

Once your legal and tax structures are set, operational adjustments are essential to fully benefit from your LLC.

Day-to-Day Operational Changes

After forming an LLC, one of the first steps is separating personal and business finances. Open a business bank account, appoint a registered agent, and prepare for ongoing compliance filings.

A registered agent is responsible for receiving legal documents on behalf of your LLC. They must be available during business hours, as missing legal notices can lead to default judgments.

Additionally, most states require annual reports or franchise tax filings, with fees ranging from $50 to $300 per year. Drafting an operating agreement is also critical – even if you’re the sole member. This document helps solidify your LLC’s status as a separate legal entity and is often required by banks when opening a business account.

"If the LLC has no operating agreement, I may have to work with the client to comb through emails and other documents to piece together agreements… The result is less certainty and higher legal fees." – Omaima Poonawala, Corporate & Trademark Attorney

Signs It’s Time to Open an LLC

Starting an LLC can make sense when your business income grows, your industry poses legal risks, or you bring on partners. If any of these situations apply, it may be time to establish a more formal business structure.

Sign 1: You’re Earning Consistent Revenue

Once your business starts generating steady income, the risks you face increase. For sole proprietors vs. LLCs, consistent revenue also comes with a higher chance of being audited. In fact, sole proprietors are 2.5 times more likely to face an IRS audit compared to structured entities like LLCs. On top of that, if your annual profits exceed $100,000, the potential tax savings alone might offset the cost of forming an LLC.

"Simple rule: once money or risk enters the picture, it’s time." – StartFleet Staff

If you’re already earning regularly, it’s a good idea to evaluate whether your industry-specific risks make forming an LLC even more critical.

Sign 2: You Work in a High-Risk Industry

Some industries naturally carry greater risks, such as lawsuits, disputes, or liability claims. If you’re in professional services (like law, medicine, or accounting), sell physical products, invest in real estate, or manage events, your personal assets could be at stake if something goes wrong. For example, 70% of small businesses use LLCs to prevent business risks from spilling over into their personal finances.

Real estate investors, in particular, often form LLCs when their property holdings exceed $1,000,000. Why? Because doing so can reduce legal liability exposure by up to 50%. Similarly, professionals like doctors, attorneys, and CPAs often choose Professional LLCs (PLLCs) to address liability concerns specific to their licensed fields.

If you’re dealing with high risks in your industry, an LLC can act as a shield for your personal finances. The same applies when you’re sharing ownership with others.

Sign 3: Adding Partners

Partnering with others can be risky if you don’t have the right structure in place. In informal partnerships, each partner is personally liable for the other’s actions, including debts or legal issues. By creating an LLC, you establish a separate legal entity, ensuring that business liabilities don’t automatically affect your personal assets.

An LLC also allows you to draft an operating agreement, which lays out key details like ownership percentages, rules for transferring shares, and how disputes will be resolved. Without a formal agreement, disagreements could lead to costly legal battles, often relying on informal communications like emails to resolve issues. If you’re planning to build a long-term business with partners, formalizing your structure with an LLC is a smart move.

Key Considerations Before You File

You should only file your LLC when your business is actively working with clients, collecting payments, shipping products, or handling customer data. Filing too early can lead to unnecessary expenses and compliance headaches.

Pre-Formation Checklist

Before filing, make sure you’ve checked off these crucial tasks:

- Business name: Confirm that your chosen name is available, stands out, and includes "LLC" or "Limited Liability Company." Attorney Omaima Poonawala emphasizes that simpler names can help avoid future complications:

"Simpler names reduce the risk of future limitations." – Omaima Poonawala, Corporate & Trademark Attorney

- Registered agent: Every state requires a registered agent with a physical address (no P.O. Boxes) to receive legal documents on your business’s behalf.

- Operating agreement: Even if your state doesn’t require it, creating an operating agreement is a smart move. It outlines ownership shares, how disputes will be handled, and the process for transferring interests.

- EIN: Apply for your Employer Identification Number (EIN) directly through the IRS. It’s free, quick, and essential for opening a business bank account, hiring employees, and managing taxes.

Also, avoid filing in late December unless necessary. For example, filing on December 28 could result in overlapping annual requirements. Starting on January 1 instead simplifies bookkeeping.

Once these steps are complete, take time to understand the costs and compliance responsibilities that come with forming an LLC.

Costs and Ongoing Compliance

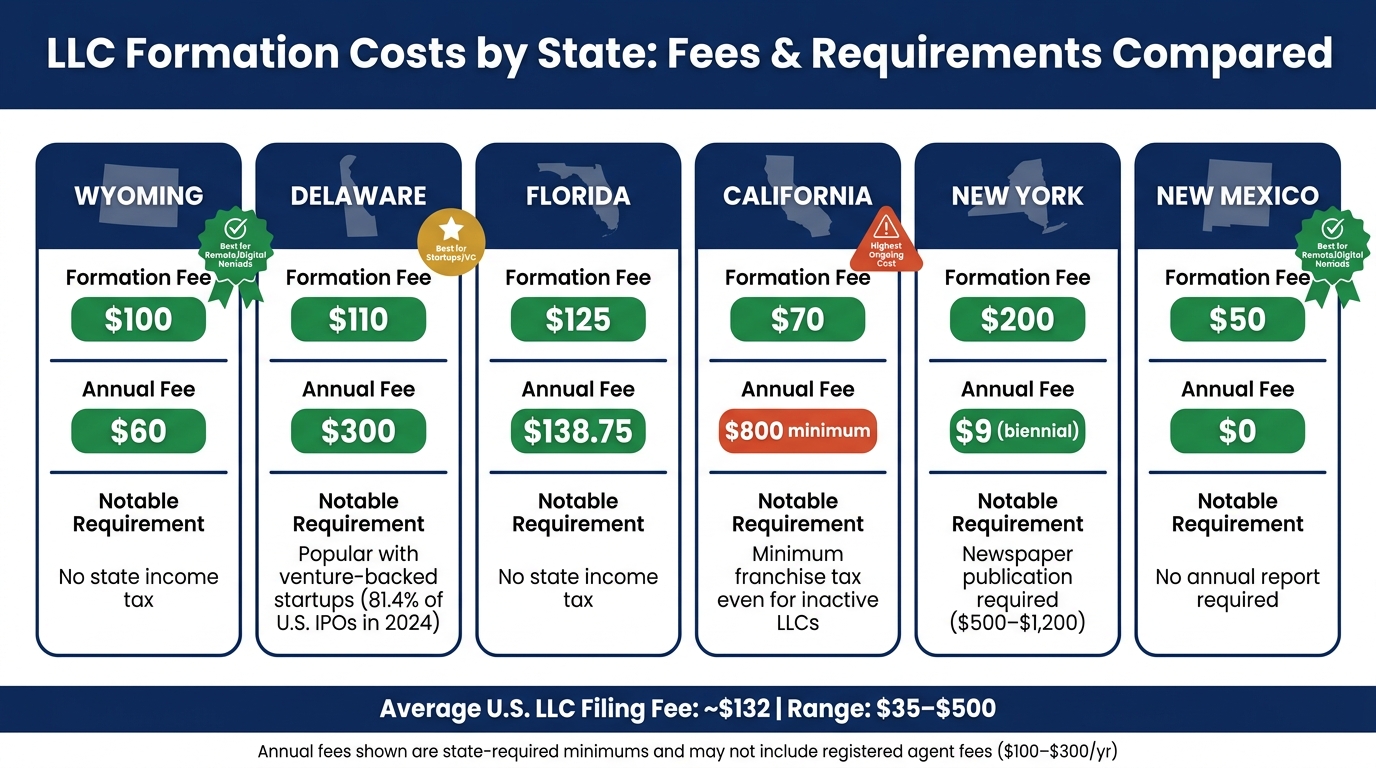

The upfront costs of forming an LLC are generally affordable. State filing fees range from $35 to $500, with the average being about $132. If you need registered agent services, expect to pay $100 to $300 annually.

Ongoing requirements differ by state. Here’s a quick overview of some popular states:

| State | Formation Fee | Annual Fee | Notable Requirement |

|---|---|---|---|

| Wyoming | $100 | $60 | No state income tax |

| Delaware | $110 | $300 | Popular with venture-backed startups |

| Florida | $125 | $138.75 | No state income tax |

| California | $70 | $800 minimum | Minimum franchise tax, even for inactivity |

| New York | $200 | $9 (biennial) | Newspaper publication required ($500–$1,200) |

| New Mexico | $50 | $0 | No annual report required |

As Marcus Williams of Kinja Business puts it:

"For $132 and 30 minutes, the LLC is the cheapest insurance policy you’ll ever buy for a business."

If your business operates remotely, there are additional factors to consider to ensure your LLC setup works for your unique situation.

Considerations for Remote and Digital Nomad Businesses

For remote businesses, forming your LLC in your home state is usually the most practical and cost-effective choice. If you form an LLC in another state, like Wyoming, while living in Florida, you’ll likely need to register as a foreign LLC in your home state. This can double your filing fees and compliance requirements.

That said, some states are more appealing for remote businesses without a physical location. Wyoming offers strong privacy protections and low annual fees ($60), while New Mexico doesn’t charge annual report fees at all.

If you’re running a fully remote business, you’ll also need a professional U.S. address to meet state requirements. A registered agent service can provide this while keeping your personal address off public records.

sbb-itb-ba0a4be

Making the Decision and Next Steps

Assess Your Goals and Risk Exposure

Before filing for an LLC, take a moment to evaluate your situation. Are you generating steady income? Do you own personal assets – like savings, a home, or investments – that could be at risk if faced with lawsuits or unpaid debts? Are you signing contracts, storing customer data, or working in a field where errors might lead to big financial consequences?

If you answered yes to any of these, it might be the right time to form an LLC. However, if you’re just testing out an idea with little revenue and minimal client-facing risk, waiting a few months could be fine. The key is to establish your LLC before any issues arise, not after. Careful planning ensures you protect your assets and set up your operations smoothly.

You should also think about taxes. Once your LLC starts earning around $80,000–$100,000 annually in profit, opting for S-corp status could significantly lower your self-employment tax burden. This makes planning ahead even more crucial.

With your goals and risks in mind, you’re ready to move on to the steps for setting up your LLC.

Step-by-Step LLC Formation Process

Here’s a simple guide to forming your LLC:

- Choose Your State of Formation: For most small businesses, forming your LLC in your home state is the easiest option. If venture capital is part of your plan, Delaware is the go-to choice – 81.4% of U.S. IPOs in 2024 were based there. Wyoming is another option for privacy and low fees.

- Confirm Your Business Name: Your chosen name must be unique among registered businesses in your state and include "LLC" or "Limited Liability Company." Check your state’s Secretary of State website to confirm availability.

- Appoint a Registered Agent: This person or service will receive legal documents on your behalf and must have a physical address in your state of formation. If you work from home and prefer to keep your address private, consider hiring a professional registered agent service.

- File Your Articles of Organization: Filing fees vary by state, typically ranging from $35 to $500, though most fall between $50 and $200. Expedited processing can cost an additional $50–$150, depending on the state.

- Apply for Your EIN and Open a Business Bank Account: You can get your EIN for free through the IRS. Use it to open a dedicated business bank account, which is essential for maintaining liability protection.

If it’s late December, consider waiting until January 1 to file. Filing in December might require you to submit annual reports for two consecutive years.

How BusinessAnywhere Can Help

Once you’ve outlined your steps, BusinessAnywhere can streamline the entire process. Their platform handles everything – from LLC filing and registered agent services (free for the first year when bundled with registration) to EIN applications – all managed through an easy-to-use online dashboard.

For entrepreneurs who need a professional U.S. address but don’t want their home address listed publicly, BusinessAnywhere offers a virtual mailbox starting at $20 per month (billed annually). This includes unlimited mail scanning and worldwide forwarding. Their registered agent service is available for as little as $147 per year for ongoing support.

BusinessAnywhere also provides compliance tools to track annual report deadlines and franchise tax filings, ensuring you stay in good standing. If you’re a digital nomad or an international entrepreneur looking to form a U.S. LLC, their Digital Nomad Kit bundles everything you need – LLC formation, registered agent service, EIN application, bank account setup assistance, and tax filing – into one convenient package.

Conclusion

Setting up an LLC is a smart move that protects your personal assets, lowers your tax obligations, and strengthens your business’s credibility. It’s crucial to establish your LLC before any liabilities arise since the protections it offers won’t apply retroactively.

The numbers tell a compelling story: small businesses in the U.S. face roughly $160 billion in liability costs every year, and 37% have dealt with employee lawsuits in the past year alone. By forming an LLC early, you create a legal shield that keeps your personal assets – like your home, savings, and car – safe from potential business risks.

"The question isn’t whether you can afford to form an LLC – it’s whether you can afford not to." – BizUpUSA

When deciding to form an LLC, consider your revenue, the risks involved, any partnerships, and your growth plans. The potential costs of delaying far outweigh the relatively low filing fees, which range from $35 to $500 depending on your state. Armed with this information, you can take the next steps with confidence.

FAQs

Will an LLC protect me if I’m personally sued or personally guarantee a debt?

LLCs can protect you from personal liability if your business encounters legal issues. However, this safeguard has limits. For instance, if you personally guarantee a loan, blur the lines between personal and business finances, or engage in wrongful actions, that protection might not hold up. To ensure your liability shield stays intact, stick to proper business practices.

Do I need to form an LLC in my home state if I run my business remotely?

If you run your business remotely from your home state, you’ll usually need to form your LLC there. States generally view your business as operating locally if it has a physical presence, employs workers, or conducts most of its activities within that state. Choosing to form an LLC in a different state could mean you’ll need to register as a foreign LLC in your home state, which often comes with extra fees and paperwork.

What mistakes can cause me to lose LLC liability protection?

Forming an LLC offers liability protection, but mistakes can jeopardize that safeguard. Frequent missteps include combining personal and business finances, neglecting to keep accurate records, or skipping essential formalities like recording meeting minutes. Additionally, engaging in fraud, illegal actions, or misconduct while operating under the LLC can strip away this protection. To maintain it, keep finances separate and stick to lawful and ethical business practices.